Diverging fortunes on the High Street: Why investors are dumping ABF and Tesco despite record sales, and what the Asda crisis means for your portfolio.

Executive Summary: The Great Retail Divergence

The January 2026 trading updates have revealed a stark polarization in the UK retail sector. While heritage grocers Tesco (TSCO) and Marks & Spencer (MKS) delivered record-breaking food sales, the broader market sentiment has been dampened by a shock profit warning from Primark owner Associated British Foods (ABF) and continued deterioration at Asda.

For retail investors, the message is clear: The consumer is still spending, but they are hyper-selective. We are witnessing a "flight to quality" in food and a "pullback on discretionary" in fashion, creating a complex landscape for 2026 portfolios.

- The Winners: Tesco and M&S

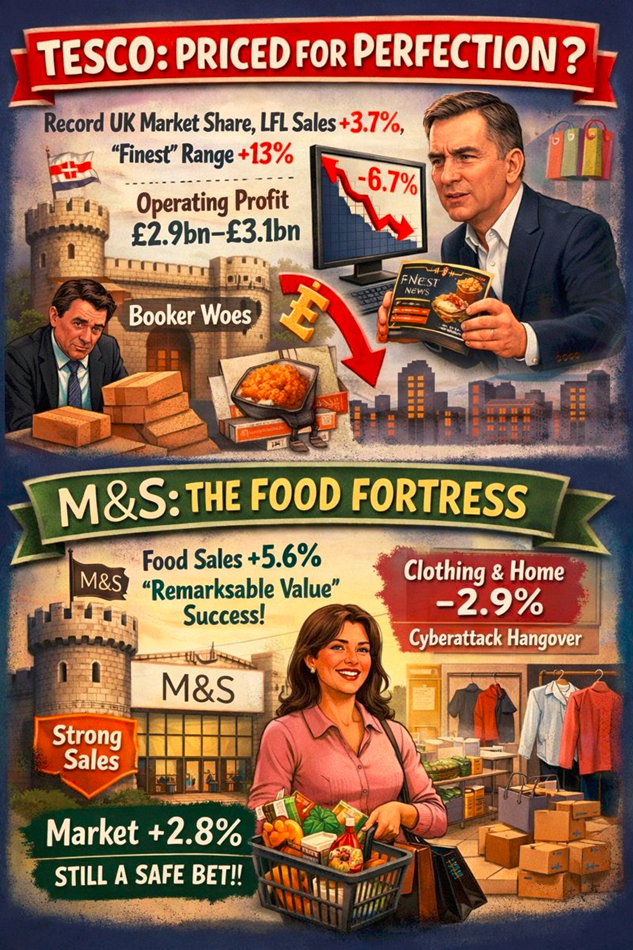

Tesco: Priced for Perfection?

The News: Tesco reported its highest UK market share in over a decade, with like-for-like (LFL) sales rising 3.7% over the "Golden Quarter." CEO Ken Murphy highlighted a massive surge in "Finest" range sales (+13%), signaling that shoppers are treating themselves at home rather than dining out.

The Market Reaction: Despite the bullish operational numbers, Tesco shares slumped ~6-7% immediately following the news.

- Why? The classic "buy the rumor, sell the news." The market had priced in a massive profit upgrade. When Tesco merely guided to the "upper end" of its existing £2.9bn–£3.1bn operating profit range (rather than raising the ceiling), investors took profits. Weakness in the Booker wholesale division also dragged sentiment.

M&S: The Food Fortress

The News: Marks & Spencer continues its renaissance, posting a 5.6% LFL rise in food sales. The "Remarksable Value" campaign has successfully eroded the price perception gap with discounters.

- The Caveat: Clothing & Home sales dipped 2.9%, a hangover from 2025's cyberattack issues and reduced high-street footfall. However, the market reacted positively (+2.8%), valuing the resilience of the food division over the temporary blip in fashion.

Source: Kalkine Group

- The Losers: Asda and ABF

Asda: The Squeezed Middle

Asda is currently the "sick man" of the UK grocery market. Data from Worldpanel reveals sales plummeted ~4-6% over Christmas.

