The 2026 Metals Supercycle: A Strategic Overview of 3 FTSE-100 Mining Giants

The global mining sector has entered a "Value Pivot" as we start 2026. While the previous decade was defined by cost-cutting, the current era is characterized by the race for "Critical Minerals" and the decarbonization of heavy industry.

Smart money—led by the likes of BlackRock, Vanguard, and specialized hedge funds—has shifted focus toward companies with high operational leverage and aggressive growth in copper, lithium, and high-grade iron ore.

Source: Kalkine Group

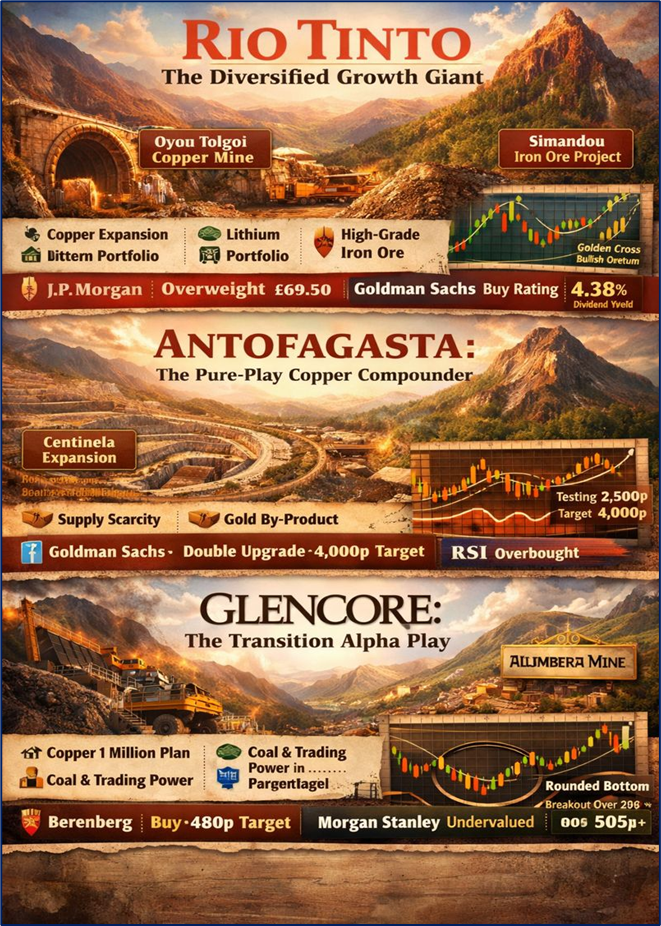

- Rio Tinto (RIO) - The Diversified Growth Giant

Latest Business Model and Operational Update Rio Tinto has pivoted from a traditional iron ore behemoth to a "Materials for the Future" powerhouse. The 2026 strategy focuses on the "Simandou" project in Guinea, the world’s largest untapped high-grade iron ore deposit, and the massive scale-up of the Oyu Tolgoi underground copper mine in Mongolia. Operationally, Rio is targeting a 40%–50% increase in EBITDA by 2030 through its "Stronger, Sharper, Simpler" initiative.

Key Drivers and Outlook

- Copper Expansion: Oyu Tolgoi is hitting its peak production ramp-up in 2026, making Rio a top-tier global copper producer.

- Lithium Portfolio: The Rincon project and potential M&A activity (including the Arcadium Lithium acquisition) position Rio as a western alternative to Chinese lithium dominance.

- High-Grade Iron Ore: Simandou provides the high-grade "green steel" inputs that the European and Asian markets are demanding for carbon-neutral manufacturing.

Current Technical Analysis As of January 2026, RIO has recently hit a 52-week high, breaking through the £62.00 resistance level. Technical indicators show a bullish "Golden Cross" on the weekly chart, with the 50-day moving average trending strongly above the 200-day average. Consolidation at these levels suggests a new floor is being established for a run toward £70.00.

Latest Analyst Opinions and Valuation

- JPMorgan: Upgraded to Overweight with a target price of £69.50.

- Goldman Sachs: Maintains a Buy rating, citing the high free cash flow (FCF) yield.

