The global mining landscape just felt a tectonic shift. In a move that has sent shockwaves from the London Stock Exchange to the outback of Western Australia, Rio Tinto (LSE: RIO) and Glencore (LSE: GLEN) have confirmed they are in preliminary discussions regarding a potential mega-merger.

If finalized, this "Titan of the Trenches" would create a natural resources behemoth with a combined market capitalization exceeding $200 billion, effectively dethroning BHP as the world's largest miner.

Source: Kalkine Group

The "Copper Rush" of 2026: Why Now?

The timing isn't accidental. As of January 2026, copper prices have breached the $13,000 per tonne mark, driven by an insatiable appetite for AI data centres, electric vehicle (EV) infrastructure, and the global energy transition.

While Rio Tinto is the undisputed king of iron ore, its "copper envy" has been no secret. By absorbing Glencore— a top-10 global copper producer—Rio Tinto would instantly secure a dominant position in the "metal of electrification."

To capture the high-level strategic "alpha" that top fund managers at firms like BlackRock, Vanguard, and Elliott Management look for, you need to look past the headlines and into the "Deal Architecture."

Here are the four strategic pillars currently being discussed in the closed-door meetings of the world's largest institutional investors regarding the Rio-Glencore tie-up.

- The "Arb" of the ESG Pivot: The Coal Carve-Out

Fund managers aren't just looking at the merger; they are looking at the spin-off. Rio Tinto is a "pure-play" green miner (zero coal), while Glencore is the world’s largest thermal coal exporter.

- The Strategy: Analysts at Jefferies and RBC Capital suggest the only way this deal passes the "ESG Filter" of European pension funds is a mandatory divestment of Glencore’s coal assets.

- The Play: Fund managers are looking for a "stapled" deal where Glencore’s coal business is spun off into a separate entity (likely listed in Australia or Johannesburg). This creates a "Bad Bank/Good Bank" dynamic, allowing green funds to hold the new Rio and value funds to harvest the massive cash flows from the "unloved" coal entity.

- The "Trading Brain" vs. "Asset Muscle"

Rio Tinto is traditionally an operational company—they dig it up and ship it. Glencore is a trading powerhouse with a "market-maker" DNA.

- The Strategy: Top managers see this as Rio Tinto buying an "intelligence agency." Glencore’s marketing arm understands global supply chains better than any government.

- The Play: Strategic investors are betting that Glencore’s trading desk can squeeze an extra 2–3% margin out of Rio’s massive iron ore and aluminum volumes through sophisticated hedging and arbitrage that Rio currently lacks.

- The Copper "Scarcity Premium" (The $260B Valuation)

With the combined entity set to control nearly 10% of global copper supply, this isn't just a merger; it's a monopoly on the energy transition.

- The Strategy: Fund managers are pricing in a "Scarcity Premium." As the world faces a projected 10-million-tonne copper deficit by 2040, owning the combined Rio-Glencore is essentially owning the "toll booth" for the AI and EV revolution.

- The Play: Rather than buying the stock at the peak, many managers are using Option Straddles to profit from the volatility leading up to the February 5th "Put Up or Shut Up" deadline.

- Regulatory "Arbiter" Strategy: The China Factor

Because Rio and Glencore are so dominant, the deal lives or dies in Beijing. China is the largest buyer of what these two sell.

- The Strategy: Fund managers are monitoring the ACCC (Australia) and SAMR (China). If regulators demand the sale of specific assets (like Glencore’s Collahuasi stake) to approve the deal, it could trigger a "fire sale" that benefits mid-cap miners like South32 or Antofagasta.

- The Play: Institutional desks are "shorting the spread"—betting that the regulatory hurdles will take 18–24 months, causing the initial merger excitement to cool, providing a better entry point later in 2026.

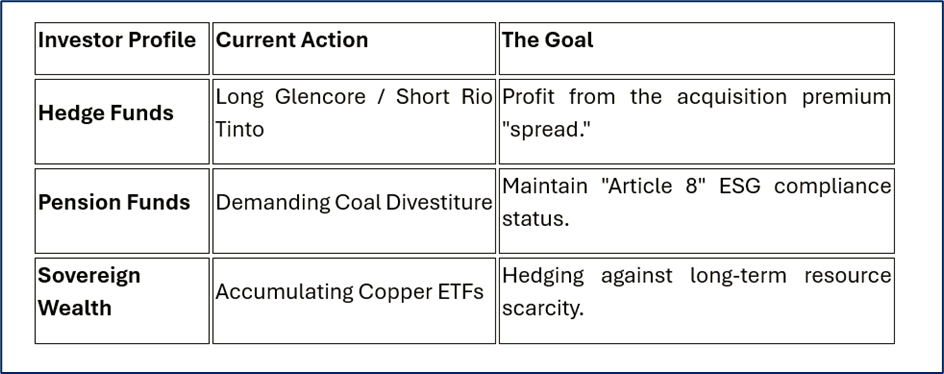

Institutional Cheat Sheet: How the Big Money is Positioned

Source: Market Data

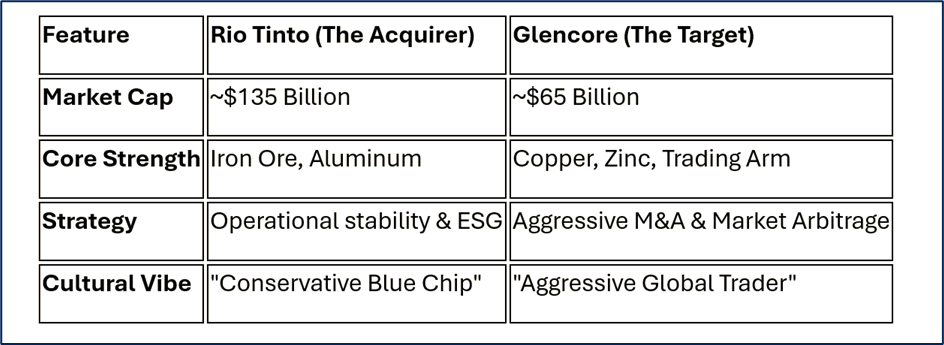

Comparing the Titans: A Tale of Two Balance Sheets - The "Firestorm" for Retail Investors: What to Watch

Source: Kalkine Group

The market is currently in a "price discovery" phase. If you are holding mining stocks, keep an eye on these three triggers:

- The February 5 Deadline: Under UK takeover rules, Rio Tinto must "put up or shut up." Expect extreme volatility as this date approaches.

- Regulatory Hurdles: The Australian Competition and Consumer Commission (ACCC) and Chinese regulators will likely scrutinize the deal for market concentration risks, particularly in copper and iron ore logistics.

- The Divestment Play: If Rio Tinto forces a spin-off of Glencore’s coal business, it could create a "Bad Bank/Good Bank" scenario, offering a potential windfall for value investors willing to hold the "un-ESG" assets.

Bottom Line: This isn't just a merger; it’s a land grab for the 21st century's most critical resources. Whether it results in a "Mining Super-Power" or an "Integration Nightmare" depends entirely on how Rio Tinto handles Glencore’s complex trading culture and controversial coal portfolio.

Please wait processing your request...

Please wait processing your request...