Market Analysis: The Mining Momentum of January 26, 2026

The London Stock Exchange witnessed a significant rotation into the basic materials sector on January 26, 2026, as the "green metal" thesis and precious metal resilience combined to propel the FTSE 100's mining heavyweights. Antofagasta, Endeavour Mining, and Anglo American emerged as the day's standout performers, buoyed by a cocktail of record-breaking commodity prices and strategic corporate maneuvers.

As copper prices breached the $13,000 per tonne mark and gold miners benefited from a broader flight to safety amid global geopolitical tensions, these three titans demonstrated the potent operational leverage inherent in the current mining super-cycle.

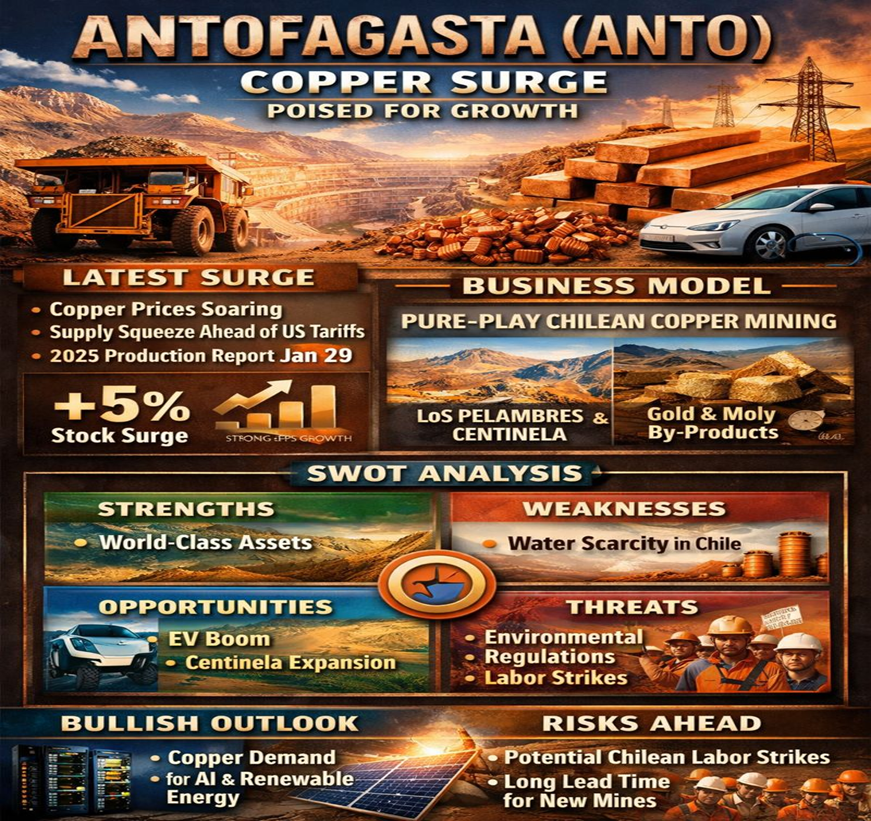

Antofagasta (ANTO)

Source: Kalkine Group

The Chilean copper specialist saw its shares surge by over 5% in early trading, cementing its position as a primary beneficiary of the global electrification trend.

- Latest Surge Drivers: The primary catalyst for the January 26 surge is the relentless climb in copper prices, driven by a widening global deficit. Traders are "front-loading" imports due to fears of upcoming US tariffs on refined copper, creating a supply squeeze that Antofagasta is perfectly positioned to exploit. Additionally, anticipation for the Q4 2025 production report (scheduled for Jan 29) has investors betting on strong year-end volumes.

- Current Business Model: Antofagasta operates a high-margin, pure-play copper mining model centered in Chile. It focuses on large-scale, low-cost assets like Los Pelambres and Centinela, complemented by gold and molybdenum by-products that act as cost offsets.

- Financial & Operational Updates: In its latest half-year results, management reported a significant jump in EBITDA and a doubling of underlying EPS, highlighting its operational leverage (Antofagasta H1 2025 Report). The company is currently maintaining its 2025 production guidance while advancing the Los Pelambres expansion.

