The final trading day of 2025 delivered a quiet but significant win for Vodafone Group PLC (LSE: VOD). While many blue-chip stocks drifted into the new year, Vodafone’s FTSE 100 listing nudged up ~1% on December 31, 2025. This move wasn't a fluke; it was the culmination of a "Year of Simplification" that has fundamentally altered the company’s DNA.

For retail investors, the 1% gain represents a vote of confidence in CEO Margherita Della Valle’s aggressive restructuring. Here is the deep-dive analysis of why the market is suddenly re-rating this telecom legacy.

The Dec 31 "Spark": Key Drivers of the Upward Tick

The move on December 31 was fueled by two major catalysts that hit the wires just as the markets prepared to close:

Source: Kalkine Group

- The India "Resolution" Bonus: News broke that Vodafone Group reached a definitive settlement regarding its long-pending liabilities in India (Vodafone Idea). By formalizing an amendment to the 2017 Implementation Agreement, the group clarified its maximum exposure, removing a massive "cloud of uncertainty" that has suppressed the stock price for years.

- Guidance Reaffirmation: In a year-end sentiment boost, internal data suggested that the German market—Vodafone’s largest and most troubled—has officially hit its "inflection point," returning to service revenue growth after five quarters of decline.

Latest Business Model: From "Global Giant" to "Lean Operator"

Vodafone has spent 2025 shedding its "imperial" skin. The latest business model is built on three distinct pillars:

- The Growth Core: Africa (Vodacom) and Turkey. These regions are now the group's "earnings engine," delivering double-digit organic growth through data demand and M-Pesa financial services.

- The Value Core: Germany and the UK. Following the merger with Three UK (completed mid-2025) and the sale of Spain/Italy, Vodafone is now the UK’s largest mobile operator. The focus here is "Value over Volume"—raising prices and cutting costs rather than chasing low-value subscribers.

- Vodafone Business (B2B): This is no longer just about sim cards. The model has shifted toward Digital Services (Cloud, IoT, and Cybersecurity), which grew at 12%+ in H2 2025.

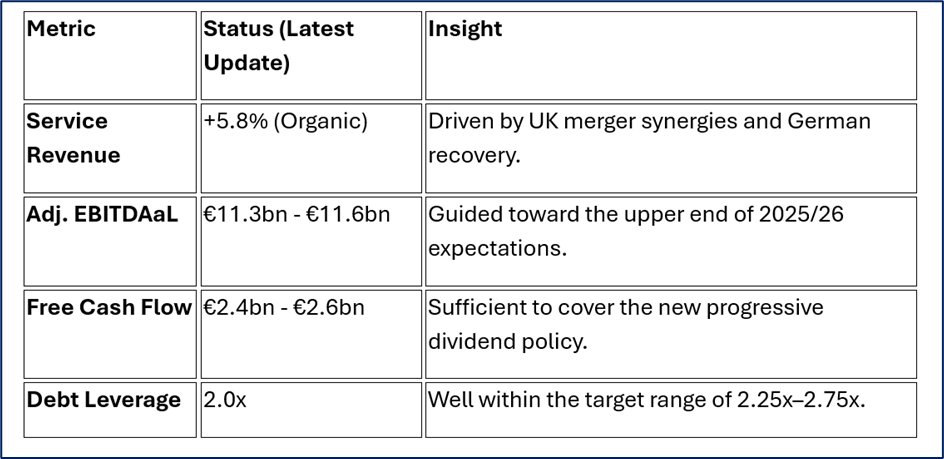

Operational & Financial Health Check (2025 Updates)

The numbers suggest a "slingshot" effect is forming for 2026:

Source: Company Data

SWOT Analysis: The 2026 Retail Outlook

Source: Kalkine Group

Strengths

- Market Leadership: Post-merger, Vodafone is the #1 player in the UK and a dominant force in Germany.

- Financial Services: M-Pesa in Africa continues to be a "fintech unicorn" hidden inside a telecom shell.

- Aggressive Buybacks: The completion of €2bn in share buybacks has supported the floor price.

Weaknesses

- German Cable Churn: Transitioning away from bulk TV laws in Germany is still causing minor subscriber "leakage."

- Capital Intensity: 5G Standalone (SA) and fiber rollouts continue to demand massive CapEx.

Opportunities

- GenAI Integration: Vodafone is currently deploying "SuperTOBi" (AI agent) across all markets to slash customer service costs.

- Satellite Connectivity: New partnerships in LEO (Low Earth Orbit) satellites aim to eliminate "not-spots" without building expensive towers.

Threats

- Regulatory Scrutiny: Continuous monitoring of the UK merger's impact on consumer pricing.

- Hyper-Inflationary Markets: Turkey remains a high-growth but high-risk currency environment.

The Risk Landscape

While the 1% gain is positive, the road to 2026 is not without potholes. The primary risk remains macro-economic pricing pressure. If European consumers face a renewed cost-of-living squeeze, Vodafone’s "Value over Volume" strategy (price hikes) could lead to higher-than-expected churn. Furthermore, the integration of "Three UK" is a multi-year project; any execution hiccups could delay the expected £500m in annual synergies.

Conclusion: A New Era of Predictability

Vodafone’s performance on December 31, 2025, reflects a market that is finally beginning to trust the management’s "Simplicity" narrative. By exiting underperforming markets (Spain, Italy) and resolving legacy liabilities (India), Vodafone has transformed from a complex, debt-heavy conglomerate into a predictable, cash-generative utility with a "growth kicker" in Africa.

For the retail observer, 2026 looks to be less about "recovery" and more about "execution." The stock is no longer trying to reinvent itself—it is simply trying to run a tighter ship.

Please wait processing your request...

Please wait processing your request...