As we navigate the opening weeks of 2026, the FTSE AIM market is witnessing a renaissance. After years of being overshadowed by US Tech, "Smart Money"—institutional fund managers and private equity—is rotating back into UK small-caps.

The primary catalyst is a "valuation spring-back." With the Bank of England continuing its rate-cutting cycle (benchmarks now hovering near 3.0%), the cost of capital for growth-hungry firms has plummeted. Analysts at Peel Hunt and Panmure Liberum are increasingly vocal that the AIM 100 is currently "priced for a recession that never arrived," creating a significant arbitrage opportunity for 2026.

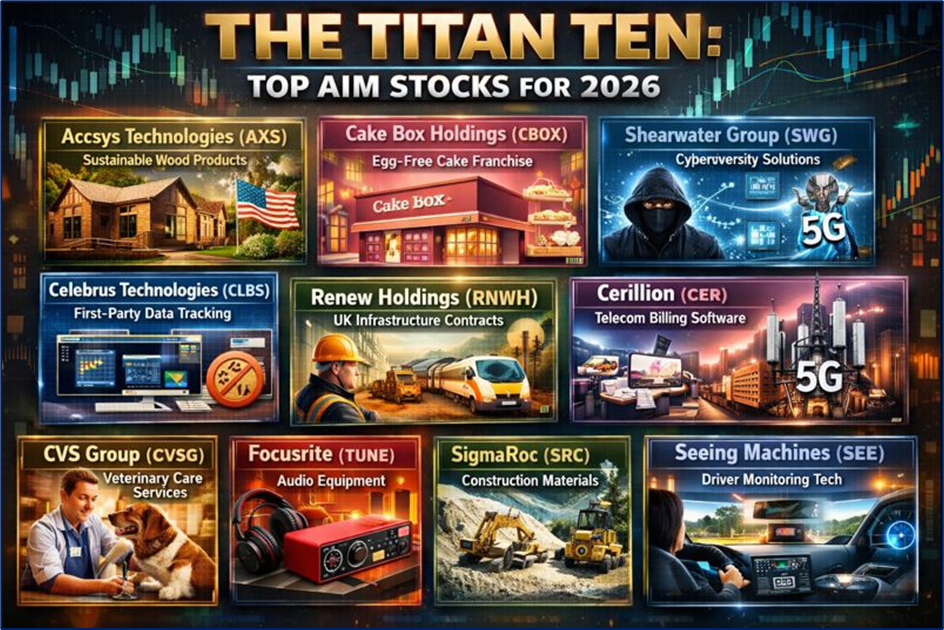

THE TITAN TEN: TOP AIM STOCKS FOR 2026

Source: Kalkine Group

- The Drivers: Decarbonizing the construction sector. Accsys creates high-performance, sustainable wood (Accoya) that outlasts tropical hardwoods.

- Latest Update: The 2026 outlook is anchored by the ramp-up of the Kingswinford facility and the US joint venture with Eastman, which is finally nearing peak capacity.

- Technical Analysis: The stock has formed a "cup and handle" pattern on the weekly chart, suggesting a breakout above the 80p resistance level.

- Risk: Commodity price volatility in raw timber supplies.

- The Drivers: First-party data capture. As third-party cookies vanish, Celebrus’s ability to help banks and retailers track user behavior ethically is a goldmine.

- Latest Update: Panmure Liberum recently highlighted a swing back to profitability, forecasting a significant jump in Annual Recurring Revenue (ARR) to £18m by mid-2026.

- Technical Analysis: Consolidation at the 200-day Moving Average (MA) suggests the "weak hands" have exited, leaving a base for an upward move.

- Risk: High competition from US-based SaaS giants.

- The Drivers: A recession-proof franchise model. Their egg-free cakes appeal to a massive, underserved demographic with high brand loyalty.

- Latest Update: The acquisition of Indian sweets specialist Ambala is being integrated, with 13 new stores opened in the last cycle, bringing the total to over 270.

- Technical Analysis: Consistent higher-lows on the daily chart indicate strong retail accumulation.

- Risk: Rising dairy and sugar input costs.

- The Drivers: Critical UK infrastructure. They maintain the railways, nuclear sites, and water networks—spending that the UK government cannot cut.

- Latest Update: Peel Hunt recently reiterated a Buy rating with a target of 1,300p, citing a record order book exceeding £800m.

- Technical Analysis: The stock is trading in a tight bullish flag; a move above 1,150p could trigger a technical squeeze to new highs.

- Risk: Labour shortages in specialized engineering.

- The Drivers: Cybersecurity tailwinds. As AI-driven cyber threats escalate, Shearwater’s advisory and software services are seeing 2026 as a "contract super-cycle."

- Latest Update: A newly won £7.3m telecoms contract expansion has de-risked the 2026 revenue forecast.

- Technical Analysis: Deeply oversold on the RSI (Relative Strength Index), making it a classic "value-growth" play at current levels.

- Risk: Project-based revenue can be "lumpy" and unpredictable.

- The Drivers: 5G rollout and billing software. Telecoms globally are upgrading legacy systems to handle 2026 data loads.

- Latest Update: Reported a 20% jump in pre-tax profits with a "record-high" pipeline of new business opportunities in the Americas.

- Technical Analysis: Trading near all-time highs; technicals suggest a "trend-following" strategy is best here.

- Risk: High valuation multiples compared to AIM peers.

- The Drivers: The "Humanization of Pets." Pet owners are spending more on complex veterinary care than ever before.

- Latest Update: Recovering from regulatory scrutiny in 2025, the business model has pivoted toward higher-margin specialized surgeries.

- Technical Analysis: Moving average convergence (MACD) has turned positive for the first time in six months.

- Risk: Continued Competition and Markets Authority (CMA) oversight.

- The Drivers: The creator economy. Their interfaces are the industry standard for podcasters and home musicians.

- Latest Update: Management has successfully diversified production away from high-tariff regions, protecting margins for the 2026 fiscal year.

- Technical Analysis: A "double bottom" at 180p suggests a strong floor is in place.

- Risk: Sensitivity to global consumer discretionary spending.

- The Drivers: Lime and heavy construction materials. They are essential for the "Green Steel" transition in Europe.

- Latest Update: Operational efficiencies from the CRH lime asset acquisition are expected to flow through to the bottom line by Q3 2026.

- Technical Analysis: Showing strong "relative strength" against the broader FTSE 250 index.

- Risk: High energy intensity in production processes.

- The Drivers: Mandatory safety tech. EU and US regulations for driver monitoring systems (DMS) are now entering a peak enforcement phase.

- Latest Update: Secured a $14m cash flow boost from a major OEM, moving the company closer to self-funded growth.

- Technical Analysis: Volatile price action; currently testing major support at the 5p level.

- Risk: Long lead times in automotive contracts.

Risks & Market Volatility

Investing in the AIM market involves a higher degree of risk than the Main Market.

- Liquidity: Many stocks have wide bid-ask spreads, making it difficult to exit large positions quickly.

- Regulatory: Lighter disclosure requirements mean investors must perform deeper due diligence.

- Macro: While the 2026 outlook is positive, any reversal in the Bank of England’s rate path could hit growth valuations hard.

Conclusion: The 2026 Opportunity

The FTSE AIM market in 2026 is no longer a "wild west" of speculative mining plays; it has matured into a hub for specialized engineering, sustainable tech, and high-margin SaaS. For the analytical investor, the combination of historically low valuations and a recovering UK macro environment makes this an era-defining entry point.

Please wait processing your request...

Please wait processing your request...