The AIM market witnessed a dormant volcano erupt today. On December 30, 2025, Galantas Gold Corporation (LSE: GAL) saw its share price surge by approximately 67%, leaving retail investors and institutional analysts scrambling to parse the data. This isn't just a "dead cat bounce"—it is the culmination of a radical business model pivot and a massive acquisition in the heart of the world's most prolific mining districts.

The Catalyst: The "Indiana Jones" Move in Chile

The primary driver for today’s 67% explosion is the finalized update regarding the acquisition of RDL Mining Corp. This move effectively transforms Galantas from a single-asset Northern Irish miner into a multi-jurisdictional powerhouse.

Source: Kalkine Group

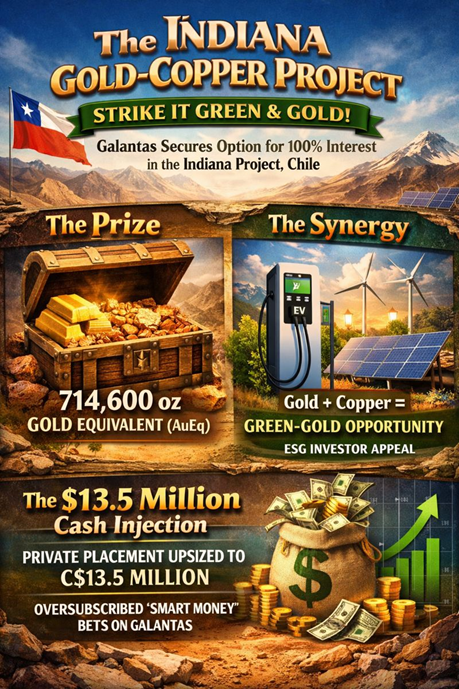

- The Indiana Gold-Copper Project

Through RDL, Galantas has secured an option to acquire a 100% interest in the Indiana Project in Chile.

- The Prize: An inferred resource estimate of approximately 714,600 ounces of gold equivalent (AuEq).

- The Synergy: With copper prices hitting record highs due to the global electrification push, the gold-copper mix at Indiana makes this a "green-gold" play, attracting a much broader ESG-focused investor base.

- The $13.5 Million Cash Injection

Institutional confidence followed the acquisition. Galantas upsized its private placement to C$13.5 million at $0.08 per unit. The fact that the financing was "upsized" indicates heavy oversubscription—a clear signal that "smart money" is betting on the new management's direction.

Latest Business Model: From "Operator" to "Strategic Partner"

Galantas has undergone a quiet but profound shift in its business model in 2025:

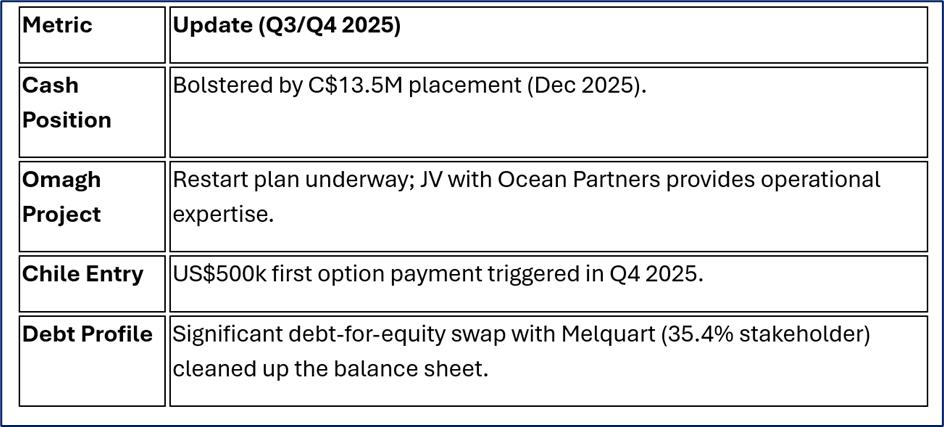

- The Joint Venture (JV) Strategy: In September 2025, Galantas closed a massive JV with Ocean Partners UK. Ocean Partners now owns 80% of the Omagh Project and acts as the operator.

- The "Free Carry" Benefit: Galantas is now free-carried on the initial $3 million investment for exploration at Omagh. This allows Galantas to retain a 20% interest (or convert to a 3% Net Smelter Royalty) without the crushing overhead of day-to-day operations.

