The London Stock Exchange closed its 2025 books with a surprising spark from Norcros PLC (LSE: NXR). While the broader FTSE indices saw muted holiday trading, Norcros shares jumped ~5.6% on 31 December 2025, ending the year at a high of approximately 327p.

This year-end rally wasn’t just "Santa Claus" momentum; it was the culmination of a year spent aggressively pivoting from a heavy manufacturer to a high-margin, asset-light powerhouse.

The "New Year" Drivers: Why the 5.6% Jump?

Several factors converged to trigger the New Year's Eve surge:

Source: Kalkine Group

- Window Dressing & Valuation Gap: Leading into the final day of 2025, analysts noted that Norcros was trading at a significant discount to its peers despite a Strong Buy consensus. Value-seeking institutional investors likely rebalanced portfolios, recognizing its 9.7x P/E ratio was undervalued relative to its 18.2% EPS growth forecast.

- The "Fibo" Factor Realized: With the acquisition of Norwegian firm Fibo (waterproof wall panels) fully integrated by Q4, the market finally priced in the "earnings-accretive" nature of the deal.

- Institutional Confidence: Recent director share dealings in late November and December 2025 signaled internal confidence, often a catalyst for retail "follow-the-leader" buying.

- Dividend Anticipation: With the next interim dividend payment of 3.7p per share scheduled for 13 January 2026, investors moved to secure positions before the new year.

Latest Business Model: Asset-Light & Design-Led

Norcros has fundamentally shifted its DNA. Previously known for capital-intensive tile manufacturing, the 2025/2026 business model is built on three pillars:

- Outsourced Manufacturing: By exiting tile production (closing Johnson Tiles UK and South Africa units), they have moved to a capital-light model, sourcing high-quality products while focusing on design and IP.

- The "One Norcros" Scale: They leverage a unified operating platform for sourcing, logistics, and technology across brands like Triton, Vado, and Croydex, reducing overhead.

- Mid-Premium Positioning: They focus on the Repair, Maintenance, and Improvement (RMI) market, which is far more resilient than the volatile new-build housing sector.

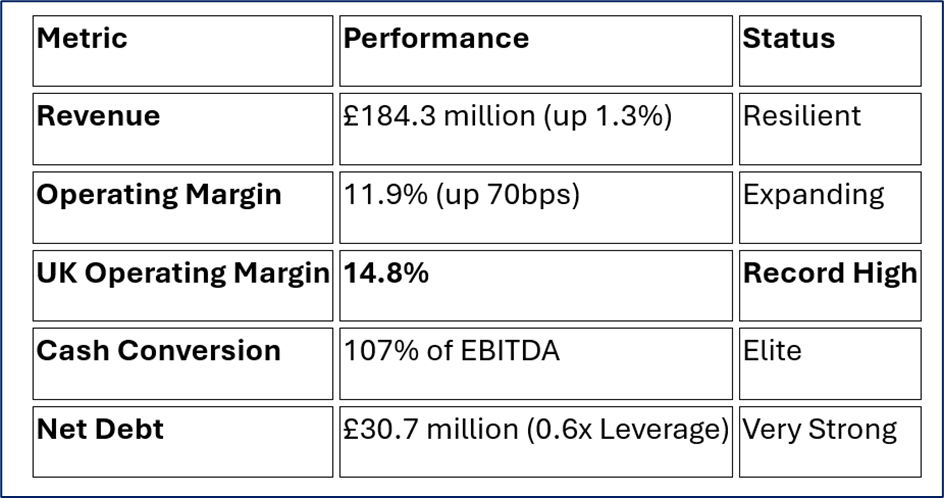

Operational & Financial Health Check (FY 2026 Interims)

The latest data from the H1 2026 report (period ended 5 Oct 2025) paints a picture of a business "hiding in plain sight":

Source: Company Data

Strategic SWOT Analysis

Source: Kalkine Group

Strengths

- Brand Power: Market leader in UK bathroom products with household names like Triton.

- Operational Efficiency: Successful exit from low-margin manufacturing has boosted the ROCE to 18.1%.

- Financial Discipline: Exceptionally high cash conversion allows for self-funded M&A.

Weaknesses

- South African Volatility: While recovering, the South African market remains a drag on overall group margins compared to the UK.

- Concentration: A heavy reliance on the UK RMI market makes them sensitive to British consumer confidence.

Opportunities

- Fibo Synergies: Huge potential to cross-sell Norwegian wall panels into the established UK trade network.

- ESG Leadership: Their "Sustainable Products Framework" aligns with increasing regulatory and consumer demand for eco-friendly bathrooms.

- M&A Runway: Low leverage (0.6x) provides a "war chest" for more acquisitions in 2026.

Threats

- Input Costs: Fluctuations in freight and raw material costs (especially eco-fuels) could pinch margins.

- Macro Headwinds: High interest rates in South Africa and a potentially slow recovery in the UK new-build sector.

Key Risks to Watch in 2026

- Integration Risk: While Fibo is a great fit, any hiccups in European expansion could stall momentum.

- Supply Chain Shift: As they move to more "eco-fuels" for shipping (target of 20% by 2026), logistics costs may see short-term spikes.

- Consumer Spending: If the UK economy enters a deeper recession, even "essential" bathroom repairs may be delayed.

The Verdict

Norcros ended 2025 as a Lean, Green, Margin-Machine. The 5.6% spike on 31 December suggests that the market is finally waking up to the fact that this is no longer a "boring" tile company, but a highly efficient, design-led distributor with world-class cash flow.

Please wait processing your request...

Please wait processing your request...