As the global transition to a green economy accelerates, two titans of the FTSE 100 have emerged as the vanguard of the mining sector’s latest resurgence. Anglo American and Antofagasta have defied broader market volatility to deliver staggering double-digit returns within a single month, a feat fueled by a structural "supercycle" in base and precious metals.

Driven by an insatiable demand for copper—the "nerve system" of the energy transition—and a strategic pivot toward operational simplification, these companies are no longer viewed as mere cyclical plays but as essential structural anchors in the modern investment portfolio.

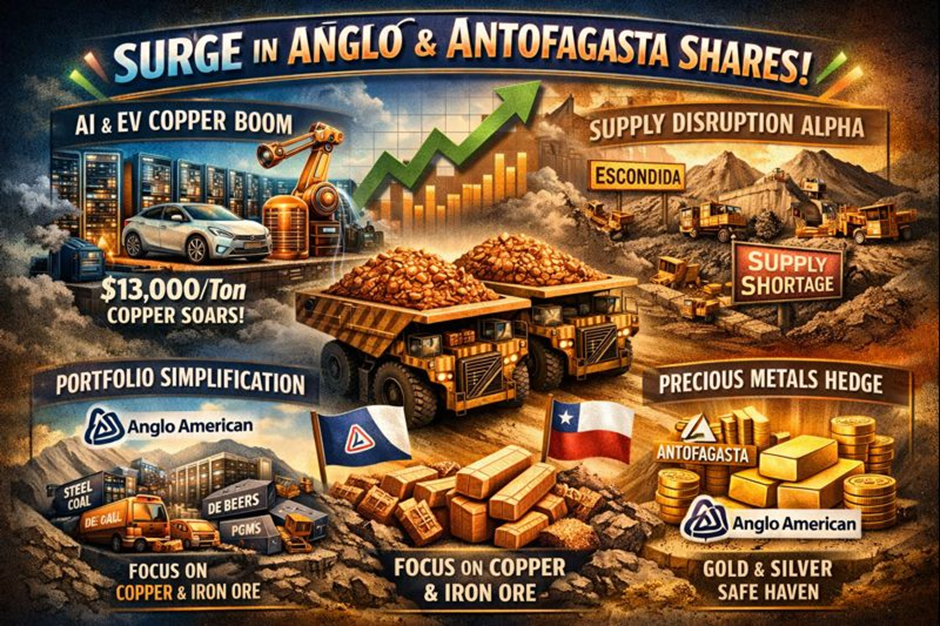

Latest Key Reasons for Surge & Drivers

Source: Kalkine Group

The recent surge in Anglo American and Antofagasta shares is underpinned by a confluence of macroeconomic and industry-specific factors:

- The AI and Electrification Nexus: Copper has become the primary beneficiary of the AI data center boom and the global shift toward EVs. Industry reports indicate that copper prices breached the $13,000 per ton mark in early 2026, creating massive tailwinds for pure-play or copper-heavy miners.

- Supply Disruption Alpha: Significant output reductions at major global mines (such as Escondida and Grasberg) have tightened the global market. Antofagasta, with its concentrated Chilean assets, has capitalized on this scarcity premium.

- Anglo American’s Portfolio Simplification: Investors have cheered Anglo’s aggressive "Transition Year" strategy, which involves divesting non-core assets (Steelmaking Coal, De Beers diamonds, and PGMs) to focus on a high-margin "Simplified Portfolio" centered on Copper and Premium Iron Ore.

- Precious Metals Hedge: Antofagasta’s significant gold by-product credits and Anglo’s exposure to precious metals have provided a secondary growth engine as central banks continue to diversify into gold amid geopolitical fragmentation.

Current Business Models

Anglo American (AAL)

The company is currently undergoing a radical transformation. Its "FutureSmart Mining" model focuses on high-quality, long-life assets that provide "see-through value."

- Simplified Core: Transitioning to a model where Copper accounts for over 60% of the portfolio.

- Quality Over Quantity: Focusing on premium iron ore (Minas-Rio and Kumba) and crop nutrients (Woodsmith project) which command higher margins and lower carbon intensity.

Antofagasta (ANTO)

Antofagasta operates as a high-conviction copper specialist with a business model rooted in Chilean operational excellence.

- Pure-Play Exposure: One of the few major miners offering concentrated exposure to copper with significant gold and molybdenum by-products.

- Infrastructure Advantage: Leveraging established desalination plants and proprietary transport networks to lower the "net cash cost" of production.

Latest Financial, Operational, and Dividend Updates

Anglo American

- Financials: Reported a strong EBITDA margin of 43% for its "go-forward" business in the latest half-year report. Net debt was managed at $10.8 billion prior to portfolio simplification proceeds (Anglo American H1 2025 Report).

- Operations: Q3 2025 production showed strong momentum in Copper (up 1% YoY) and a significant 140% jump in Manganese as operations normalized. Minas-Rio iron ore guidance was upgraded to 23–25 million tonnes (Anglo American Q3 Production Report).

- Dividends: Announced a provisional 2026 dividend timetable with the final dividend announcement set for February 20, 2026, and payment on May 6, 2026 (Investegate / Company Announcement).

Antofagasta

- Financials: Management noted that margins expanded to some of the highest levels in years during H1 2025, with EPS more than doubling compared to the prior period (IG/City Index).

- Operations: Copper production in 9M 2025 was 476,600 tonnes (up 3% YoY). Notably, gold production surged 22% year-on-year, providing massive "by-product credits" that lowered net cash costs to $1.24/lb (Antofagasta Q3 2025 Production Report).

- Dividends: A final dividend of approximately 12.26p (16.6c) is expected to be declared in February 2026, following a strong 2025 payout cycle (DividendMax).

Latest SWOT Analysis

Source: Kalkine Group

Outlook and Risks

The outlook for both firms remains tethered to the "policy-driven business cycle" of 2026. Experts predict that as governments prioritize mineral security, these miners will see increased state-backed support and preferential financing. Anglo American is expected to emerge as a leaner, higher-margin entity by the end of 2026 as its divestment program concludes. Antofagasta is poised to benefit from its Centinela expansion and increased desalination capacity.

Risks include a potential slowdown in Chinese property markets (impacting iron ore), volatile national policies in South America, and the "cost of capital" if interest rates remain higher for longer than anticipated. Furthermore, any rapid advancement in "deep-sea mining" or lab-grown alternatives (for Anglo’s exiting diamond business) could shift market sentiment.

Compelling Conclusion

The double-digit ascent of Anglo American and Antofagasta serves as a powerful signal that the "Age of Metals" has arrived. By aligning their business models with the inescapable demands of decarbonization and digital infrastructure, these companies have transformed from traditional industrial stocks into high-growth catalysts. While operational and geopolitical risks remain inherent to the terrain, the structural scarcity of copper and the strategic pivot toward portfolio simplicity suggest that the current surge is not merely a seasonal spike, but a fundamental re-rating of the sector’s value in the global economy.

Please wait processing your request...

Please wait processing your request...