- The Problem: Squeezed between the premium offer of Tesco/Sainsbury's and the relentless price undercutting of Aldi/Lidl, Asda is losing customers in both directions. Without the capital cushion of a public listing (owned by TDR Capital/Issa brothers), its debt pile limits its ability to fight a price war.

ABF (Primark): The Shock Warning

The News: Associated British Foods dropped a bombshell, warning that profits would fall below last year's levels. Primark sales in Europe collapsed 5.7% LFL.

- Analysis: This is a macro signal. Primark is a bellwether for the budget-conscious consumer. If Primark shoppers are pulling back, the "cost of living" crisis has morphed into a "cost of confidence" crisis. ABF shares plunged ~11%, wiping billions off its value.

Source: Kalkine Group

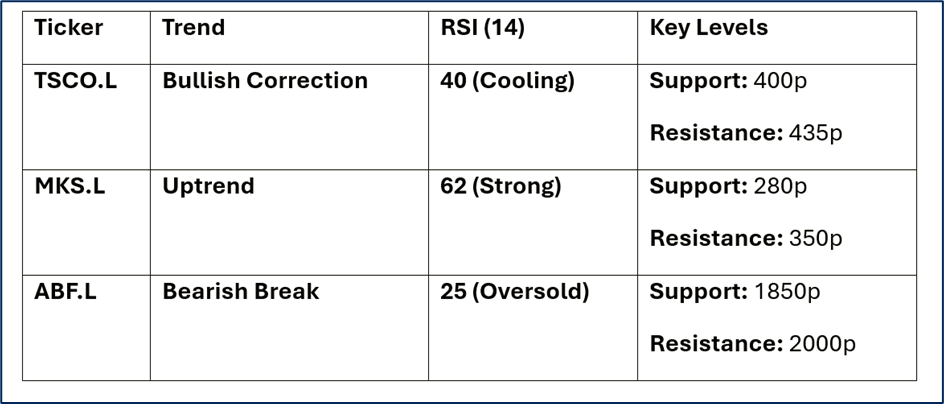

- Technical Analysis Summary (Jan 9, 2026)

Source: Kalkine Group

- Strategy for Retail Investors

Defensive Play: Stick with Food

The 2026 consumer is prioritizing the dinner plate over the wardrobe.

- Action: Tesco remains a core portfolio hold. The recent 7% drop is an attractive entry point for dividend seekers, given their dominant market share and "clubcard moat."

- Dividend Yield: Look for yields around 3.5–4% to cushion volatility.

Value Trap Warning: Avoid High Debt & Discretionary

- Avoid: Companies with high exposure to "middle-market" fashion or high debt piles. The ABF warning suggests the European consumer is weaker than the UK consumer—be wary of UK stocks with heavy EU retail exposure.

- Discounters: While you cannot buy Aldi/Lidl directly, their pressure is hurting Sainsbury's and Morrisons. M&S is the best hedge against discounters because its product is differentiated (you can't buy Percy Pigs at Aldi).

The Contrarian Bet: ABF

- Risky: The 11% drop in ABF brings its P/E ratio down significantly. With a solid balance sheet and diversified sugar/grocery divisions, value investors might start nibbling near 1900p, betting that the Primark slump is cyclical, not structural.

- Outlook 2026: The "Sticky" Year

Global finance houses agree on the theme for 2026: "Sticky Inflation, Picky Consumer."

- Q1 Forecast: Expect a wave of "clearance" sales as retailers like Primark try to shift unsold winter stock. Margins will be compressed.

- Inflation: Grocery inflation has eased to ~4.3%, but wage growth is slowing. This means volume growth (selling more items, not just higher prices) will be the only way to grow profits in 2026. Tesco is winning this volume game; Asda is losing it.

Analyst Take: "The easy money from inflation-driven price hikes is over. 2026 is about market share warfare. Tesco has the war chest; Asda does not."

Please wait processing your request...

Please wait processing your request...