The most robust investment strategy for a retail client integrates their personal life stage and career earnings potential (Human Capital) with their accumulated savings (Financial Capital). This alignment dictates the appropriate risk level, transitioning from aggressive accumulation to conservative decumulation.

1. The Financial Human Life Cycle: Accumulation vs. Decumulation

An individual's financial journey is typically segmented into two macro phases, each requiring fundamentally different investment strategies and risk management approaches.

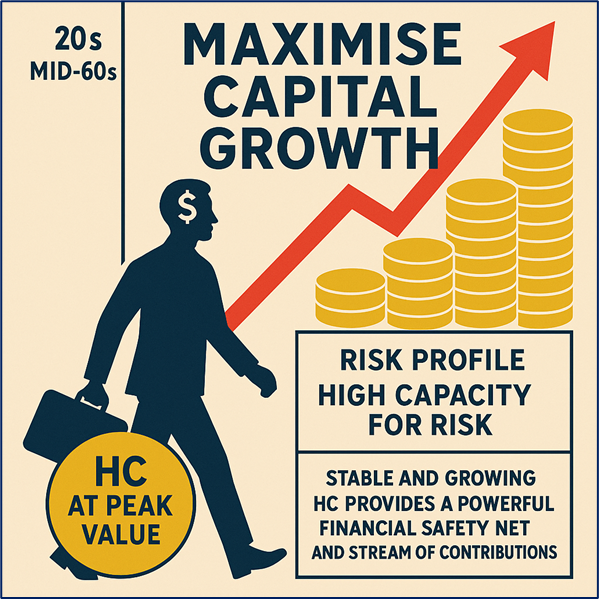

A. The Accumulation Phase (Early Career to Pre-Retirement)

- Timeline: Typically, ages 20s to mid-60s.

- Primary Objective: Maximise Capital Growth. The focus is on increasing the size of the Financial Capital base.

- Risk Profile: High Capacity for Risk. The long-time horizon allows the investor to withstand significant market downturns, as they have years to recover and can continue investing regularly at lower prices (Dollar-Cost Averaging).

- Human Capital (HC) Role: HC is at its peak value. Stable and growing HC provides a powerful financial safety net and stream of contributions. This high-value HC allows the Financial Capital portfolio to take a higher risk.

Source: Kalkine Group

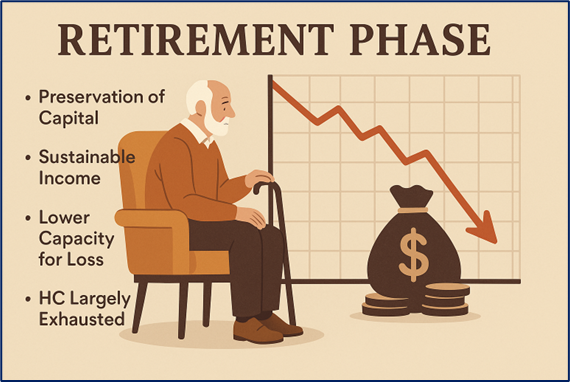

B. The Decumulation Phase (Retirement and Beyond)

- Timeline: Typically ages mid-60s onwards.

- Primary Objective: Preservation of Capital and Generation of Sustainable Income. The goal shifts from growth to funding withdrawals without prematurely depleting the pot.

- Risk Profile: Lower Capacity for Loss. Market downturns during this phase can severely reduce the portfolio's longevity due to the Sequence of Returns Risk (selling assets when markets are down to fund withdrawals).

- Human Capital (HC) Role: HC is largely exhausted (income is no longer derived from work). The Financial Capital must now bear the full burden of funding living expenses.

Source: Kalkine Group

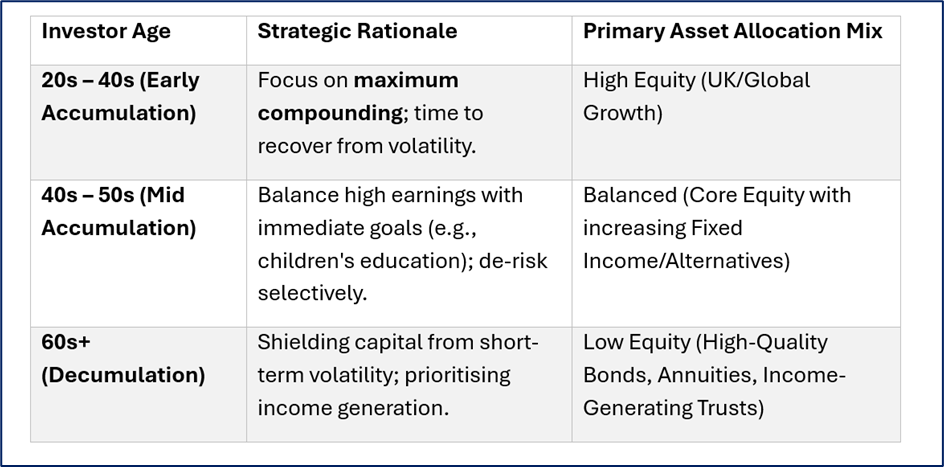

2. Age-Based Rules and Asset Allocation

The traditional guidance for retail investors links increasing age to decreasing risk. While simplified, this remains a powerful starting point for managing risk across the life cycle.

