HSBC Holdings: Banking Giant Surges 2.3% on Strategic Milestones

HSBC Holdings (LSE: HSBA) demonstrated significant market strength on January 27, 2026, with its share price climbing 2.3% in London trading, marking it as a top performer within the FTSE 100 index. This upward momentum reflects a confluence of positive macroeconomic data from Asia and the successful execution of the group's long-term restructuring plans.

As the bank moves closer to its full-year 2025 results announcement scheduled for late February, investors are reacting to the bank’s strengthened grip on its Hong Kong operations and its resilience in a shifting interest rate environment.

Latest Drivers and Reasons for the Surge

Source: Kalkine Group

- Hang Seng Privatization Success: A primary catalyst for today’s movement is the finalization of the Hang Seng Bank privatization. As of January 27, 2026, Hang Seng Bank shares are officially withdrawn from the Hong Kong Stock Exchange, making it a wholly-owned subsidiary of the HSBC Group. This move is expected to streamline operations and enhance capital efficiency across the group’s core Asian hub (HSBC Investor Relations).

- Mainland China Economic Sentiment: Markets were buoyed by fresh data showing that China’s industrial profits rose in 2025 for the first time in four years. A sharp rebound in December has renewed confidence in the region’s earnings recovery, directly benefiting HSBC given its heavy exposure to Chinese trade and corporate lending.

- Deepened Market Connectivity: Positive sentiment followed pledges from China's central bank to deepen financial market connectivity with Hong Kong. As the dominant player in this corridor, HSBC is positioned as the primary beneficiary of increased cross-border capital flows.

- Global Interest Rate Outlook: Investors are recalibrating expectations ahead of this week’s Federal Reserve meeting. While the broader market remains cautious, HSBC’s "structural hedge" strategy has successfully mitigated the impact of falling rates in certain regions, protecting its net interest income (NII) targets (HSBC Q3 2025 Earnings Update).

Current Business Model and Operational Updates

HSBC has transitioned into a "Wealth-First" global bank, pivoting away from lower-margin retail banking in the West to focus on high-growth markets in Asia and the Middle East.

- Strategic Market Reallocation: The group has largely completed its exit from non-core markets, including the sale of its Canadian and Argentinian businesses. In January 2026, reports also surfaced regarding the potential sale of its Singapore insurance unit to further sharpen its focus on wealth management (Sharecast News).

- Four-Pillar Structure: Effective January 1, 2025, the bank simplified its organizational structure into four main businesses: Hong Kong, UK, Corporate & Institutional Banking (CIB), and International Wealth & Premier Banking (IWPB).

- Digital and AI Integration: The 2026 HSBC Innovation Horizons Report highlights a massive shift in capital allocation toward AI-driven automation. The bank is currently deploying AI to enhance private banking advisory and automate internal compliance processes to meet its $1.5 billion annualized cost-reduction target by the end of 2026.

Financial and Dividend Updates (Source: HSBC Holdings)

- Profitability Targets: HSBC has maintained its guidance for a return on average tangible equity (RoTE) in the "mid-teens" for 2026. This is supported by an anticipated banking net interest income (NII) of approximately $42 billion for the 2025-2026 cycle.

- Capital Strength: The Common Equity Tier 1 (CET1) ratio remains robust, hovering within the target range of 14% to 14.5%, even after aggressive capital returns to shareholders.

- Dividend Policy: The bank remains committed to a payout ratio of 50% for 2025/2026. With the Hang Seng privatization now complete, the group has consolidated its dividend-paying capacity. The final dividend for the 2025 fiscal year is expected to be announced on February 25, 2026 (HSBC Financial Calendar).

- Share Buybacks: Following a $2 billion buyback program completed in early 2025, analysts expect further buyback announcements during the upcoming annual results to manage excess capital.

