Key Takeaways

- AI Inflection Point: 2025 marks the shift from generative AI hype to autonomous, ROI-driven agentic AI.

- Capital vs. Workforce: Massive Capex drives concentrated productivity gains, while 141,000+ tech jobs cut globally, highlighting the labor-capital shift.

- UK Strategic Advantage: Flexible AI regulations, £250M government compute support, AI Growth Zones, and hyperscaler investments position the UK as a global AI hub.

- Compute & Energy Challenges: GW-scale data centers strain the National Grid; solutions include Green Computing, SMRs, and renewable integration.

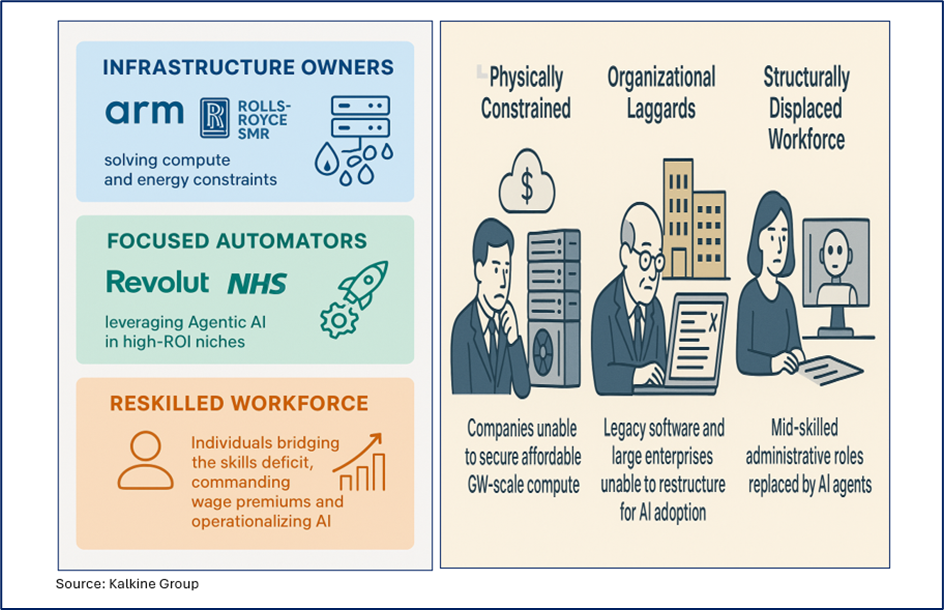

- Smart Money Winners: Key beneficiaries include ARM (chips), Rolls-Royce SMR (energy), Oxford Nanopore (deep science), and AI startups like incident.io and PhysicsX.

- ROI-Driven Enterprise Adoption: AI delivers tangible results in healthcare (NHS efficiency gains), cybersecurity (97% UK firms), and fintech (Revolut fraud reduction 50%).

- Disruption & Risks: Firms failing to secure compute, restructure operations, or reskill staff face marginalization, while mid-skilled roles are displaced by automation.

- Outlook (2025–2030): Success depends on scaling infrastructure, deploying agentic AI, reskilling workforce, and leveraging sustainable energy solutions to fully capture the AI Supercycle.

AI is no longer hype—it’s a capital-intensive force reshaping the UK economy. The year 2025 marks a critical inflection point: generative AI moves from novelty to autonomous, agent-driven enterprise utility, forcing major global capital deployment decisions. Britain, with its flexible regulatory framework and talent-rich ecosystem, is perfectly positioned to capture outsized value in this AI supercycle.

- The AI Inflection Point – From Hype to ROI

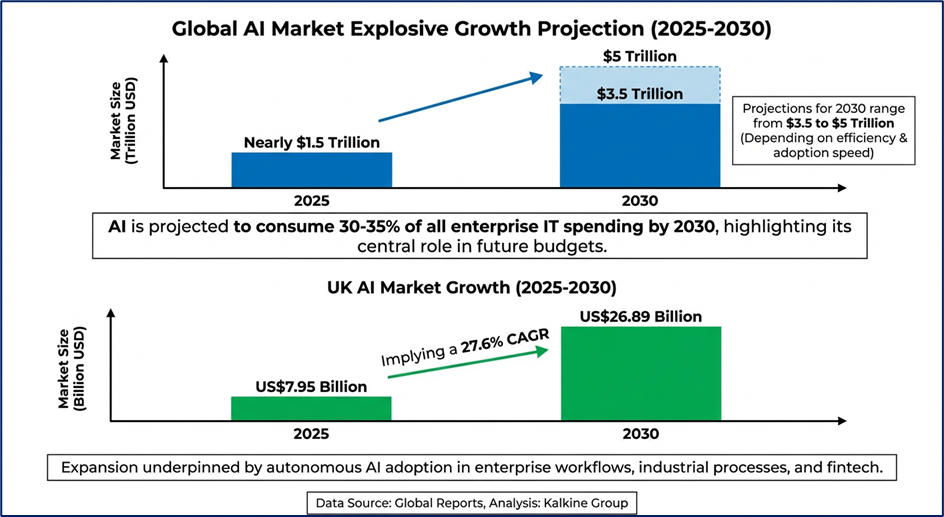

Explosive Market Growth

The UK AI market is poised to grow from US$7.95 billion in 2025 to US$26.89 billion by 2030, implying a 27.6% CAGR (global market reports). This expansion is underpinned by autonomous AI adoption in enterprise workflows, industrial processes, and fintech.

