The final trading sessions of 2025 are delivering fireworks for small-cap investors. TomCo Energy (LSE: TOM), the Utah-focused oil development group, has ignited a massive 25% rally today, December 30. For a stock that has spent much of the year navigating the choppy waters of "pre-revenue" uncertainty, this double-digit breakout is catching the eyes of retail traders and institutional vultures alike.

Is this a seasonal "Santa Rally," or is there a fundamental shift in the TomCo story? Let’s dive into the analytical breakdown of why TOM is the talk of the AIM market today.

The Catalyst: What’s Driving the Dec 30 Surge?

While penny stocks are prone to volatility, today’s move appears rooted in a "perfect storm" of year-end positioning and long-awaited operational clarity.

Source: Kalkine Group

- Valkor Partnership Milestones: Investors are reacting to the culmination of the company's objective to commence drilling in Utah. Throughout 2025, TomCo has been in deep negotiations with its technical partner, Valkor LLC, to finalize a partnership for four wells. Speculation is rife that the definitive agreement—and the funding consortium to back it—is finally crossing the finish line.

- Revenue Proximity: For the first time in years, "meaningful revenue" is no longer a distant dream. Each well in the Utah Lease Area is estimated to cost between $0.8M and $1.0M. The market is betting that the transition from a "land-holding" company to a "production" company is imminent.

- Low Liquidity Momentum: With a market cap hovering around £2.3M - £3M, it doesn't take much buy-side volume to move the needle. A few "Buy" orders in a thin holiday market can trigger a 25% vertical move as shorts cover and momentum traders pile in.

Latest Business Model: The "Utah Oil Sands" Pivot

TomCo’s business model has matured significantly in 2025. Moving away from purely experimental technology, the company now operates a dual-track strategy through its subsidiary, Greenfield Energy LLC:

- Near-Term Cash Flow: Drilling conventional wells on the AC Oil Lease in partnership with Valkor. This aims to generate immediate revenue to sustain the company without constant equity dilution.

- Long-Term Upside: The Oil Sands Separation project. TomCo is positioning itself to use innovative technology to unlock the massive hydrocarbon resources in the Green River Formation, Utah.

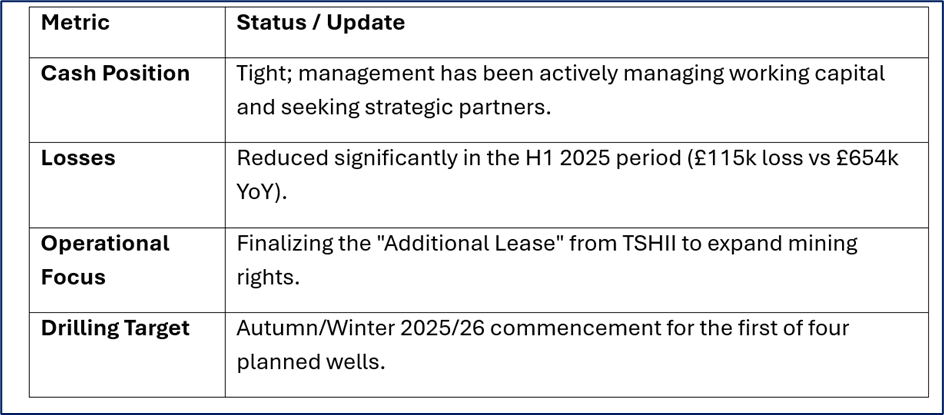

Financial & Operational Snapshot (Q4 2025)

Source: Company Data

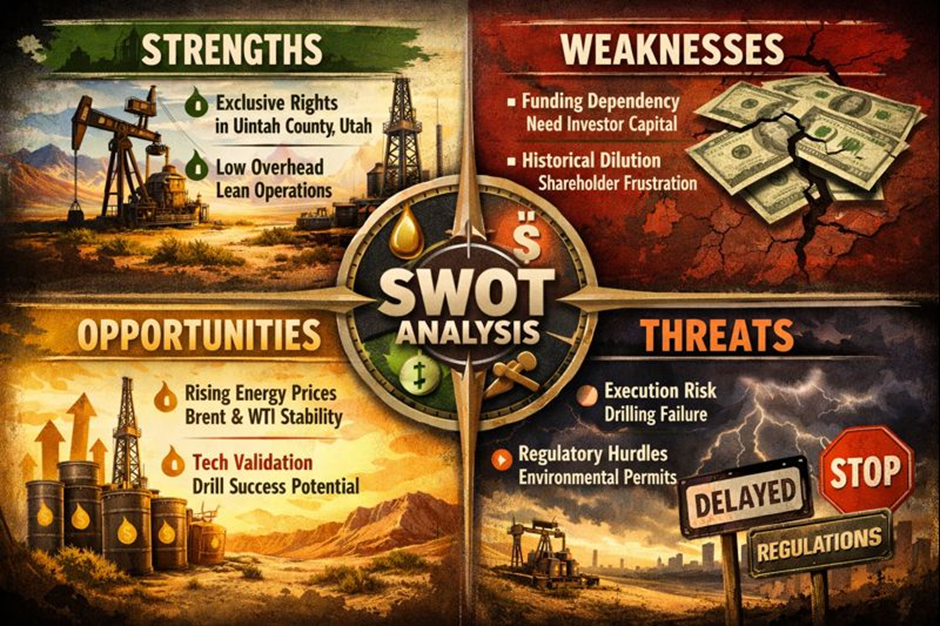

SWOT Analysis: The Cold, Hard Truth

Source: Kalkine Group

Strengths

- Prime Assets: Exclusive rights to explore and mine in the oil-rich Uintah County, Utah.

- Low Overhead: Operating as a lean entity with minimal permanent staff, focused on partner-led development.

- Strategic Partners: Alignment with Valkor provides technical expertise that TomCo couldn't afford solo.

Weaknesses

- Funding Dependency: The company remains dependent on raising capital or securing a "consortium of investors" to fund drilling.

- Historical Dilution: Frequent share issuances have frustrated long-term holders.

Opportunities

- Energy Prices: With Brent Crude and WTI stabilizing, the economics of Utah's unconventional oil become more attractive.

- Technology Validation: A successful drilling campaign could re-rate the stock from a "speculative penny" to a "junior producer."

Threats

- Execution Risk: Any delay in the Valkor partnership or technical failure in the initial wells could crater the price.

- Regulatory Hurdles: Utah environmental permits are always a moving target.

The Risks: Investor Beware

Despite the 25% gain, TomCo is not for the faint of heart. The stock is currently trading at a high Price-to-Book (P/B) ratio compared to its peers, and it remains pre-revenue. The "Going Concern" note is a staple of junior miners, and TomCo is no exception. If the projected funding for the four-well program fails to materialize, the current rally could evaporate as quickly as it appeared.

Conclusion: A New Chapter or a Dead Cat Bounce?

Today’s 25% jump marks a pivot point for TomCo Energy. The market is clearly pricing in a successful transition to drilling operations. If the company confirms the finalization of the Valkor agreement in early January, this could be the start of a sustained recovery. However, until the first barrel of oil is sold, TOM remains a high-stakes play on the future of Utah's oil sands.

Please wait processing your request...

Please wait processing your request...