The Scoop: Why Did VEIL Pop on Christmas Eve?

While most of the FTSE 250 was winding down for the holidays, Vietnam Enterprise Investments Limited (LSE: VEIL) delivered a solid ~1% gain on December 24, 2025, closing at GBX 781. This wasn't just random holiday volatility; it was a calculated move driven by three massive catalysts converging at year-end.

Source: Kalkine Group

- The "Tender Offer" Adrenaline Shot The biggest driver right now is the 10% Tender Offer announced mid-December. VEIL is actively buying back up to 10% of its own shares to narrow the discount between its share price and its Net Asset Value (NAV).

- Why it matters: Buybacks artificially increase demand. Investors are piling in, knowing the fund is committed to defending its share price.

- The "Emerging Market" Upgrade Hype FTSE Russell officially announced Vietnam’s upgrade to Secondary Emerging Market status earlier this quarter (effective late 2026). The market is now "front-running" this massive inflow of institutional capital. VEIL, as a proxy for the Vietnam index, is the easiest way for London investors to ride this wave.

- Window Dressing & NAV Growth With Vietnam's GDP projected to hit near 8% for 2025, the underlying portfolio (banks, real estate, retail) is on fire. The VN-Index is hovering near historic highs (~1,800 points). Fund managers are "window dressing" their portfolios before year-end, snapping up winners like VEIL to show them on their books for Q4.

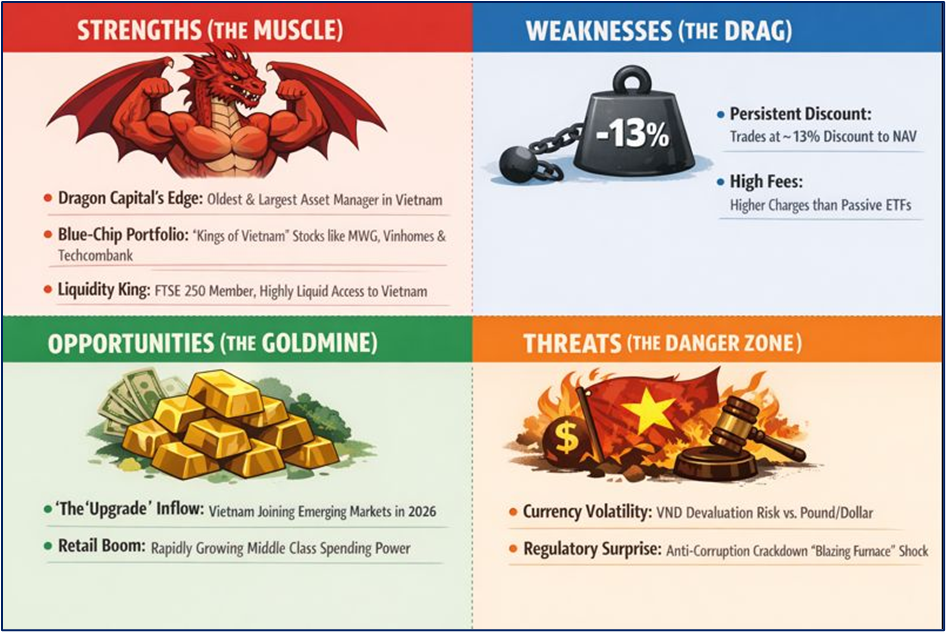

SWOT Analysis

Source: Kalkine Group

Strengths (The Muscle)

- Dragon Capital's Edge: Managed by the oldest and largest asset manager in Vietnam. They have "first call" on major IPOs and deals.

- Blue-Chip Portfolio: Heavily weighted in "Kings of Vietnam" stocks like Mobile World, Vinhomes, and Techcombank. These are cash-rich giants dominant in their sectors.

- Liquidity King: As a FTSE 250 constituent, it’s one of the most liquid ways to trade Vietnam during London hours.

Weaknesses (The Drag)

- Persistent Discount: Despite the jump, VEIL still trades at a ~13% discount to its actual Net Asset Value (NAV of ~890p). You are buying £1 of assets for 87p—good for buyers, but bad for long-term sentiment if it doesn't close further.

- High Fees: The ongoing charge ratio is historically higher than passive ETFs, eating into pure beta returns.

Opportunities (The Goldmine)

- The "Upgrade" Inflow: When Vietnam officially enters the Emerging Market index in 2026, billions of dollars from passive trackers (Vanguard, BlackRock) must buy Vietnamese stocks. VEIL’s holdings will skyrocket.

- Retail Boom: Vietnam's middle class is the fastest growing in SE Asia. VEIL’s heavy bet on consumer discretionary (retail, banking) captures this direct spending power.

Threats (The Danger Zone)

- Currency Volatility: If the Vietnamese Dong (VND) devalues against the Pound/Dollar due to US tariffs (a lingering threat in late 2025), gains in Vietnam get wiped out when converted back to GBP.

- Regulatory Surprise: The Vietnamese government’s anti-corruption crackdown ("Blazing Furnace") is good long-term but can cause sudden, sharp panic selling in real estate stocks.

Latest Business Model: How VEIL Makes Money

VEIL is not a standard company; it is a Closed-End Fund.

- Core Strategy: They take capital raised in London and deploy it into high-growth Vietnamese companies (both listed on the Ho Chi Minh Exchange and pre-IPO).

- Active Management: Unlike an ETF that just buys the index, VEIL’s managers (Dragon Capital) actively rotate sectors. In late 2025, they have pivoted aggressively into Digital Banking and Industrial Real Estate to capitalize on the "China Plus One" manufacturing shift.

- Value Extraction: They use their size to demand better governance from Vietnamese companies, often unlocking value that retail investors can't access.

Critical Financial & Operational Updates (Dec 2025)

- NAV per Share: ~889p - 897p (Estimated).

- Share Price: 781p.

- Discount: Narrowed to ~13% (down from ~18% average earlier in the year).

- Top Holdings Performance:

- Mobile World Corp: Surged on strong holiday electronic sales.

- Vinhomes: Recovering fast as new land laws clear property development backlogs.

- Dividend Policy: VEIL focuses on capital growth, not income. Don't expect a yield; expect price appreciation.

The Risks: What Could Go Wrong?

- The "Trump Trade" / Tariff Fears: With global trade tensions high, any new US tariffs on Vietnamese exports (solar, steel) could crush the manufacturing sector, which is a key engine of VEIL's portfolio. 2. The Liquidity Trap: While liquid in London, the underlying Vietnamese market can freeze up during panics. If VEIL needs to sell assets to fund the tender offer during a crash, they might take a haircut. 3. Frontier Volatility: Despite the upgrade news, Vietnam is still officially a "Frontier" market until 2026. Expect wild swings—1% up days can easily be followed by 3% down days.

Conclusion

The ~1% rise on December 24, 2025, is a bullish signal that the market is waking up to VEIL's deep value. The combination of share buybacks, robust GDP growth, and the inevitable index upgrade creates a powerful tailwind for 2026. For the aggressive investor, VEIL offers a rare chance to buy high-growth assets at a double-digit discount. However, this is not a "set and forget" stock—it requires a stomach for emerging market rollercoasters.

Please wait processing your request...

Please wait processing your request...