The mining behemoth Rio Tinto (LSE: RIO) is ending 2025 with a bang. On December 22, the stock climbed ~1.6%, outperforming a cautious FTSE 100. This isn't just a daily fluctuation; it's the market's reaction to a strategic "sharpening" of the world’s second-largest miner.

Key Reasons & Market Drivers for the Dec 22 Surge

Source: Kalkine Group

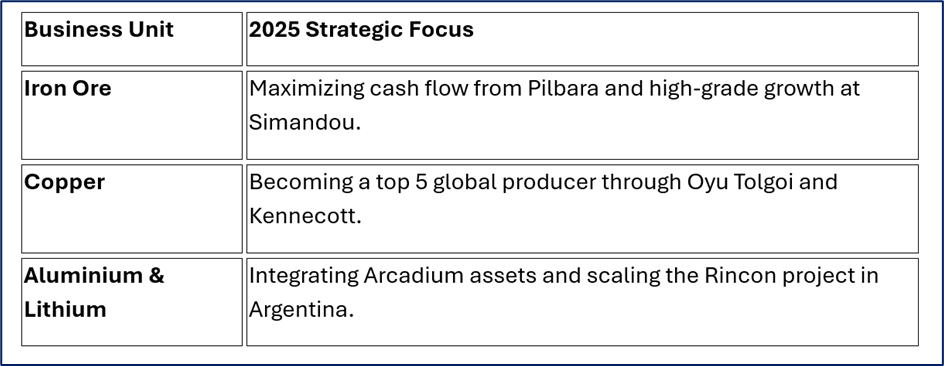

- "Stronger, Sharper, Simpler" Strategy: Investors are rallying behind new CEO Simon Trott’s restructuring plan, which streamlines the company into three core pillars: Iron Ore, Copper, and Aluminium & Lithium.

- Copper Guidance Upgrade: Rio recently bumped its 2025 copper production guidance to 860–875 kt (up from 780–850 kt), signaling that the Oyu Tolgoi underground ramp-up is ahead of schedule.

- Asset Sale Buzz: Reports of a $10 billion asset release program—targeting non-core titanium and borates units—have fueled expectations of a massive capital return or a war chest for further lithium acquisitions.

- The "Simandou" Milestone: With first ore already moving at the Simandou project in Guinea, Rio is proving it can execute high-stakes, high-grade projects in complex jurisdictions.

- Undervaluation Signal: Analysts (including Zacks) highlighted RIO as a "Value" powerhouse today, citing a forward P/E of ~9.9x and a remarkably low PEG ratio of 0.37.

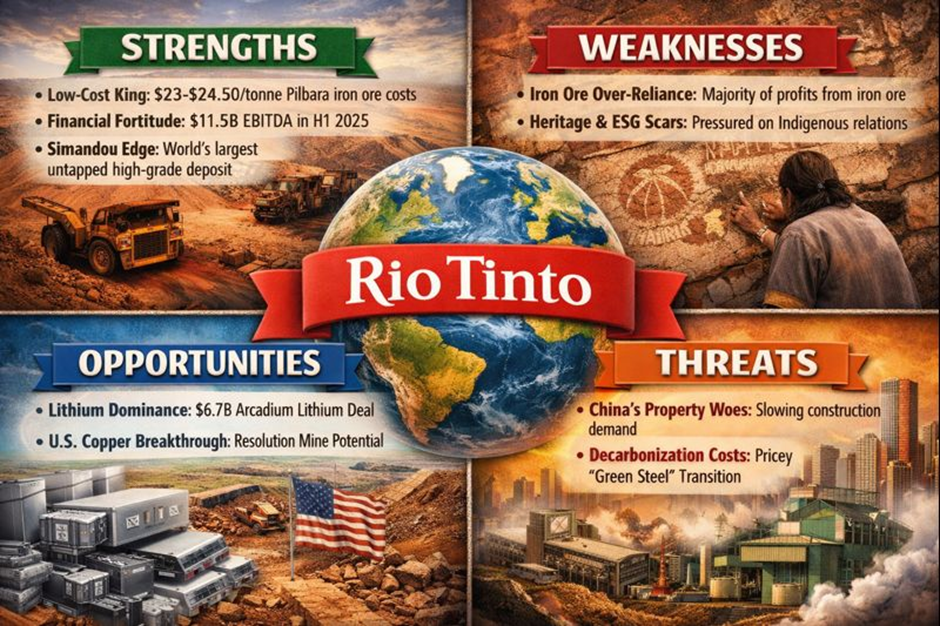

2025 SWOT Analysis

Source: Kalkine Group

Strengths

- Low-Cost King: Pilbara iron ore unit costs remain ultra-competitive at $23.00–$24.50/tonne.

- Financial Fortitude: Delivered a resilient $11.5 billion EBITDA in H1 2025 despite volatile iron ore pricing.

- Simandou Edge: Ownership of the world's largest untapped high-grade iron ore deposit.

Weaknesses

- Iron Ore Over-Reliance: Despite diversification, iron ore still dictates the majority of the bottom line.

- Heritage & ESG Scars: Ongoing pressure to repair relations with Indigenous groups following historic site damage.

Opportunities

- Lithium Dominance: The $6.7 billion Arcadium Lithium acquisition (closing March 2025) makes Rio a top-tier player in the EV battery supply chain.

- U.S. Copper Breakthrough: Potential fast-tracking of the Resolution Copper mine in Arizona under a more pro-mining U.S. administration.

Threats

- China’s Property Sector: Continued cooling in Chinese construction could dampen long-term steel demand.

- Decarbonization Costs: The "green steel" transition requires billions in CapEx for low-carbon smelting technology.

Latest Business Model: The "Three-Pillar" Pivot

Rio Tinto has officially moved away from being a "diversified conglomerate" to a Future-Facing Commodity Hub.

Source: Company Data

Financial & Operational Updates (Q4 2025)

- Production Momentum: Group-wide production is expected to rise 7% year-on-year in 2025.

- Cost Discipline: Management targets a 4% reduction in unit costs by 2030 through automation and AI-driven logistics.

- Dividend Yield: Currently sitting at a juicy 5.28%, supported by a consistent 40-60% payout policy.

- Net Debt: While debt rose to $14.6bn following the Arcadium deal, cash flow from operations remains robust at over $15bn annually.

Risks to Watch

- Geopolitical Friction: Trade barriers or tariffs on refined copper and aluminium could disrupt global supply chains.

- Operational Disruptions: As seen with Cyclone Sean earlier this year, extreme weather remains a persistent threat to Pilbara port operations.

- Commodity Volatility: A sharp drop in iron ore prices below $90/tonne would test the stock’s current support levels.

Conclusion

Rio Tinto is no longer just a "legacy" iron ore miner. By aggressively pivoting toward Copper and Lithium while maintaining its status as the world's most efficient iron ore producer, it has positioned itself as a primary beneficiary of the global energy transition. Today's 1.8% gain reflects a market finally pricing in the "sharper, simpler" Rio.

Source: Trading View, 22 December 2025

Please wait processing your request...

Please wait processing your request...