- SWOT Analysis:

- Strengths: Pure-play exposure to copper; world-class Chilean assets.

- Weaknesses: Geographic concentration in Chile; exposure to local water scarcity.

- Opportunities: Expansion of the Centinela Second Concentrator; rising EV demand.

- Threats: Tightening Chilean environmental regulations; volatile energy costs.

- Outlook & Risks: The outlook remains bullish as long as copper demand for AI data centers and renewable grids persists. However, risks include potential labor strikes in Chile and the 18-year lead time for new mine discoveries, which limits rapid supply response.

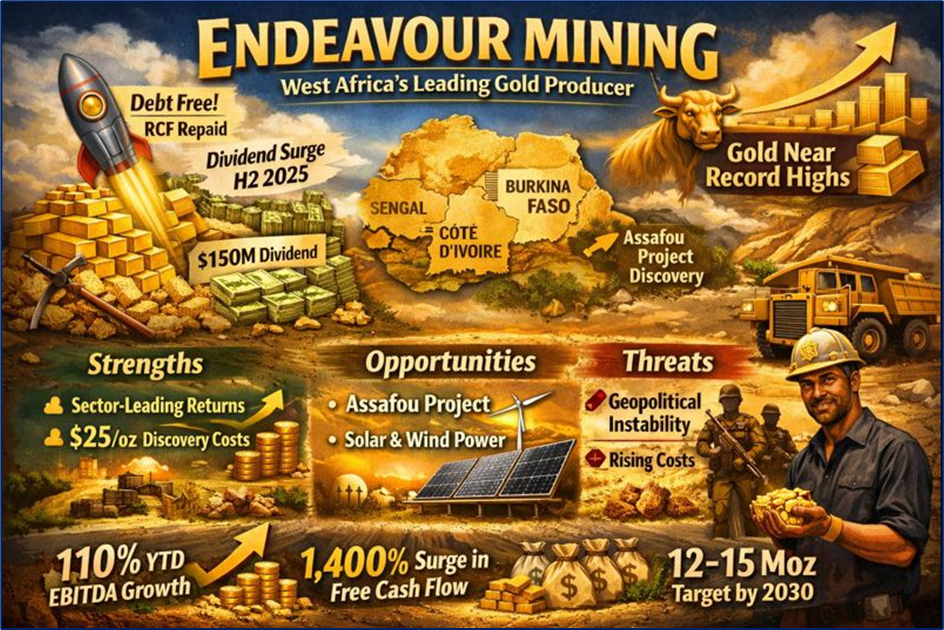

Endeavour Mining (EDV)

Source: Kalkine Group

As the largest gold producer in West Africa, Endeavour Mining rallied by more than 4% as investors sought refuge in bullion-backed assets.

- Latest Surge Drivers: Gold miners are rallying as the yellow metal nears historic highs. For Endeavour specifically, the market is reacting to the company's aggressive debt reduction—having fully repaid its Revolving Credit Facility (RCF)—and the impending announcement of its H2 2025 dividend, expected to significantly exceed minimum commitments.

- Current Business Model: Endeavour focuses on high-grade, low-cost gold production in the Birimian Greenstone Belt across Senegal, Côte d'Ivoire, and Burkina Faso. Its strategy emphasizes organic growth through the "drill bit," targeting 12–15 million ounces of new discoveries by 2030.

- Financial & Operational Updates: The company reported a 110% increase in Year-To-Date (YTD) Adjusted EBITDA and a record $150 million dividend paid in October 2025 (Endeavour Q3 2025 Results). Free cash flow surged by over 1,400% compared to the previous year.

- SWOT Analysis:

- Strengths: Sector-leading shareholder returns; low discovery costs ($25/oz).

- Weaknesses: Operations localized in high-risk West African jurisdictions.

- Opportunities: Discovery of the Assafou project; integration of solar/wind power to lower AISC.

- Threats: Geopolitical instability; inflationary pressure on royalty costs.

- Outlook & Risks: Management targets a "top half" production guidance for the full year. Key risks involve security concerns in Burkina Faso and fluctuating gold prices which directly impact royalty expenses.

