Views Expressed Disclaimer:

You are reading a free article with opinions that may differ from the recommendation given by Kalkine in its paid research reports. Become a Kalkine member today to get access to our research reports, in-depth technical and fundamental research.

Burberry has entered 2026 under significant market pressure, with its share price falling more than 7% year-to-date by late February. This underperformance stands in stark contrast to the broader FTSE 100, which has been approaching record levels. The decline reflects more than short-term volatility—it highlights a combination of structural industry challenges, regional macroeconomic headwinds, and the risks associated with Burberry’s ambitious transformation strategy.

As the company advances its “Burberry Forward” turnaround plan, investors are closely watching whether the brand can restore growth momentum while navigating a cooling luxury market.

Source: Kalkine Group

A Cooling Luxury Market Is Weighing on Sentiment

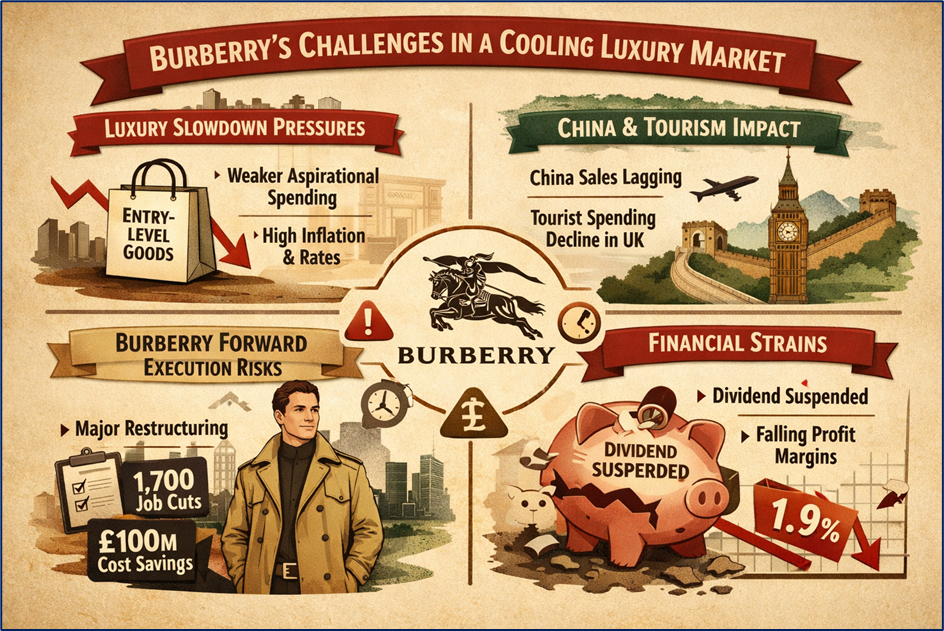

One of the most important factors behind Burberry’s weak share performance is the broader slowdown across the global luxury sector. After the surge in spending that followed pandemic lockdowns, consumer demand has normalized considerably.

A key pressure point has been the decline in purchases from aspirational consumers—shoppers who typically buy entry-level luxury items such as scarves, accessories, or smaller leather goods. This group is particularly sensitive to inflation, borrowing costs, and economic uncertainty. With interest rates remaining elevated in many regions, discretionary spending has softened, directly affecting brands positioned between premium and ultra-luxury segments.

At the same time, the luxury industry has become increasingly polarized. Ultra-high-end brands with strong pricing power and exclusivity have shown resilience, while more accessible luxury names like Burberry have experienced greater volatility in demand.

China and Tourism Trends Remain Critical Variables

China continues to represent a vital growth driver for Burberry, but the recovery trajectory has been uneven. While the company reported modest improvement—such as mid-single-digit growth in Greater China sales during its fiscal third quarter—the rebound has not matched historical levels.

Beyond domestic demand, shifting global tourism patterns have also created challenges.

The United Kingdom’s removal of VAT refunds for overseas visitors following Brexit has reduced London’s competitiveness as a luxury shopping destination compared with cities such as Paris and Milan. High-spending international tourists, particularly from Asia and the Middle East, increasingly choose alternative European locations where tax-free incentives remain available.

This policy change has had a measurable impact on Burberry’s regional performance, as tourist spending historically represented a meaningful revenue contributor in the UK market.

Execution Risks Surround the “Burberry Forward” Turnaround

Burberry is undergoing a major strategic reset under CEO Joshua Schulman. The “Burberry Forward” initiative aims to reposition the brand around its heritage strengths, particularly outerwear and scarves, while improving operational efficiency.

Encouragingly, core categories linked to the brand’s British identity have shown strong growth, with double-digit increases in key product segments. This suggests the heritage-focused strategy is resonating with consumers.

However, the transformation comes with substantial execution risks.

The company has announced plans to eliminate approximately 1,700 roles and achieve around £100 million in annual cost savings by 2027. While these measures are intended to strengthen long-term profitability, the near-term impact includes restructuring charges estimated at roughly £50 million during fiscal 2026.

Market participants remain cautious about how quickly these initiatives will translate into sustainable earnings improvements. Some analysts have warned that consensus expectations may underestimate the time required for a full turnaround.

Financial Signals: Dividends and Margins Under Pressure

Burberry’s financial metrics have also contributed to investor caution.

The company suspended its dividend in 2024 to preserve cash during the restructuring period. This decision, while strategically prudent, reduced the stock’s appeal for income-focused investors who traditionally favour FTSE dividend payers.

Profitability metrics have also deteriorated. Adjusted operating margins fell sharply, reaching approximately 1.9% in the first half of the fiscal year—well below historical levels. Although sequential improvement was reported later, margins remain significantly compressed, reinforcing concerns about earnings visibility.

Key Performance Snapshot

Share Price: Down more than 7% in 2026

Impact: Negative sentiment and market underperformance

Dividends: Suspended

Impact: Reduced attractiveness for income investors

China Sales: Modest growth returning

Impact: Early signs of stabilization

Core Categories: Strong growth in heritage products

Impact: Strategic validation

Cost Savings Plan: £100 million target by 2027

Impact: Long-term positive, short-term risk

Outlook for Burberry in 2026

Investor sentiment toward Burberry currently reflects a cautious “wait-and-see” approach. The company is demonstrating progress in reconnecting with its heritage identity, and early product performance indicates the brand still holds strong global appeal.

However, several uncertainties remain:

- The pace of recovery in luxury demand, particularly among aspirational consumers

• Economic conditions in China and global tourism flows

• The effectiveness and timing of restructuring benefits

• Margin normalization and potential dividend reinstatement

For Burberry to regain market confidence, it must show that its strategic reset can deliver not only brand desirability but also consistent profit growth and stronger operating margins.

If execution improves and macro conditions stabilize, the current period could represent a transitional phase rather than a structural decline. Until then, the stock is likely to remain sensitive to both sector trends and evidence of tangible financial progress.

Please wait processing your request...

Please wait processing your request...