- Strategic Focus: The company is now a lean exploration and development vehicle, focusing its remaining capital on high-upside targets in Chile and Scotland (Gairloch Project) rather than getting bogged down in the operational complexities of Northern Ireland.

Financial & Operational Health Check

Source: Company Data

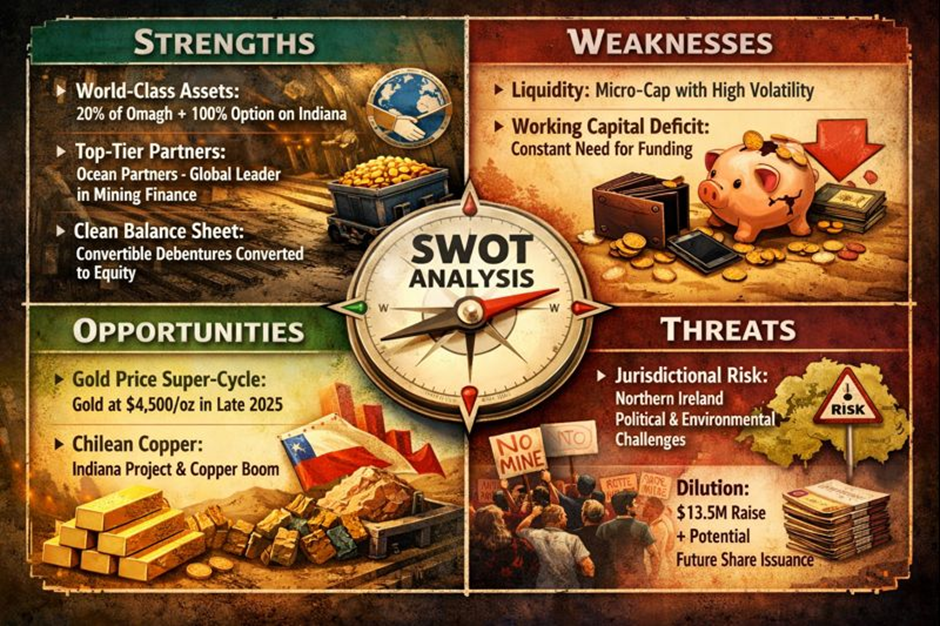

SWOT Analysis: The Hard Truths

Source: Kalkine Group

Strengths

- World-Class Assets: Holding a 20% stake in Omagh plus 100% option on Indiana (Chile).

- Top-Tier Partners: Ocean Partners is a global leader in concentrate marketing and mining finance.

- Clean Balance Sheet: Conversion of convertible debentures into equity has removed the immediate "insolvency" overhang seen in late 2024.

Weaknesses

- Liquidity: Despite the surge, the stock remains a micro-cap with high volatility.

- Working Capital Deficit: Historic filings showed a deficit that requires constant capital raises to bridge the gap to production.

Opportunities

- Gold Price Super-Cycle: Gold hit record highs near $4,500/oz in late 2025. Galantas is a high-beta play on this price.

- Chilean Copper: The Indiana project provides exposure to the copper supply crunch.

Threats

- Jurisdictional Risk: Operating in Northern Ireland remains politically and environmentally sensitive.

- Dilution: The recent $13.5M raise issued 168 million units; future raises could further dilute existing shareholders.

The Risks: Why You Should Watch Your Step

While a 67% gain is intoxicating, the "Galantas Gamble" is not without thorns:

- Permitting Hurdles: Chile is pro-mining but has stringent environmental regulations that could delay the Indiana Project.

- Execution Risk: The company must now prove it can transition from an explorer to a developer under a new board structure.

- Gold Price Volatility: Any pullback in the underlying commodity will hit micro-cap miners twice as hard.

Conclusion

The 67% move on December 30, 2025, marks the market finally pricing in the Chilean transformation. By offloading the operational burden of Omagh to Ocean Partners and acquiring a massive resource in Chile, Galantas has effectively "re-relisted" itself as a high-growth explorer. For retail investors, the story is no longer about a struggling mine in County Tyrone—it's about a diversified gold-copper junior with enough cash to survive 2026.

Please wait processing your request...

Please wait processing your request...