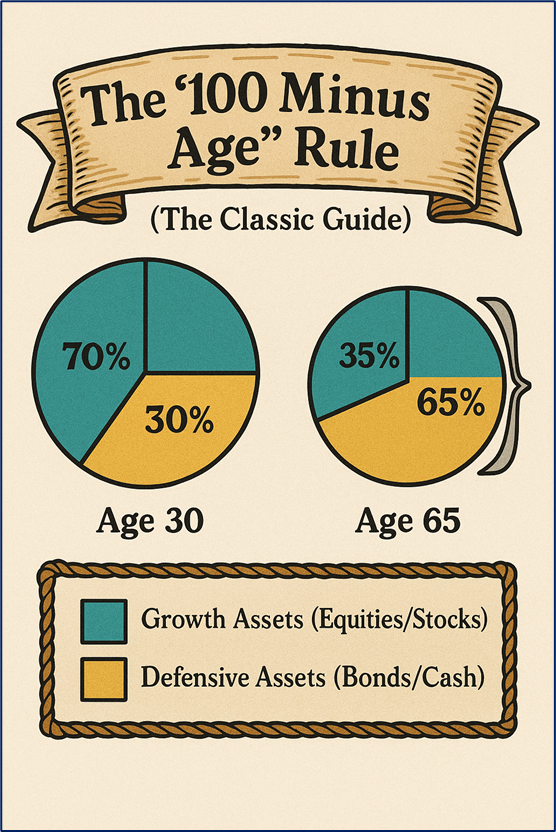

The "100 Minus Age" Rule (The Classic Guide)

This rule suggests that the percentage of your portfolio allocated to Growth Assets (Equities/Stocks) should equal 100 minus your current age, with the remainder allocated to Defensive Assets (Bonds/Cash).

- Example for a 30-year-old: 100 - 30 = 70% Equities / 30% Defensive Assets.

- Example for a 65-year-old: 100 - 65 = 35% Equities / 65% Defensive Assets.

Source: Kalkine Group

Asset Allocation Mix

Source: Kalkine Group

Note on Modern Adjustments: Given increased longevity, some practitioners suggest using "110 or 120 minus age" to maintain a higher equity allocation for longer, acknowledging that a 65-year-old may have a 25–30-year retirement horizon.

3. Risk-Taking and Asset Class Selection

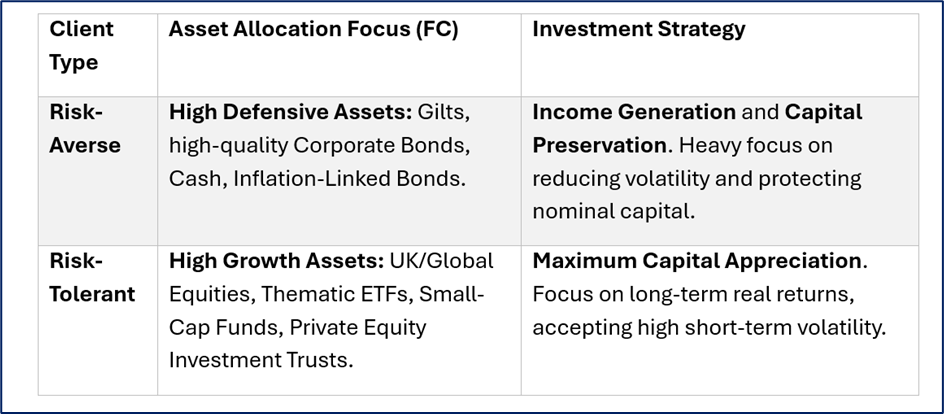

A. Risk-Averse vs. Risky Clients

Asset allocation strategies must reflect the client's risk tolerance (willingness to take risk) and capacity for loss (ability to withstand loss).

Source: Kalkine Group

B. Portfolio Optimisation for UK Retail Clients

- Diversification Among Geographies: Counteracting the UK Home Bias. Even a risk-averse client should hold exposure to globally diversified low-cost ETFs to access growth markets (US, Developed Europe) and reduce reliance on the domestically focused FTSE 250.

- Sectoral Diversification: Balancing Cyclicals (e.g., Financials, Industrials, dependent on economic cycle) with Defensives (e.g., Utilities, Healthcare, stable regardless of the economic cycle).

- Smart Money Strategy (Goal Buckets): Using Goal-Based Investing to partition the portfolio. Short-term goals (e.g., deposit in 3 years) are placed in Cash/Short-Term Bonds, while long-term goals (e.g., retirement in 25 years) are in high-growth equities, regardless of the client's overall current age.

Source: Kalkine Group

4. Outlook for UK Assets to 2026

The medium-term outlook for UK markets to 2026 suggests a continuation of the theme of corporate value and yield.

- UK Gilts: Potentially offer stability and moderate capital gains if inflation moderates and the BoE begins easing interest rates. Crucial for the Decumulation Phase.

- UK Equities (Global Earners): The large, internationally focused companies of the FTSE 100 are expected to remain resilient, providing consistent dividends. Ideal for the income component of Accumulation and a core holding in Decumulation.

- Thematic Sectors: Continued investment in Renewable Energy Infrastructure Trusts (UK focused) and Digital Healthcare/Life Sciences (global focus) will be important for the Growth component of a strategy.

Conclusion: The Evolving Risk Budget

The management of a retail client's wealth is a constant process of adjusting the risk budget. When Human Capital is high and future cash flow is secure (early Accumulation), the portfolio can be aggressive. As the investor moves into Decumulation, Financial Capital becomes the only asset, necessitating a sharp shift towards capital preservation and reliable income. All investment decisions should flow from the question: Which asset class best serves the specific goal at this unique point in the investor’s life cycle?

Please wait processing your request...

Please wait processing your request...