1. The Launchpad: Why OTB Jumped 14% on Final Results

On the Beach Group plc (LSE: OTB) experienced a sharp 14% increase in its share price today, December 2, 2025, immediately following the release of its robust Final Results for the Year Ended 30 September 2025 (FY25).

This dramatic market movement was a reaction to management's delivery of better-than-expected profitability and clear strategic direction. The increase reflects a reassessment of the company's value based on strong fundamental performance, resolving market uncertainty that had impacted the stock earlier in the year.

The primary factors driving the significant re-rating were:

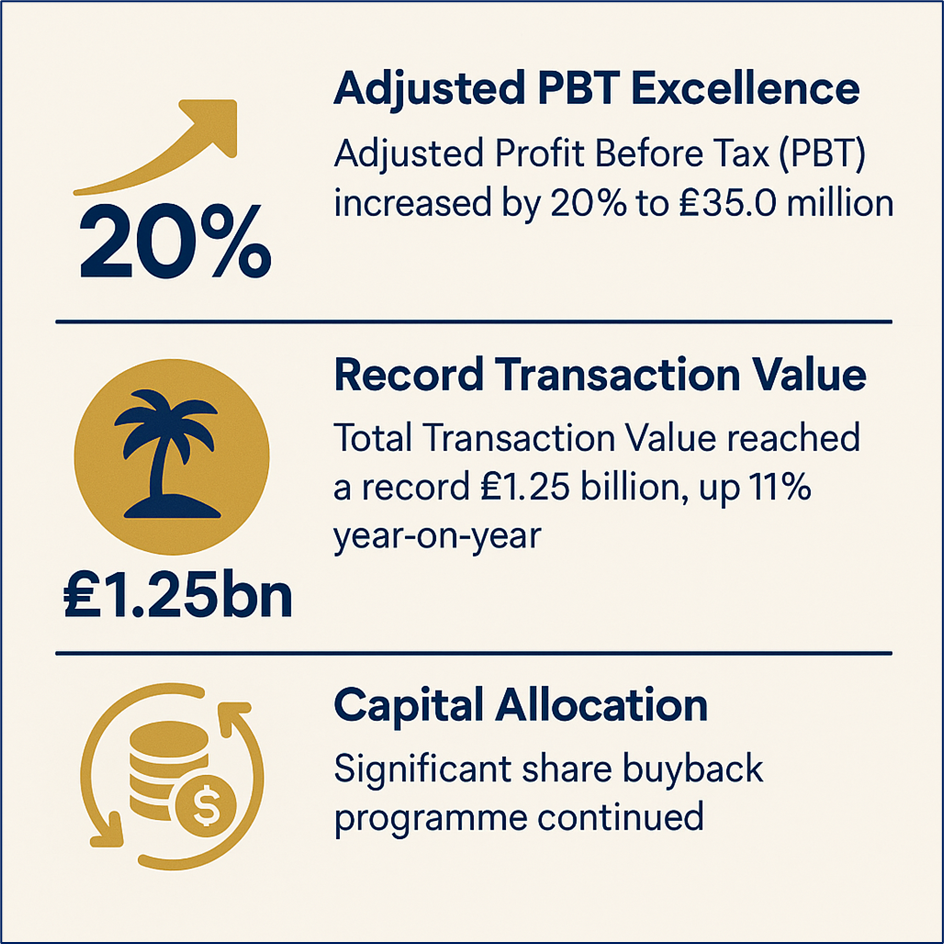

- Adjusted PBT Excellence: Adjusted Profit Before Tax (PBT) increased by 20% to £35.0 million, demonstrating powerful operational leverage and exceeding previous market projections.

- Record Transaction Value: Despite global macroeconomic pressures, Total Transaction Value (TTV)—the gross value of all holidays sold—hit a record £1.25 billion, an increase of 11% year-on-year, underscoring the resilience of consumer demand for beach holidays.

- Capital Allocation: The results confirmed the continuation of the company’s capital return strategy, including a significant share buyback programme, which signals management confidence in future cash flow generation capabilities.