- Latest Valuation: Trading at a forward P/E of approximately 11.2x, which remains below historical peaks during previous commodity booms.

- Latest Dividend: Maintained a policy of 40%–60% payout, with current yields hovering around 4.38%—one of the most stable in the FTSE 100.

- Antofagasta (ANTO) - The Pure-Play Copper Compounded

Latest Business Model and Operational Update Antofagasta is the premier "pure-play" copper miner on the FTSE. Its latest business model is centered on the Centinela Phase 2 expansion. This $4.4 billion project is the centerpiece of its 2026 outlook, expected to add 170,000 tonnes of copper equivalent annually. The company has successfully navigated Chile’s regulatory landscape, securing long-term water and energy stability.

Key Drivers and Outlook

- Supply Scarcity: With global copper deficits projected to reach 330 kmt in 2026 (J.P. Morgan data), Antofagasta’s unhedged production offers maximum exposure to rising prices.

- Operational Resilience: Unlike diversified peers, ANTO’s focus on the high-grade Chilean districts allows for tight cost controls.

- Gold By-product: Rising gold prices (forecasted near $4,000/oz by some analysts) provide a significant credit to their copper production costs.

Current Technical Analysis The stock has seen an "impressive" 18.7% monthly gain in early January 2026. It is currently testing the 2,500p psychological barrier. Momentum oscillators like the RSI are approaching overbought territory (75+), suggesting a brief period of cooling before the next leg up.

Latest Analyst Opinions and Valuation

- Goldman Sachs: Recently double-upgraded to Buy with a "Positive Catalyst Watch" and a price target of 4,000p.

- Deutsche Bank: Downgraded to Sell, warning that the stock has "decoupled from the underlying copper price" due to its scarcity value.

- Latest Valuation: The company trades at a premium to its peers (P/E ~20x), reflecting its high-quality asset base and lack of exposure to "riskier" commodities like coal.

- Latest Dividend: Announced an interim dividend of $0.17, showing a significant year-on-year increase in payout ratios.

- Glencore (GLEN) - The Transition Alpha Play

Latest Business Model and Operational Update Glencore has undergone a radical strategic restructuring. After deciding not to spin off its coal business (following investor feedback), it is now using its massive coal cash flows to fund its "Copper 1 Million" plan. The goal is to produce 1 million tonnes of copper annually by 2028. Its latest operational update highlights a partnership with Chile’s Codelco and the restart of the Alumbrera mine in Argentina.

Key Drivers and Outlook

- Marketing Engine: Glencore’s unique trading arm allows it to profit from market volatility and supply chain dislocations, a feature other miners lack.

- The "V" Recovery: After a year of underperformance in 2025, 2026 is viewed as the "catch-up" year as operational issues in African assets are resolved.

- Capital Allocation: Glencore is targeting $1 billion in recurring cost savings by the end of 2025, which will bolster the 2026 bottom line.

Current Technical Analysis GLEN is showing a "Rounded Bottom" formation on the daily chart, typically a precursor to a long-term trend reversal. The stock has broken above 480p, and analysts are watching the 500p mark as a critical breakout point that could trigger algorithmic "buy" signals.

Latest Analyst Opinions and Valuation

- Berenberg: Upgraded from Hold to Buy, raising the price target to 480p.

- Morgan Stanley: Rated Overweight, citing the stock's significant undervaluation relative to its copper peers.

- Latest Valuation: Trading at a discount to the sector with a forward P/E of roughly 9.5x.

- Latest Dividend: While the base dividend remains variable, share buybacks are expected to be the primary tool for shareholder returns in 2026.

Strategic Risks for 2026

- Geopolitical Tariffs: Potential 25% US tariffs on refined copper (Section 232) could disrupt trade flows and create price premiums in Western markets.

- China Demand: While AI and grid infrastructure drive growth, a slowdown in the Chinese property sector remains a persistent "headwind" for bulk commodities like iron ore.

- Cost Inflation: Despite falling energy prices, "social inflation" and higher labor costs in South America and Australia continue to squeeze margins.

Please wait processing your request...

Please wait processing your request...