Yet, this boom contrasts sharply with the global labor market: tech giants have announced over 141,000 job cuts in 2025 even as they invest $375 billion in AI infrastructure. Capital is replacing labor. The resulting productivity gains are highly concentrated, benefiting shareholders while reshaping employment structures.

Why the UK Matters

Britain is pursuing a flexible, principles-based regulatory approach, encouraging innovation and foreign direct investment. In contrast, the EU’s prescriptive AI Act imposes strict rules from August 2025.

- Microsoft: US$30 billion investment in UK AI infrastructure (2025–2028)

- UK Government (DSIT): Up to £250 million in compute resources for research and startups

- Zoom & Equinix: £28 million+ investments in UK data centers

This policy mix positions the UK as a global hub for AI safety, fintech, and scientific innovation, attracting both capital and talent.

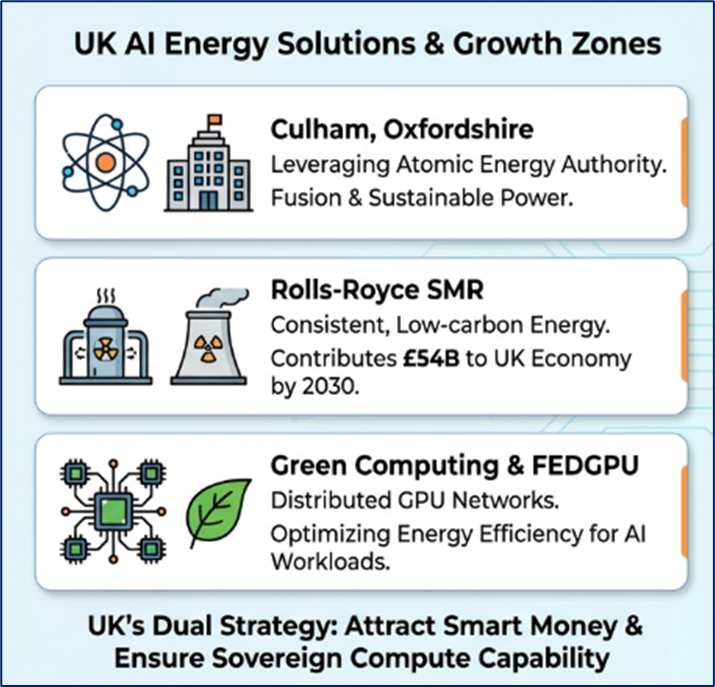

II. The Compute Battleground

AI adoption depends on compute capacity. Large-scale AI models require high-density data centers and massive power. The global AI market demands $5.2 trillion in data center investment by 2030, adding 125 GW of new capacity.

UK Infrastructure Bottlenecks

- Existing UK grid capacity is constrained; future AI data centers may require 500 MW+, equivalent to several small towns.

- Electricity costs are among the highest in Western Europe, with OpEx pressure for running large-scale AI operations.

- Microsoft shifted to leasing ready-to-use data centers at US$11.1 billion in 2026 to bypass grid delays.

Strategic Response

The UK has introduced AI Growth Zones, fast-tracking data center approvals and securing priority energy access.

Analysis: Kalkine Group

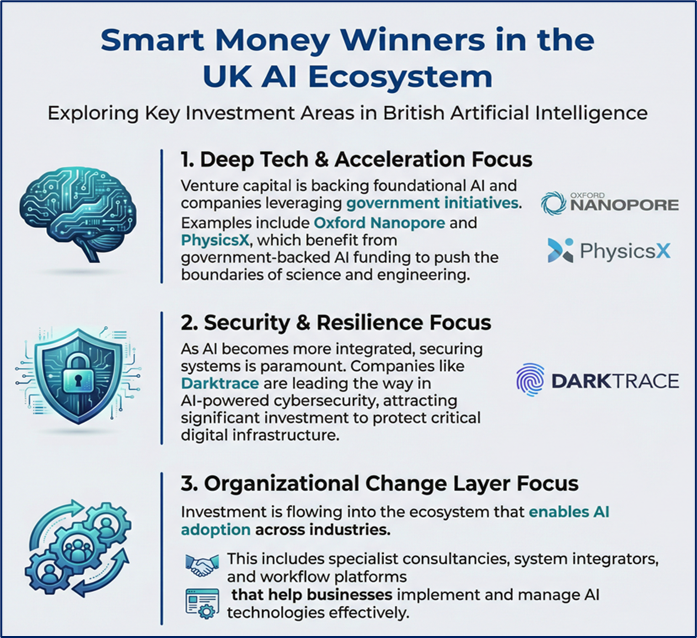

III. Who Wins – The Smart Money Thesis

Investment in the AI supercycle flows into two primary areas: infrastructure enablers and enterprise automation platforms (Agentic AI).

