As of January 20, 2026, Critical Metals (LSE: CRTM / NASDAQ: CRML) is experiencing an extraordinary period of price discovery, propelled by a perfect storm of geopolitical tension, strategic partnerships, and a global scramble for non-Chinese rare earth supplies. The stock has surged significantly, leaving investors to weigh the massive potential of its Greenland assets against the risks of a "Momentum Trap."

Critical Metals: Latest Drivers as of January 20, 2026

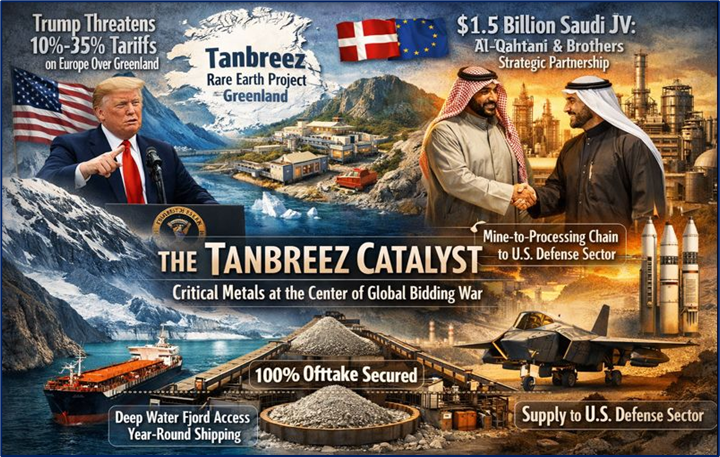

Source: Kalkine Group

- Geopolitical Spark: The primary driver today is the escalating tension between the U.S. and Denmark over Greenland. President Trump’s recent announcement of potential 10% to 25% tariffs on European nations—unless an agreement is reached for the U.S. to acquire or secure mineral rights in Greenland—has put Critical Metals’ Tanbreez project at the center of a global bidding war.

- The Saudi Power Move: Last week’s non-binding term sheet with a leading Saudi Arabian industrial conglomerate (Al-Qahtani & Brothers) for a $1.5 billion joint venture is a game-changer. This facility will refine 25% of Tanbreez's output, creating a strategic "Mine-to-Processing" chain that terminates in the U.S. defense sector.

- Offtake Certainty: As of today, the company has successfully secured offtake arrangements for 100% of the rare earth concentrate expected from Tanbreez, providing long-term revenue visibility that was previously absent.

- The "Tanbreez Catalyst": The project is one of the world's largest rare earth deposits. Its unique "deep water fjord" access allows for year-round shipping, a logistics advantage that drastically lowers the "Greenland risk" usually associated with Arctic mining.

Current Price and Technical Analysis (Jan 20, 2026)

The stock (CRML/CRTM) is currently trading near $19.40 (NASDAQ) and 16.50p - 19.00p (LSE) as of the market sessions today. After a 76% surge in the last month, the technical profile is characterized by extreme momentum. The price is currently trading over 60% above its 200-day moving average, which often signals a "Momentum Trap" or an overextended rally in the short term.

However, the breakout above previous resistance at $17.50 on high volume suggests that the market is repricing the stock based on structural changes (the Saudi JV) rather than just speculative froth. The Relative Strength Index (RSI) is hovering near 86, indicating overbought conditions that could lead to a healthy consolidation or "pullback to the mean" before the next leg up.

Latest Analyst Ratings & Upgrades

- Consensus Rating: The current analyst consensus remains a "Strong Buy" among the few specialized firms covering the stock, though the price targets are struggling to keep up with the vertical move.

- Clear Street: Analyst Tim Moore recently initiated coverage with a Buy rating, calling it a "unique way to gain exposure" to high-value magnets and defense-grade metals.

- Valuation Gap: While some analysts maintain a conservative price target of $12.00 to $14.00, these targets largely reflect the "pre-Saudi JV" fundamentals. Markets are currently ignoring these trailing targets as "lagging indicators" while pricing in the $1.5 billion refinery deal.

- Smart Money Sentiment: Institutional flow from commodity-focused hedge funds has increased, with many viewing CRML as a "Sovereignty Trade"—an asset that gains value as global trade protectionism increases.

Business Model & Operational Update

- Strategic Asset Portfolio: The business model has shifted from pure exploration to a fully integrated supply chain developer. The flagship Tanbreez Project (Greenland) provides the raw material (HREE and eudialyte), while the Wolfsberg Lithium Project (Austria) serves as Europe’s first fully permitted lithium mine.

- Revenue Streams: Unlike traditional miners, CRML is positioning itself to sell construction materials (by-products) early on to ensure near-term profitability, while the long-term value lies in the 27% High Rare Earth Element (HREE) concentration.

- Financial Update: The company recently issued Convertible Loan Notes to bolster liquidity ahead of the 2026 construction phase. Management has scheduled a high-stakes webcast for January 22, 2026, where they are expected to finalize the Saudi JV details and provide a definitive timeline for the "One Project, One Process" framework in North American collaborations.

Latest Dividend & Valuation Analysis

- Dividend Status: As of today, January 20, 2026, Critical Metals does not pay a dividend. As a development-stage mining company, all capital is being re-invested into exploration, permitting, and the $1.5 billion refinery infrastructure.

- Valuation Metric: The current market capitalization of approximately $2.08 billion is considered "asymmetric" by many fund managers. When compared to the multi-billion dollar strategic reserves being proposed by the U.S. and EU, the stock is viewed as undervalued on a "Replacement Value" basis but overvalued on a "Current Cash Flow" basis (which is currently zero).

- Peer Comparison: CRML is trading at a premium to other micro-cap miners but at a significant discount to established defense-grade suppliers like MP Materials or Lynas during their peak growth phases.

Outlook, Risks, and Conclusion

The 2026 Outlook

The outlook is exceptionally bullish from a geostrategic perspective. With the U.S. Strategic Resilience Reserve likely to unlock Pentagon contracts for execution-ready platforms, CRML is "in the right place at the right time." The target for first production remains 2028, with 2026 serving as the "year of construction and final permitting."

Key Risks

- Geopolitical Whiplash: While Trump’s Greenland interest drives the price up, any diplomatic resolution that ignores CRML’s assets could lead to a rapid "de-risking" sell-off.

- Dilution: The reliance on convertible loan notes and the need for massive capex for the Saudi refinery could lead to future shareholder dilution.

- Execution Risk: Moving from a "term sheet" to a finalized, operational $1.5 billion facility in Saudi Arabia involves significant regulatory and engineering hurdles.

Conclusion

Is it still "undervalued" to buy after a 76% surge? For the retail speculator, the stock is technically overbought and carries high short-term risk. For "Smart Money" and long-term fund managers, the current $2 billion valuation may still represent a bargain if the company successfully becomes the primary non-Chinese supplier for the Western defense complex. The January 22nd update will likely be the deciding factor for the next 50% move in either direction.

Please wait processing your request...

Please wait processing your request...