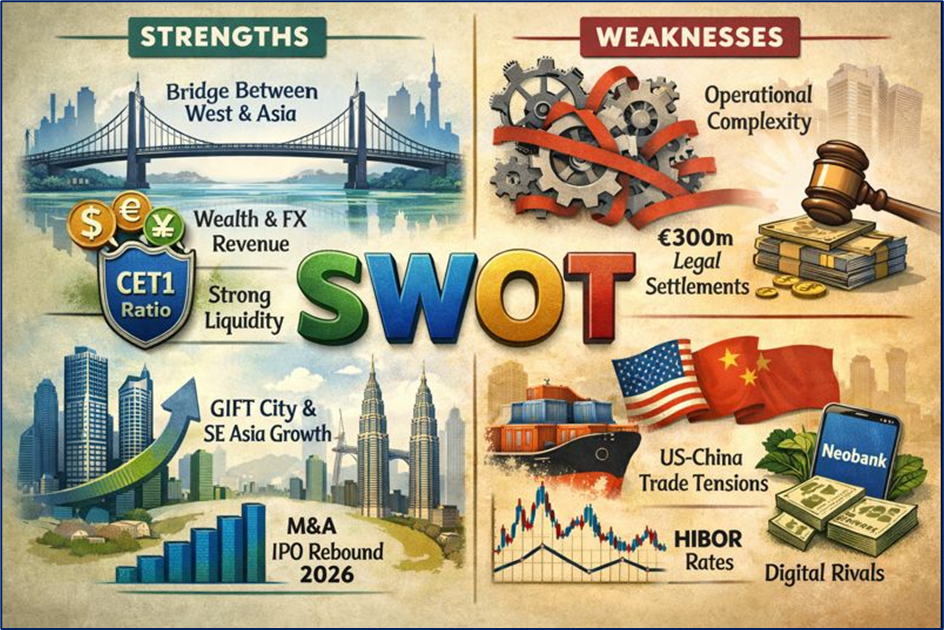

Latest SWOT Analysis

Source: Kalkine Group

Strengths

- Unrivaled "bridge" position between Western capital and Asian growth markets.

- Diverse revenue streams, with Wealth and Foreign Exchange activity offsetting declines in traditional lending margins.

- Strong liquidity position with a high-quality CET1 ratio.

Weaknesses

- High operational complexity despite recent simplification efforts.

- Exposure to legacy legal settlements, such as the €300m French dividend tax probe settled in early 2026.

Opportunities

- Growth in the "GIFT City" (India) and Southeast Asian wealth centers like Malaysia.

- Further consolidation of the Asian banking market following the Hang Seng delisting.

- Potential for higher-than-expected fees from a rebound in global M&A and IPO activity in 2026.

Threats

- Geopolitical tensions, particularly potential trade tariffs between the US and China.

- Macroeconomic sensitivity to the Hong Kong Interbank Offered Rate (HIBOR) fluctuations.

- Increasing competition from digital-native "neobanks" in the UK and Hong Kong retail sectors.

Outlook and Risks

The outlook for HSBC into the remainder of 2026 is defined by "Resilience in a Transforming World." The bank expects productivity gains from AI adoption to begin flowing through to the bottom line by Q3 2026. However, significant risks remain:

- Tariff Scenarios: The bank has modeled "disruptive tariff scenarios" involving a 25% tariff on certain Asian imports, which could dampen trade finance revenues.

- Rate Volatility: While the structural hedge provides a cushion, a faster-than-expected decline in global interest rates could pressure Net Interest Margins (NIM) in the medium term.

- Regulatory Scrutiny: As a Global Systemically Important Bank (G-SIB), HSBC remains subject to evolving capital requirement rules (Basel 3.1) which could impact future buyback capacity.

Conclusion

The 2.3% surge in HSBC’s stock on January 27, 2026, serves as a testament to the bank's successful pivot toward a more integrated and Asia-centric model. By taking Hang Seng Bank private and focusing on high-margin wealth services, HSBC has managed to maintain investor confidence despite a complex global backdrop. While geopolitical and interest rate risks persist, the bank’s disciplined capital allocation and robust dividend framework continue to make it a focal point of the FTSE 100’s financial sector.

Please wait processing your request...

Please wait processing your request...