The first trading day of 2026 wasn't just another day at the office for the City of London. As the FTSE 100 briefly eclipsed the historic 10,000-point mark on January 2nd, St. James’s Place (LSE: STJ) emerged as a standout performer, climbing ~2.8% to close at GBX 1,423.50.

For a firm that spent much of 2024 and 2025 in the regulatory "sin bin," this surge signals a powerful redemption arc. Here is the analytical deep dive into why the UK’s largest wealth manager is suddenly back in vogue.

The Big 3: Why STJ Popped on Jan 2nd

Source: Kalkine Group

1. The 'Boring is Beautiful' Rotation

As global investors grew wary of "priced-to-perfection" US tech valuations, the 2026 New Year mantra became value and dividends. St. James’s Place, trading at a significant discount compared to its historical peaks, became a prime target for international capital looking for "cheaper" UK exposure with reliable cash generation.

2. Record-Breaking AUM Milestones

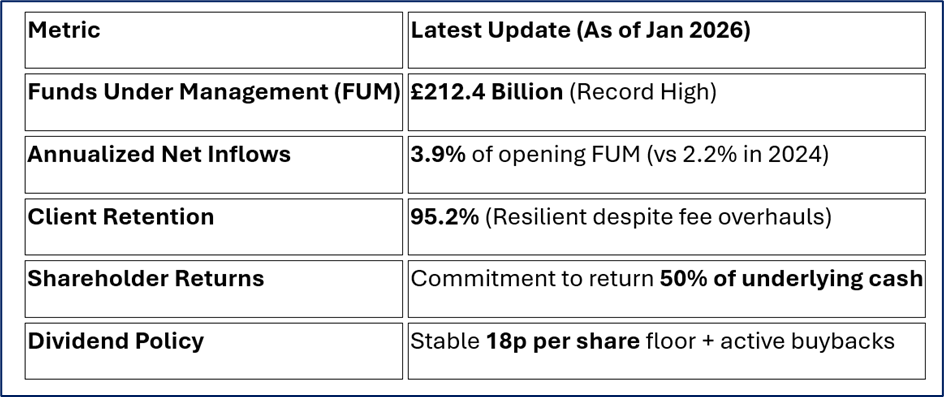

Sentiment was bolstered by the carry-over from late 2025, where STJ officially surpassed the £212 billion milestone in Funds Under Management (FUM). Net inflows have nearly doubled year-on-year, proving that despite fee changes, the "advice-led" model remains a magnet for UK wealth.

3. Operational Lean-Out

The market is finally pricing in the success of the £100 million cost-cutting program. With the "heavy lifting" of the 2024–2025 restructure now in the rearview mirror, investors are eyeing the 2026–2027 "Amplify" phase, which promises higher margins and leaner operations.

The 2026 Business Model: Advice 2.0

SJP has undergone a radical transformation to survive the FCA’s Consumer Duty era.

- Fee Transparency: The controversial "Early Withdrawal Charges" (EWC) are gone for new business. The new "Class S" share structure unbundles advice fees from product charges, making SJP’s costs comparable to DIY platforms like AJ Bell or Hargreaves Lansdown for the first time.

- The Hybrid Shelf: Moving beyond purely active management, the new business model incorporates the Polaris Multi-Index range—a blend of SJP’s active asset allocation with low-cost index-tracking funds to lower the total cost of ownership for clients.

- Tech-Enabled Advice: SJP is now utilizing AI-driven tools (like Synthesia for training and Matillion for data hubs) to reduce manual overhead by up to 75% in certain administrative sectors.

Latest Financial & Operational Pulse

Source: Company Data

SWOT Analysis

Source: Kalkine Group

Strengths

- Scale: Dominant 9% market share of the £2.4 trillion advised UK market.

- Adviser Youth: Average adviser age is 46 (industry average is 58), ensuring long-term "intergenerational" wealth transfer.

- Retention: 95%+ retention suggests high "stickiness" of the face-to-face advice model.

Weaknesses

- Legacy Redress: The £426 million provision for historical service reviews remains a drag on the balance sheet.

- Performance Scrutiny: Some funds still struggle to beat benchmarks after the new fee adjustments.

Opportunities

- The Advice Gap: With UK liquid assets expected to grow 7% p.a. to 2030, the demand for complex tax/pension planning is at an all-time high.

- AI Productivity: Huge potential to use generative AI to automate the "suitability reports" that currently consume adviser time.

Threats

- Regulatory Creep: Any further tightening of Consumer Duty by the FCA could squeeze margins.

- Macro Volatility: A sharp market correction in 2026 would hit FUM-based fee income instantly.

The Risk Radar

While the stock is climbing, two "Grey Swan" events linger:

- Private Credit Contagion: SJP leadership has warned that if the rapidly grown private credit market sours, it could force liquidations in the high-quality bond markets where SJP holds significant client assets.

- Adviser Attrition: If the new, lower-fee structure significantly reduces partner commissions, SJP risks losing its "star" advisers to boutique competitors.

Conclusion

The 2.8% gain on January 2nd reflects a market that is finally looking past SJP’s regulatory trauma and focusing on its fundamental engine: a massive, loyal client base and a leaner cost structure. As the FTSE 100 enters the "10k Era," St. James’s Place appears positioned as a prime beneficiary of the UK’s compounding wealth—provided it can maintain its 95% retention rate under the glare of new transparency.

Please wait processing your request...

Please wait processing your request...