Riding the Post-Spinoff Wave: Key Drivers Behind the Early Market Melt-Up

The recent 5.33% intraday surge in the FTSE 100 listed shares of The Magnum Ice Cream Company (LSE: MICC) on December 11, 2025, marked a significant moment for the newly independent global ice cream powerhouse. Spun off from consumer goods giant Unilever (ULVR) just days prior, the stock experienced volatile but ultimately positive early trading. This surge, while likely amplified by short-term market dynamics, underscores strong investor confidence in the company's long-term strategy as the world's largest ice cream pure-play.

The company's primary listing is in Amsterdam, with a secondary listing on the London Stock Exchange (LSE) under the ticker MICC, making it a keenly watched stock among FTSE investors.

Key Reasons and Drivers for the Stock Surge

The notable single-day jump can be attributed to a confluence of market forces and the company's compelling fundamental narrative:

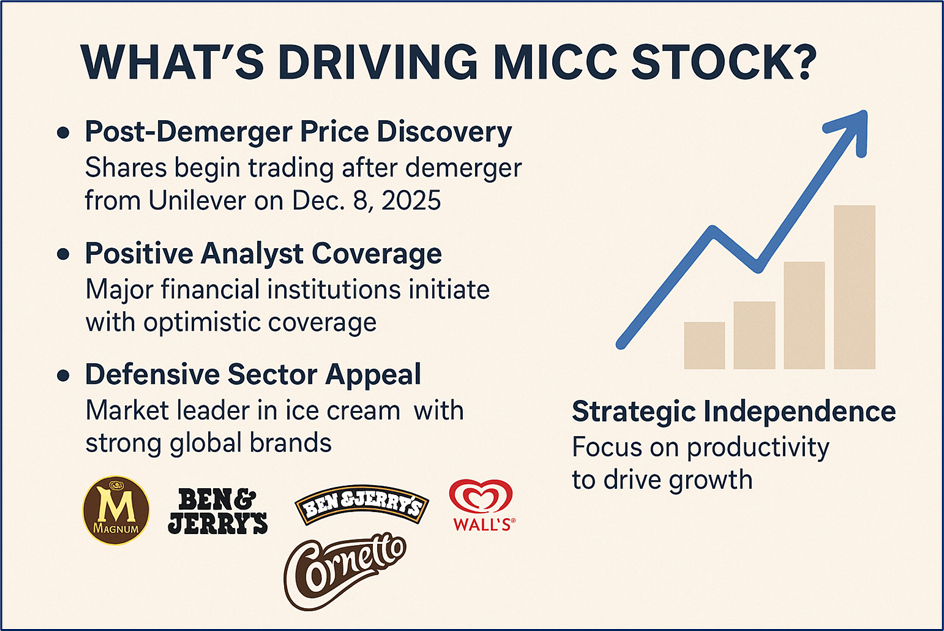

- Post-Demerger Price Discovery and Valuation Adjustment: The most immediate driver is the process of price discovery following the demerger from Unilever on December 8, 2025. Shares were distributed to existing Unilever shareholders (1 MICC share for every 5 ULVR shares held). The initial days see volatility as the market properly values the new entity. The surge suggests the market, after initial soft trading, quickly concluded the stock was undervalued relative to its peers and future prospects.

- Positive Analyst Coverage and Fair Value Estimates: Major financial institutions-initiated coverage with optimistic fair value estimates. This positive external validation boosted investor sentiment.

- Defensive Sector Appeal and Market Leadership: As a pure-play in the consumer defensive packaged foods sector, MICC owns an impressive portfolio of global, iconic brands like Magnum, Ben & Jerry's, Cornetto, and Wall's. This collection commands a dominant 21% share of the global retail ice cream market. In an uncertain economic environment, defensive stocks with strong brand power are often highly prized.

- Focus on Strategic Independence and Productivity: The separation allows a refreshed, focused management team to execute a category-specific strategy. Investors are cheering the ambitious €500 million productivity program aimed at eliminating supply chain and overhead inefficiencies. This is expected to drive annual adjusted EBITDA margin expansion of 40–60 basis points over the medium term.

Source: Kalkine Group

Latest Business Updates and Strategic Outlook

The Magnum Ice Cream Company enters the market as a fully functioning, profitable, and cash-flow-positive entity, having operated standalone since July 1, 2025.

Business Updates:

- Successful Triple Listing: Achieved initial admission to trading on Euronext Amsterdam (primary), London Stock Exchange, and New York Stock Exchange on December 8, 2025.

- Revenue Scale: Generated substantial revenues of €7.9 billion in the last financial year (with €4.5 billion in H1 2025), translating into a solid 16.5% adjusted EBITDA margin.

