The UK housing market shifted gears on December 17, 2025, as Barratt Redrow (LSE: BTRW), the nation’s largest housebuilder, closed ~3.6% at GBX 375.90. While the broader FTSE 100 gained a solid 0.9%, Barratt Redrow’s outperformance signalled a major "risk-on" move from institutional and retail investors alike.

But what actually moved the needle? Let’s dive into the drivers, the business model, and the SWOT analysis of this newly merged titan.

- The Dec 17 Catalyst: A "Goldilocks" Inflation Print

Source: Kalkine Group

The primary driver for the jump was a sharper-than-expected fall in UK inflation.

- The Data: Headline CPI cooled to 3.2% (down from 3.6% in October).

- The Reaction: This data effectively "green-lit" a Bank of England interest rate cut scheduled for December 18.

- Why it matters for BTRW: Lower interest rates are the "lifeblood" of housebuilders. They reduce mortgage costs for buyers—stimulating demand—and lower the cost of capital for construction projects.

- Latest Business Updates: Post-Merger Momentum

Since the transformative merger between Barratt Developments and Redrow in late 2024, the "New Co" has been moving at light speed to prove the deal’s worth.

- Synergy Targets Smashed: The group originally targeted £100m in annual cost savings. As of late 2025, they have already confirmed £80m of these, with £45m expected to hit the bottom line in FY26.

- Completions Guidance: Despite a sluggish early 2025, the group remains on track to deliver 17,200 to 17,800 homes for the full year.

- Cash is King: The company maintains a powerhouse balance sheet with net cash of £772.6m, supporting an ongoing £100m share buyback program.

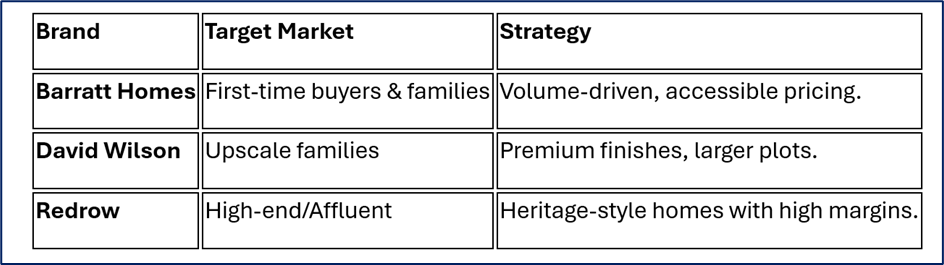

- The Business Model: A Three-Pronged Strategy

Barratt Redrow doesn't just build "houses"; it operates a diversified brand portfolio designed to capture every segment of the UK market:

Source: Company Data

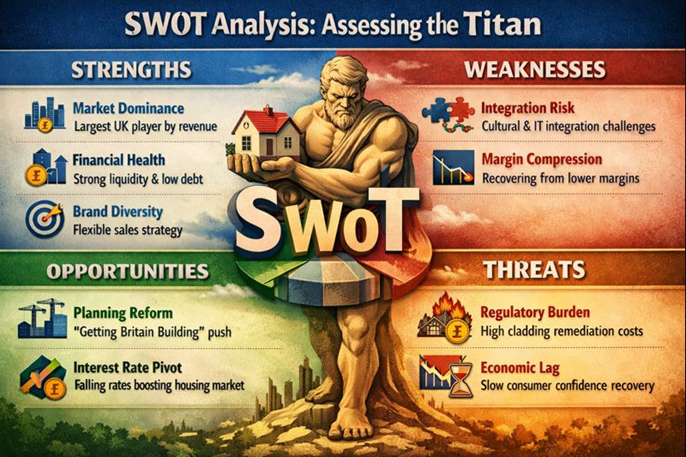

- SWOT Analysis: Assessing the Titan

Source: Kalkine Group

Strengths

- Market Dominance: Largest UK player by revenue; massive procurement power reduces build costs.

- Financial Health: Exceptionally strong liquidity and low debt compared to historical cycles.

- Brand Diversity: Ability to pivot sales focus if one demographic (e.g., first-time buyers) slows down.

Weaknesses

- Integration Risk: Merging two corporate cultures and IT systems is complex and can lead to short-term friction.

- Margin Compression: While improving, adjusted gross margins (approx. 15.7%) are still recovering from peak 2022 levels.

Opportunities

- Planning Reform: The UK government's focus on "getting Britain building" could unlock stalled land banks.

- Interest Rate Pivot: We are entering a cycle of falling rates, which historically leads to multi-year rallies in housing stocks.

Threats

- Regulatory Burden: Building safety remediation costs (cladding issues) remain a persistent multi-million-pound drain on cash.

- Economic Lag: Even if rates fall, the "lag effect" means consumer confidence may take months to fully recover.

- Key Risks to Watch

- Mortgage Volatility: If inflation proves "sticky" in early 2026, the Bank of England may pause rate cuts, dampening the recent rally.

- Build Cost Inflation: While currently stable at 1–2%, any spike in energy or labor costs could squeeze margins.

- Planning Bottlenecks: Local authority delays remain the #1 hurdle to reaching the group's medium-term goal of 22,000 homes per year.

Conclusion: A Giant Awakening?

Barratt Redrow’s 3.6% jump on December 17 wasn't just a random fluctuation; it was a market vote of confidence in a business that has successfully integrated a massive acquisition and is now sitting at the "starting blocks" of a new interest rate cycle. With a massive land bank and a £100m buyback supporting the share price, the group is positioned as the primary proxy for a UK economic recovery.

Source: Trading View, 17 December 2025

Please wait processing your request...

Please wait processing your request...