Is this the FTSE 250’s hidden gem? Unpacking the 24 Dec 2025 surge

Pan African Resources (LSE: PAF) is catching eyes this Christmas Eve, trading up ~1% to GBX 122.40. While a 1% move might seem modest in isolation, it’s the why beneath the surface that signals a much bigger story. With gold smashing through $4,500/oz, PAF isn't just riding the wave—it’s building a surfboard.

Here is your analytical, no-nonsense breakdown of why this mid-tier miner is glittering right now.

- The Golden Catalyst: Why the Stock is Moving

The 1% bump on December 24, 2025, isn't random noise. It is the result of a "perfect storm" of macro tailwinds and operational execution:

Source: Kalkine Group

- The $4,500+ Gold Super-Cycle: Gold prices are hovering near $4,565/oz. For a producer like PAF, which has significant operational leverage, every $10 increase in the gold price flows almost directly to the bottom line.

- The "Debt-Free" Countdown: The market is pricing in the reality that PAF is on track to be net debt-free by February 2026. In a high-interest-rate world, a debt-free miner paying dividends is a rare unicorn.

- Main Market Mojo: Having recently graduated to the Main Market of the London Stock Exchange (LSE) in late 2025, PAF is now attracting institutional flows that couldn't touch it when it was on AIM. The volume is stickier, and the buying is deeper.

If you think PAF is just another deep-level South African digger, you’re looking at an outdated model. The 2025 business model has pivoted:

- Tailings Titans (Low Cost, Low Risk): The core profit engine is now surface tailings retreatment (recycling old mine dumps). This is safer, cheaper, and cleaner than deep mining. The Mogale Tailings Retreatment (MTR) plant is the crown jewel here, ramping up to 60,000oz/year by this month.

- Geographic De-Risking: PAF has officially gone international. The commissioning of the Nobles Project in Australia (acquired via Tennant Consolidated) adds ~50koz of production outside of South Africa, significantly reducing the "SA Risk Discount" investors usually apply.

- Energy Independence: With solar plants at Evander and Barberton, they are insulating themselves from grid instability, lowering costs and carbon footprints simultaneously.

- Financial & Operational "Report Card" (Late 2025 Update)

- Production: Guidance is strong. The group is eyeing 275k - 292k oz for the full financial year, fueled by the new Australian ounces and the MTR ramp-up.

- MTR Success: The Mogale plant came in ahead of schedule and under budget. They are already studying an expansion (the Soweto Cluster) to push this complex to nearly 100k oz/year.

- Dividends: PAF remains a dividend aristocrat among mid-caps. With record cash flows, the payout ratio is healthy, and the yield is attractive relative to the wider FTSE 250.

- Evander 8 Fast-Track: High gold prices have allowed them to fast-track capital expenditure at the Evander underground mine, extending its life and boosting output sooner than planned.

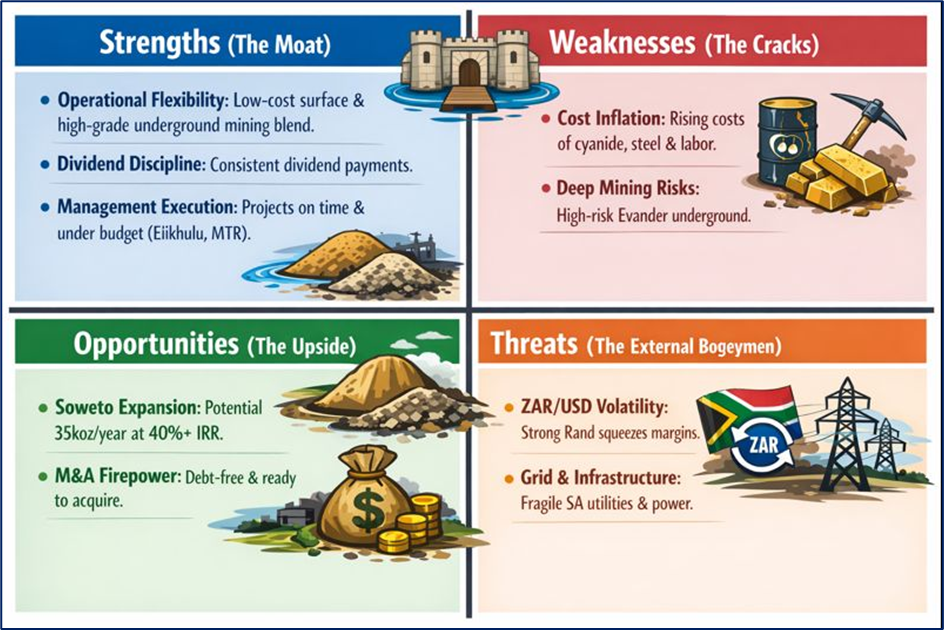

- SWOT Analysis

Source: Kalkine Group

Strengths (The Moat)

- Operational Flexibility: A mix of low-cost surface mining and high-grade underground mining allows them to blend costs effectively.

- Dividend Discipline: A long track record of paying dividends, even in leaner years.

- Management Execution: They build plants on time and under budget (Elikhulu, and now MTR). That is rare in mining.

Weaknesses (The Cracks)

- Cost Inflation: While gold is up, so are the costs of cyanide, steel, and labor. Margins are great, but cost creep is a silent killer.

- Deep Mining Risks: The Evander underground operations, while high-grade, are technically challenging and carry higher safety risks than the surface dumps.

Opportunities (The Upside)

- The Soweto Expansion: If approved, the Soweto Tailings Retreatment (STR) circuit could add another 35koz/year with an Internal Rate of Return (IRR) of 40%+ at current gold prices.

- M&A Firepower: Being debt-free gives them a war chest to buy more distressed assets or juniors, just like they did with Tennant.

Threats (The external Bogeymen)

- ZAR/USD Volatility: A strengthening South African Rand (ZAR) is actually bad for PAF, as they sell in USD but pay costs in ZAR. If the Rand rallies, their margins squeeze.

- Grid & Infrastructure: Despite solar investments, they still rely on South African infrastructure (water/rail/power), which remains fragile.

- The Risks: What Could Go Wrong?

Don't get blinded by the sparkle. Here is the bear case:

- Gold Price Correction: If gold drops back below $3,000, the aggressive valuation premiums erode quickly.

- Execution Risk in Australia: Operating in a new jurisdiction (Australia) brings new regulatory and labor challenges they haven't faced before.

- The "priced in" problem: The stock has had a massive run in 2025 (up over 160% YTD by some metrics). Much of the good news (MTR, high gold) might already be in the price.

Conclusion

Pan African Resources is no longer just a "South African gold play." It is evolving into a diversified, mid-tier producer with a focus on high-margin, safe surface ounces. The ~1% rise on Dec 24 is a quiet confirmation that the market believes in the "Debt-Free + Growth" narrative heading into 2026.

They are generating cash, paying dividends, and expanding production—a trifecta that is hard to find in the FTSE 250.

Please wait processing your request...

Please wait processing your request...