- Inclusion in AEX Index: The company confirmed its immediate inclusion in the AEX index on Euronext Amsterdam, a testament to its scale and market importance.

Source: Kalkine Group

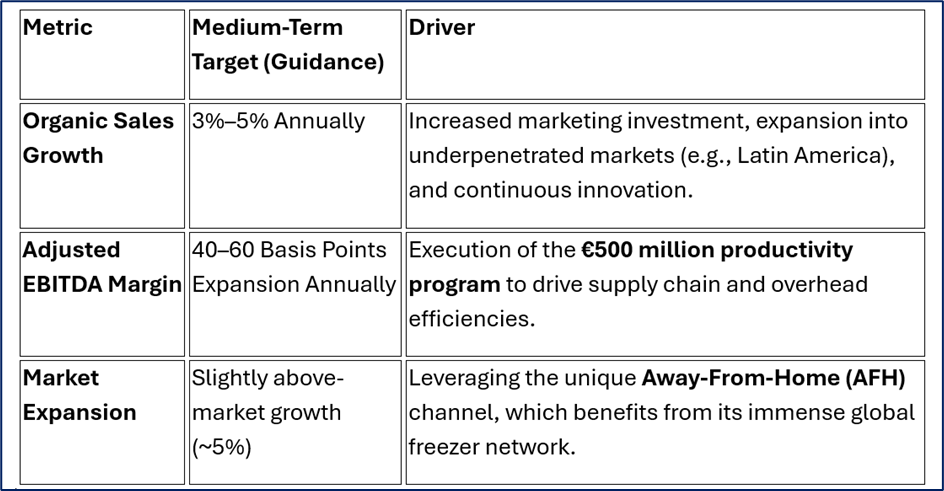

Outlook and Growth Strategy:

The company has outlined a clear medium-term strategy focused on accelerated growth and margin improvement:

Source: Company Data, Kalkine Group

Business Model and Competitive Advantage

MICC’s business model is built on an unparalleled combination of iconic branding and complex infrastructure.

Core Model Pillars:

- Iconic Brand Portfolio: Ownership of some of the most recognized ice cream brands globally, allowing for premium pricing and consumer loyalty.

- World-Class Cold Chain: The business requires a highly complex, capital-intensive cold-chain infrastructure for manufacturing, storage, and distribution—a significant barrier to entry for competitors.

- Freezer Cabinet Strategy (The "Moat"): The company owns and strategically places approximately 3 million branded freezer cabinets worldwide. This physical, in-store visibility is a massive distribution advantage, particularly for impulse-driven purchases in the lucrative Away-From-Home channel.

This combination grants MICC a powerful, wide economic moat—a sustainable competitive advantage—in a challenging, low-growth category.

Key Risks and Headwinds

Despite the initial enthusiasm, investors must acknowledge several risks inherent to the business:

- Index-Tracking Fund Selling Pressure: As the stock is not a FTSE 100 constituent (its main listing is in Amsterdam), UK-focused index-tracking funds that received the shares as part of the spin-off are often mandated to sell the stock. This structural selling creates temporary downward pressure on the share price in the short term.

- The GLP-1 Consumption Risk: The rise of weight-loss drugs like GLP-1 agonists (e.g., Ozempic) poses a potential long-term, secular risk. These drugs have been shown to reduce cravings for high-calorie, sweet foods like ice cream, which could dampen future consumption growth.

- Dividend Hiatus: The company has communicated that it will not initiate dividend payments until 2027 as it prioritizes reinvestment and balance sheet stability in its new standalone life. This may deter income-focused investors.

- Unilever Overhang: Unilever retains a 19.9% voting stake in MICC, which it intends to wind down gradually over the next five years. Future sales of this large block of shares could act as an "overhang" on the stock, limiting significant price appreciation during the sell-down period.

Conclusion: A Sweet Spin-Off with a Strong Foundation

The 5.33% surge in The Magnum Ice Cream Company's stock on the LSE is a strong vote of confidence, signaling that institutional investors are beginning to price in the value of an undervalued asset freed from the constraints of its former parent.

The immediate drivers are the unwinding of short-term selling from the demerger and the market's positive reception to a strong, focused management strategy. In the long term, MICC's unmatched brand portfolio, its global-scale cold-chain infrastructure, and the massive leverage of its 3 million freezer network give it a defensible leadership position.

While short-term selling pressure from index funds and the distant shadow of the GLP-1 consumption trend present genuine risks, the company's clear strategy for margin accretion and market-beating sales growth makes it a compelling growth story in the defensive consumer staples sector. The initial surge suggests the market is ready to pay a premium for this newfound independence and focus.

Source: Trading View, 11 December 2025, 12:50 PM GMT

Please wait processing your request...

Please wait processing your request...