Source: Company Data, Kalkine Group

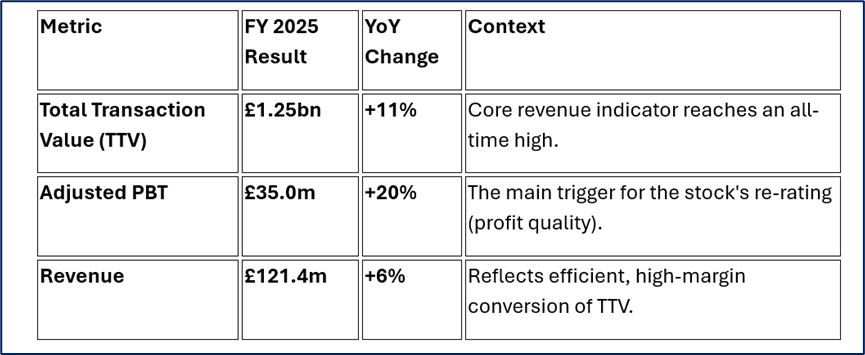

2. Financial and Operational Data Snapshot

The FY25 figures detail a business that has successfully executed its strategy of focusing on the high-margin, scalable B2C model:

Source: Company Data

3. The 'Asset-Light' Engine: OTB's Business Model

OTB’s fundamental operational model is the reason for its superior margins and high cash generation, distinguishing it from traditional travel companies that bear the high fixed costs of owning physical assets (airlines, hotels).

- Dynamic Packaging: OTB functions as a technology platform, instantly assembling packages from real-time flight seats and hotel rooms. This approach means the company carries no inventory risk, avoiding the significant capital expenditure of its competitors.

- Negative Working Capital: This crucial financial mechanism allows OTB to receive customer cash up front and hold it in a protected trust account (ATOL-compliant), while paying suppliers later. This process provides the company with a substantial, interest-free 'cash float,' which it can strategically deploy for growth and capital returns.

- Strategic Focus: The decision to conduct an orderly wind-down of its non-core B2B segment (Classic Collection) was a critical strategic move, enabling management to dedicate resources entirely to the higher-growth, higher-margin B2C platform.

4. Key Operational Drivers & Outlook Momentum

- Premium Strategy: Initiatives, such as offering free airport lounges and fast-track security for 4-star-plus bookings, have successfully shifted the business toward higher-value, more resilient customer segments.

- Geographic Expansion: Investment into the Republic of Ireland has begun to provide a new avenue for growth outside of the mature UK market.

- Forward Visibility: The outlook remains strong, supporting the valuation adjustment. Winter 25/26 forward bookings are currently 15% ahead of the previous year, with early Summer 2026 bookings also reflecting positive momentum. Management restated its ambitious medium-term goal: achieving £100m EBITDA.

5. Risks and Structural Headwinds

While the results are strong, structural factors introduce complexity:

- The Consumer Spend Environment: The current level of robust demand is sensitive to future economic deceleration. If consumer confidence declines or real incomes are further squeezed in 2026, booking volumes could be negatively impacted.

- Digital Dependency: OTB’s model relies heavily on high visibility on search engines. Any change to Google’s core algorithm or a significant increase in paid search costs could substantially impact its efficient customer acquisition model.

- Competitive Landscape: Integrated competitors like Jet2holidays and TUI control the entire customer journey (flight, transfer, hotel). They leverage their vertical integration to offer packages that can be positioned with greater consistency, control, or scale.

- Regulatory Changes: Potential future modifications to consumer protection laws, particularly those governing the handling of customer prepayments (e.g., ATOL reform), could potentially constrain OTB’s negative working capital advantage, affecting cash flow flexibility.

6. Conclusion

The 14% surge in On the Beach (OTB) stock today reflects a positive re-evaluation of the company’s strategic execution and financial strength. The organization successfully navigated a complex operating environment by doubling down on its highly efficient B2C model and effectively eliminating non-core activities. This operational refinement, coupled with consumers’ sustained desire for holidays, has yielded exceptional profit growth and liquidity.

The market’s strong reaction is a clear acknowledgement of management’s successful execution of the 'Asset-Light' thesis. However, the company operates in a constant competitive environment against well-capitalized rivals and remains exposed to macro-economic shifts and digital platform risks. Today’s event confirms OTB’s strong positioning as a technologically advanced operator, but its sustained success will depend on its ability to maintain its marketing efficiency and innovation trajectory.

Source: Trading View, 2 Dec 2025, 9:15 AM GMT

Please wait processing your request...

Please wait processing your request...