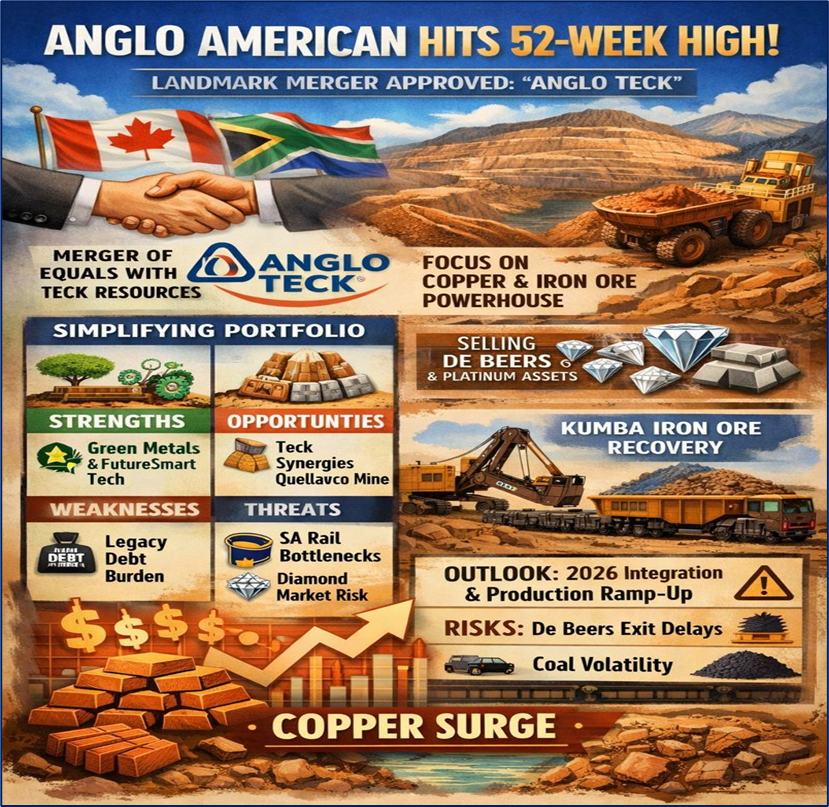

Anglo American (AAL)

Source: Kalkine Group

Anglo American hit a new 52-week high today, driven by structural portfolio shifts and the "premiumization" of its commodity basket.

- Latest Surge Drivers: Beyond the copper price rally, Anglo is riding the wave of its landmark "merger of equals" with Teck Resources to form "Anglo Teck." Shareholders and the Canadian government recently approved the deal, which will create a simplified copper and iron ore powerhouse.

- Current Business Model: Anglo is in the midst of a radical simplification, divesting non-core assets like De Beers (diamonds) and platinum group metals to focus on "future-enabling" products: copper, premium iron ore, and crop nutrients.

- Financial & Operational Updates: Anglo and Teck received Investment Canada Act approval in late December 2025, clearing the path for the merger (Anglo American Press Release, Dec 16, 2025). The company is also seeing production recovery in its Kumba iron ore division as South African rail logistics slowly improve.

- SWOT Analysis:

- Strengths: Highly diversified "green metal" portfolio; industry-leading FutureSmart Mining™ tech.

- Weaknesses: Legacy debt from previous capital-intensive projects.

- Opportunities: Synergies from the Teck merger; ramp-up of the Quellaveco copper mine.

- Threats: South African infrastructure (Transnet) bottlenecks; diamond market volatility (De Beers).

- Outlook & Risks: The outlook is centered on the 2026 integration with Teck and reaching steady-state production at Quellaveco. Risks include potential delays in the De Beers separation and continued volatility in the steelmaking coal exit.

Compelling Conclusion

The surge in Antofagasta, Endeavour, and Anglo American on January 26 reflects a broader market realization: the transition to a low-carbon economy is resource-intensive. While each company faces unique regional and operational risks, their collective ascent underscores the critical role of mining in the 2026 global economy. Whether it is the pure-play copper leverage of Antofagasta, the cash-flow-heavy gold production of Endeavour, or the strategic rebirth of Anglo American, these stocks remain the primary vehicles for investors looking to navigate the intersection of commodity scarcity and industrial evolution.

Please wait processing your request...

Please wait processing your request...