- Infrastructure & Core Compute

- ARM Holdings (ARM, Nasdaq): Dominates chip architecture for edge devices and AI infrastructure. YTD stock growth: +90.48% (April 2025).

- Oxford Nanopore Technologies (ONT, LSE): AI-driven genomics accelerates drug discovery, backed by £137 million government funding for scientific research.

- Agentic Enterprise & High ROI

AI adoption now hinges on measurable outcomes rather than tech novelty.

Healthcare:

- Microsoft 365 Copilot pilots in 90 NHS organizations save 43 minutes per staff member per day, equating to millions of hours annually.

Cybersecurity:

- 97% of UK cyber orgs now consider AI essential for threat detection and predictive analytics.

Fintech:

- Revolut launched AI-powered financial assistants to guide customers and reduce fraud losses by up to 50%.

- AI triage cuts manual review time by 50%, transforming cost centers into competitive strengths.

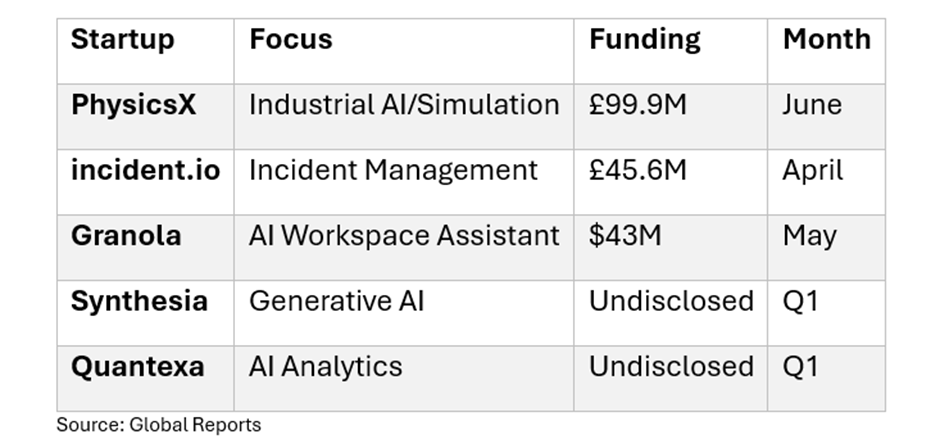

- Venture Capital Hotspots

2025 saw record VC funding for UK AI startups:

Smart money favors foundational IP and high-ROI agentic automation over organizational-wide, capital-intensive transformations.

IV. Who Loses – Disruption Zones

- Workforce Displacement

- Automation is hollowing out mid-skilled roles.

- AI-driven CapEx replaces labor, contributing to economic decoupling from employment.

- Talent Scarcity

- Specialized AI skills now command a 56% wage premium.

- Companies failing to retrain staff risk losing operational advantage.

- Legacy Software

- ERP and accounting providers like Sage face competition from cloud-native AI-first platforms (Xero, QuickBooks, NetSuite).

- Slow adaptation threatens market share and long-term profitability.

- Execution Failures

- Ocado Group demonstrates that technological leadership doesn’t guarantee commercial success.

- Robotics and reinforcement learning cut costs but scaling internationally proved challenging, eroding shareholder value.

V. Governance, Regulation, and Geopolitical Risk

- Flexible UK Regulation

- Principles-based approach encourages investment while minimizing deployment friction.

- Contrasts with EU’s prescriptive AI Act (active August 2025).

- AI Safety & International Coordination

- UK leads on global AI safety, including the Paris AI Action Summit 2025.

- AI Safety Institute operationalizes international agreements, focusing on catastrophic risk mitigation.

- Liability Risks

- Rapid adoption in healthcare introduces legal uncertainty.

- Survey: 20% of therapists report AI-generated guidance that could harm mental health patients.

- Creates a growing market for AI liability insurance and legal services.

- Financial Systemic Risk

- Concentrated Capex among hyperscalers risks market volatility if ROI targets fail.

- Bank of England warns of potential correction amid record AI valuations.

VI. Smart Money Flow Map (2025–2030)

1. Infrastructure vs. Software

Analysis: Kalkine Group

Analysis: Kalkine Group

2. Key Investment Themes

Analysis: Kalkine Group

VII. Winners and Losers – UK AI Supercycle 2025–2030

Conclusion

The UK AI Supercycle is a high-stakes convergence of capital, technology, regulation, and infrastructure. The next five years will determine who captures the £100 billion smart money flowing into Britain’s $27 billion AI economy.

- Success favors those who own the compute backbone, execute targeted high-ROI AI deployments, and reskill their workforce.

- Failure awaits those constrained by energy bottlenecks, legacy systems, or poor execution.

Britain’s flexible regulatory framework, combined with strategic infrastructure investments, positions the UK as a prime destination for global AI capital—provided it resolves the grid and energy constraints threatening its supercycle ambitions. The AI Supercycle is no longer optional; it’s the 21st-century industrial transformation defining who will lead in technology, capital, and global competitiveness.

Please wait processing your request...

Please wait processing your request...