Videndum PLC (LSE: VID) has been one of the most volatile stories on the London Stock Exchange this December. After a brutal 55% plunge on December 23rd following a massive refinancing announcement, the stock staged a modest recovery of ~3.3% on December 24, 2025, closing at approximately GBX 13.95.

While a 3.3% gain might seem like a drop in the ocean compared to recent losses, it signals a critical moment of price discovery. Here is the analytical breakdown of what is driving this content-creation titan.

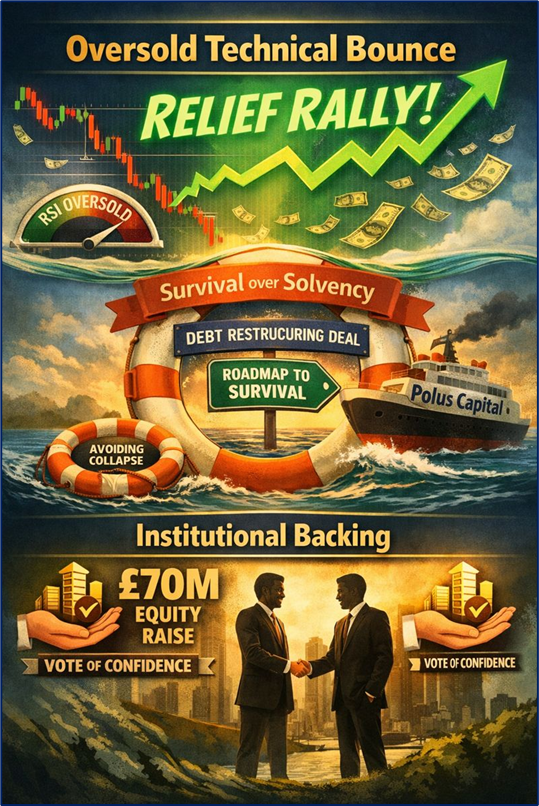

Key Drivers: Why the 3.3% Bounce?

The uptick on Christmas Eve was largely driven by technical "bottom-fishing" and a reassessment of the company’s survival odds.

Source: Kalkine Group

- Oversold Technical Bounce: Following a two-day crash that wiped out half the company's market cap, the Relative Strength Index (RSI) hit extreme oversold territory. Traders often step in at these "pivot bottoms" for a short-term relief rally.

- Survival over Solvency: The massive refinancing plan—while dilutive—effectively removes the immediate "zero-value" threat. By securing a deal with Polus Capital and major shareholders, the company has a roadmap to avoid administration.

- Institutional Backing: The two largest institutional shareholders have indicated support for the £70 million equity raise, providing a "vote of confidence" that there is still a business worth saving.

Latest Business Model: The Leaner Content-Capture Machine

Videndum has evolved from a broad hardware conglomerate into a more focused provider of mission-critical tools for the "Creator Economy."

- Two-Division Streamlining: The company has consolidated its operations to improve efficiency, moving away from its previous three-division structure.

- Direct-to-Creator Focus: With 90% of revenue coming from content creators and 80% of that deemed "mission-critical," the model focuses on high-end brands like Manfrotto, Gitzo, and Teradek.

- Asset Disposals: The recent sale of the JOBY brand to VIJIM for £5 million highlights a shift away from lower-margin consumer products toward professional-grade hardware and software.

Financial & Operational Updates (December 2025)

The financial landscape for Videndum is a tale of "short-term pain for long-term stability."

The Refinancing Nuclear Option

- Equity Raise: A proposed £70 million cash injection via new shares.

- Debt-to-Equity: Conversion of £23 million of debt into equity.

- Net Debt Reduction: Pro-forma net debt is expected to drop from £143.3 million (as of Nov 30) to approximately £52 million.

- The Catch: Existing shareholders face massive dilution, with new shares likely issued significantly below the 20p nominal value.

Operational Performance

- Order Book Momentum: As of Q3 2025, the order book was up 40% year-on-year, particularly in the US.

- Cost Savings: On track for £15 million in FY25 savings, with an annualized "exit rate" of £19 million by the end of 2025.

- Market Recovery: A forecast 80% increase in new productions (Q2 to Q3) suggests the "Cine and Scripted TV" market is finally awakening after the 2024 strikes.

SWOT Analysis: The Hard Truth

Source: Kalkine Group

Critical Risks to Watch

Investors shouldn't mistake a 3.3% bounce for a "clear runway." Several hurdles remain:

- The Dilution Wall: The exact pricing of the £70m equity raise will dictate the "floor" for the share price. If priced at a deep discount, the 13.95p level may not hold.

- Execution Risk: The refinancing is expected to complete by Q1 2026. Any delay or failure to gain shareholder approval could trigger a "no recovery" scenario for existing holders.

- Macro Volatility: Uncertainty regarding US trade policies continues to make distributors hesitant to hold large inventories.

Conclusion

Videndum’s 3.3% climb on December 24th is a classic "relief rally." The company is successfully pivoting from a debt-laden crisis toward a stabilized, albeit heavily diluted, future. While the operational turnaround (rising order books and cost savings) is visible, the financial restructuring is the primary driver of the current share price. For the retail observer, the story is no longer about "will they survive," but rather "what is the fair price of the new, diluted entity?"

Please wait processing your request...

Please wait processing your request...