With the FTSE 100 shattering records and crossing the historic 10,000-point threshold, the spotlight has shifted to a select group of "rising stars" that are outperforming the broader market.

Today’s momentum is driven by a unique confluence of safe-haven gold demand, high-stakes merger speculation, and resilient consumer spending. Institutional fund managers and elite brokers are increasingly moving away from speculative tech and back into the UK's "Value Titans."

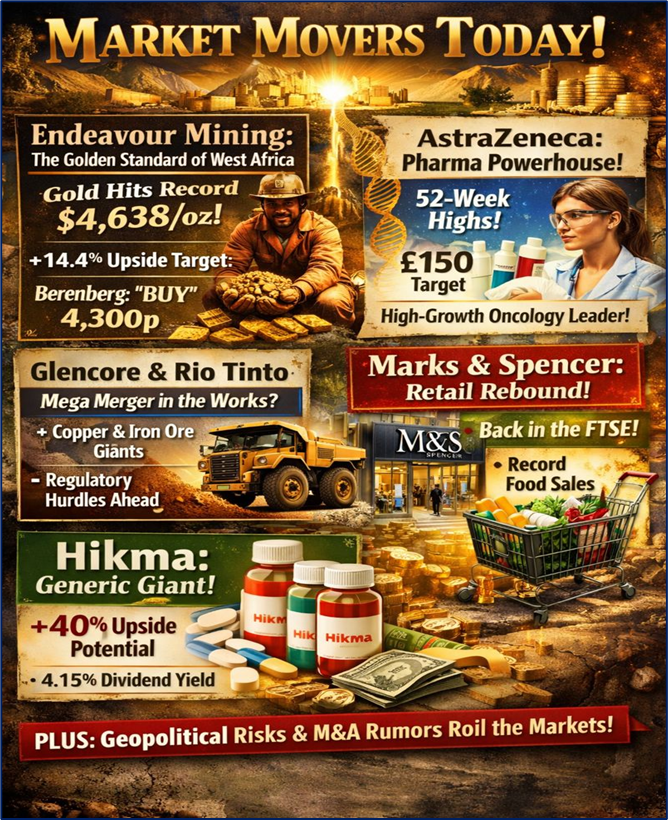

Source: Kalkine Group

Endeavour Mining (EDV): The Golden Standard of West Africa

Endeavour Mining has emerged as the clear leader in today’s rally, fueled by gold prices reaching a record $4,638 per ounce. Smart money is flowing into EDV as the company leverages its position as West Africa’s largest gold producer.

- Key Drivers: Record-breaking gold prices and the successful ramp-up of low-cost production assets in Senegal and Côte d’Ivoire.

- Technical Analysis: The stock is in a confirmed bullish breakout, trading well above its 50-day and 200-day moving averages ($3,576 and $3,014 respectively). The RSI sits at 72, indicating strong momentum but hinting at a potential short-term cooling period.

- Analyst Outlook: Berenberg Bank recently restated a "Buy" with a price target of 4,300p. Consensus remains a "Strong Buy" with a projected 14.4% upside.

- Dividend & Valuation: Yielding approximately 2.3% with a payout ratio of 60%. The forward P/E is elevated, reflecting market expectations of aggressive earnings growth in 2026.

- Risks: Geopolitical instability in West Africa and volatility in bullion prices.

AstraZeneca (AZN): The Pharmaceutical Powerhouse Defying Gravity

AstraZeneca continues to hit new 52-week highs, proving that its $80 billion 2030 revenue ambition is more than just talk. Investment banks are praising its "all-weather" business model.

- Business Model: Transitioning from a general pharma giant to a leader in high-margin oncology, rare diseases, and weight management therapies.

- Latest Financials: Reaffirmed guidance for 2025 with low double-digit EPS growth. The company is on track for a core operating margin in the mid-30% range by 2026.

- Analyst Upgrades: JPMorgan recently restated an "Overweight" rating, while Jefferies lifted its price target to £150.

- Valuation: Currently trading at a P/E of 23.8x. While not "cheap," a PEG ratio of 0.86 suggests it is undervalued relative to its growth trajectory.

- Risks: Pricing pressures in China (VBP procurement) and high R&D expenditure at the upper end of 20% of revenue.

Glencore (GLEN) & Rio Tinto (RIO): The M&A Mega-Deal Rumor Mill

The mining sector is buzzing following the bombshell announcement of preliminary merger discussions between Glencore and Rio Tinto. This "Combination of Giants" could create a global natural resources hegemon.

- The Driver: Glencore’s transition metals portfolio (Copper, Cobalt) is a perfect match for Rio Tinto’s iron ore dominance. Any potential all-share merger would be the largest in mining history.

- Technical Analysis (RIO): Support is holding at 6,100p. The stock is benefiting from a "rotation to value" as investors seek protection against inflation.

- Dividend Yields: Rio Tinto remains a dividend king with a yield of 3.64%, while Glencore’s focus on de-risking copper projects is attracting long-term institutional buyers.

- Operational Update: Glencore is strengthening its presence in Peru (Quechua Project), while Rio Tinto eyes the 5 February 2026 deadline to formalize its intentions.

- Risks: Regulatory hurdles for a merger of this scale are massive; failure to reach a deal could lead to a short-term sell-off.

Marks & Spencer (MKS): The Retail Phoenix Rising

MKS is the surprise comeback story of the FTSE. Despite a severe cyber-attack in early 2025, the company has regained its footing with record food market shares.

- Key Drivers: Food sales grew 5.6% in the latest quarter. The "Remarksable Value" range is successfully capturing families struggling with the cost of living.

- Technical Analysis: Analysts at Hargreaves Lansdown note that MKS is trading at a discount to peers, with a forward P/E of 10.5x compared to its 10-year average of 11.0x.

- Dividend: A prospective yield of 2.0% offers a modest but growing income stream.

- Financial Health: The balance sheet is robust, with a £100 million insurance payout mitigating the costs of the 2025 data breach.

- Risks: Fashion and Home recovery is slower than Food; ongoing friction with partner Ocado Retail over performance targets.

Hikma Pharmaceuticals (HIK): The Generic Giant with 40% Upside

Hikma is trending as a top defensive pick for 2026, offering exposure to the specialty and generic drug markets with a highly attractive valuation.

- Latest Update: Revenue growth of 5.7% and a commendable Return on Equity of 15.4%. The company has a robust free cash flow of over $128 million.

- Analyst Sentiment: Overwhelmingly bullish; 10 out of 11 analysts rate it a "Buy," with price targets suggesting a potential 40.5% upside.

- Dividend: Boasts a strong 4.15% yield, one of the highest in the healthcare sector, making it a favorite for income-focused "smart money."

- Technical Analysis: Currently trading near 1,565p. While the RSI suggests an overbought state, long-term moving averages remain in a "Golden Cross" formation.

- Risks: High valuation metrics (forward P/E) and potential bearish momentum if it breaks below the 1,550p support level.

Conclusion: Is Now the Time to Buy?

The data suggests a bifurcated market. For those seeking growth and stability, AstraZeneca and Hikma offer strong defensive moats. For speculative upside, the potential Rio Tinto-Glencore merger and the gold-backed rally of Endeavour Mining provide high-octane opportunities. Marks & Spencer remains the "value play" for those betting on a UK retail recovery.

Please wait processing your request...

Please wait processing your request...