London’s Blue-Chip Index Shrugs Off Retail Blues as Rio Tinto-Glencore Mega-Merger Rumors Spark Commodity Firestorm

The FTSE 100 is defying the winter gloom today, trading up 0.42% as of midday. While the high street is grappling with a "post-Christmas hangover" following mixed updates from retail giants, the City of London is fixated on a potential seismic shift in the natural resources sector.

The headline driver? The return of the "mother of all mining deals." Rio Tinto and Glencore have confirmed preliminary discussions regarding a potential business combination—a move that could create a global titan in copper, iron ore, and energy transition metals.

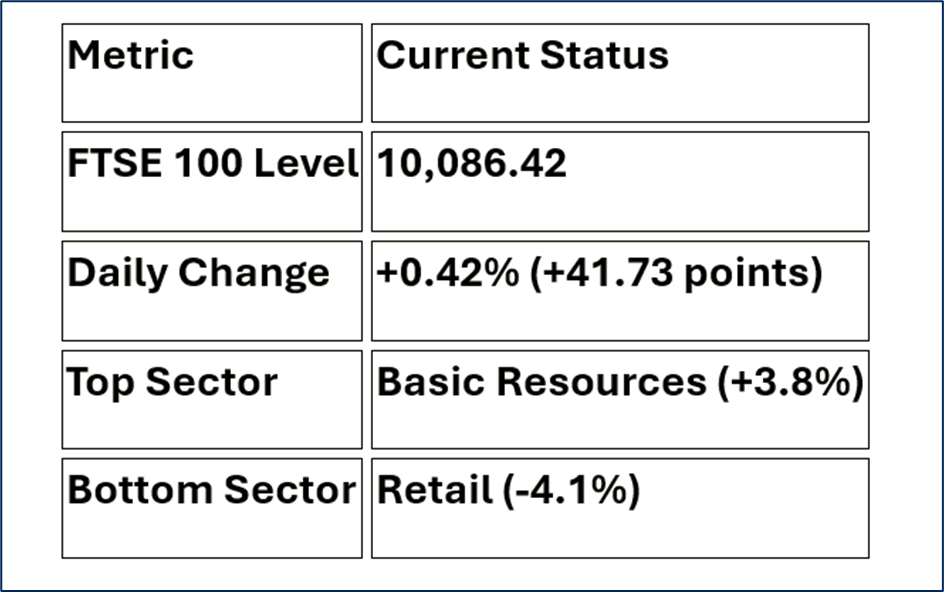

Market Snapshot: The 9 Jan Scorecard

Source: Market Data

The Key Drivers: Why the FTSE is Climbing

- The Mining Mega-Merger

The market was electrified by the news that Rio Tinto and Glencore are back at the negotiating table. Analysts suggest Rio Tinto is eyeing Glencore’s massive copper portfolio to fuel its green energy transition strategy. This has sparked a "follow-the-leader" rally across the entire mining sector.

- Sterling’s Strategic Slide

The British Pound fell 0.1% to $1.3417 today. While a weaker currency usually signals economic caution, it is a classic "tailwind" for the FTSE 100. Since roughly 75% of the index's revenue is earned in foreign currencies (mostly USD), a weaker pound inflates the value of those overseas earnings when brought back to London.

- Goldman Sachs’ Bullish Call

Sentiment was further bolstered by Goldman Sachs, which issued a major upgrade for Antofagasta, raising its price target from 2,480p to a staggering 4,000p. This move signaled to institutional investors that the "commodity supercycle" still has plenty of runway in 2026.

Source: Kalkine Group

Winners & Losers: Stocks in Focus

The Leaderboard (Gainers)

- Glencore (GLEN): +8.2% – The primary target of the merger talks; investors are betting on a significant premium if the deal proceeds.

- Antofagasta (ANTO): +4.8% – Riding the wave of the Goldman Sachs upgrade and surging copper prices.

- BAE Systems (BA.): +2.1% – Continued momentum following reports of increased UK and US defense spending for 2026.

- Anglo American (AAL): +1.5% – Benefiting from sector-wide consolidation fever.

The Laggards (Losers)

- J Sainsbury (SBRY): -5.4% – Despite reporting strong grocery sales, the market was spooked by a miss in "General Merchandise" and Argos performance.

- Rio Tinto (RIO): -2.6% – The "acquirer’s curse." Investors often sell the buyer in a potential merger due to the massive capital requirements of a deal this size.

- Tesco (TSCO): -1.8% – Still feeling the drag from yesterday’s disappointing Christmas trading update.

Technical Analysis: The Road to 10,100

The FTSE 100 is currently testing a crucial resistance zone. After breaching the psychological 10,000 mark earlier this week, the index is showing a "bullish consolidation" pattern.

- Support: Immediate support lies at 9,928 (the November peak).

- Resistance: The all-time high of 10,160 is the next target. If the index closes above 10,100 today, technical analysts expect a "breakout" toward 10,400 by the end of Q1.

- RSI (Relative Strength Index): Currently at 68, suggesting the market is "warm" but not yet "overbought," leaving room for more upside.

Source: Trading View

Analyst Upgrades & Downgrades

- UPGRADE: Antofagasta – Goldman Sachs (Neutral to BUY); PT raised to 4,000p.

- DOWNGRADE: J Sainsbury – Jefferies (Buy to HOLD); citing margin pressure in non-food categories.

- REITERATED: Barclays – Morgan Stanley maintains OVERWEIGHT; citing the bank's benefit from a "higher-for-longer" interest rate environment in the UK.

Conclusion: A Tale of Two Markets

The FTSE 100 is currently a tale of two markets: the old-world cyclicals (miners and banks) are carrying the index to record heights, while the consumer-facing retailers are struggling under the weight of a cautious UK consumer. For global investors, the London market remains a premier "value play" and a hedge against global inflation, especially with the prospect of the largest mining merger in a decade on the horizon.

The big question for this afternoon: Will the US Non-Farm Payrolls (due at 1:30 PM GMT) support the rally or trigger a weekend sell-off?

Please wait processing your request...

Please wait processing your request...