Key Takeaways

- FTSE 100 & 250 Drop: UK stocks fell ~1.6% and ~1.5% after the government abandoned planned income tax rises.

- Gilt Yields Surge: 10-yr up ~10bps, 30-yr up ~12bps — higher borrowing costs for businesses and households.

- GBP Weakens: Pound fell ~0.5% vs USD, impacting import costs and investor confidence.

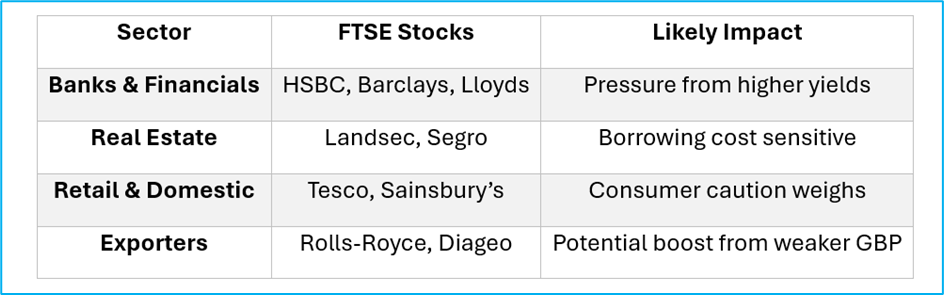

- Banks & Financials Hit Hard: HSBC (LSE: HSBA), Barclays (LSE: BARC), and Lloyds (LSE: LLOY) faced higher funding costs.

- Real Estate & Domestic Sectors Under Pressure: Land Securities (LSE: LAND), Segro (LSE: SGRO), Tesco (LSE: TSCO), J Sainsbury (LSE: SBRY) affected by borrowing costs and consumer caution.

- Exporters May Benefit Slightly: Rolls-Royce (LSE: RR), Diageo (LSE: DGE) see potential lift from weaker GBP, though global risk sentiment remains key.

- Fiscal Credibility in Focus: Market confidence shaken; risk-off sentiment may persist until 26 Nov Budget.

- Investor Strategy: Monitor gilt yields, GBP trends, and sector rotations; diversification remains key.

- Headline Shock: FTSE Reacts

When the Treasury signalled a sudden abandonment of planned income tax increases ahead of the 26 Nov Budget, markets responded quickly:

- FTSE 100: ~1.9% drop

- FTSE 250: ~1.7% drop

- GBP/USD: fell ~0.5% to 1.3159

- Gilt yields: climbed, reflecting rising funding costs and investor caution

Source: EODHD/Others, 14 November 2025

- Why Markets Are Watching Closely

Fiscal Credibility Questions

- The reversal raises concerns about the government’s ability to close the £20–30 billion fiscal gap.

- Bond markets reacted to potential unfunded commitments; yields across maturities jumped.

- Resulting risk premiums affect equities, credit, and currency channels.

Sector Sensitivity

- Domestic banks & financials: HSBC, Barclays, Lloyds — higher funding costs and slower credit growth.

Source: EODHD/Others, 14 November 2025

- Real estate/property: Landsec, Segro — valuations pressured by rising borrowing costs.

Source: EODHD/Others, 14 November 2025

- Retail/domestic demand: Tesco, Sainsbury’s — consumer caution amid uncertainty.

Source: EODHD/Others, 14 November 2025

- Exporters/multinationals: Rolls-Royce, Diageo — currency boost potential but still sensitive to global demand.

Source: EODHD/Others, 14 November 2025

- Currency & Bond Mechanics

- Rising gilt yields → higher borrowing costs for businesses and households

- Weaker GBP → import costs rise, pressuring corporate margins

- Interconnected effect: fiscal uncertainty → yields → currency → equities → sector performance

Source: EODHD/Others, 14 November 2025

- Retail Investors: What to Monitor

26 Nov Budget: Clarity on fiscal policy may trigger volatility

- Gilt yields & curve movements: Signal confidence and borrowing cost trends

- GBP/USD movements: Indicate macro stability or risk-off sentiment

- Sector rotation: Domestic vs export-heavy companies may diverge

- Stock sensitivity table:

Analysis: Kalkine Group

- Final Word: Analytical Take

The budget U-turn may ease growth pressure (no new tax hikes) but raises questions about funding credibility. This duality creates uncertainty for FTSE 100 & 250, gilts, and GBP. Market participants should track sector-specific sensitivities and macro signals as clarity develops ahead of the 26 Nov Budget.

Please wait processing your request...

Please wait processing your request...