In the 2026 investment landscape, the FTSE Utilities sector has transitioned from a sleepy "widows and orphans" income play into a dynamic engine for wealth compounding. This shift is fueled by a "Golden Age of Infrastructure," where the dual demands of AI data centre power and the net-zero energy transition are driving unprecedented capital expenditure.

Below is an analytical deep dive into three FTSE utilities positioned for potential outperformance through 2026.

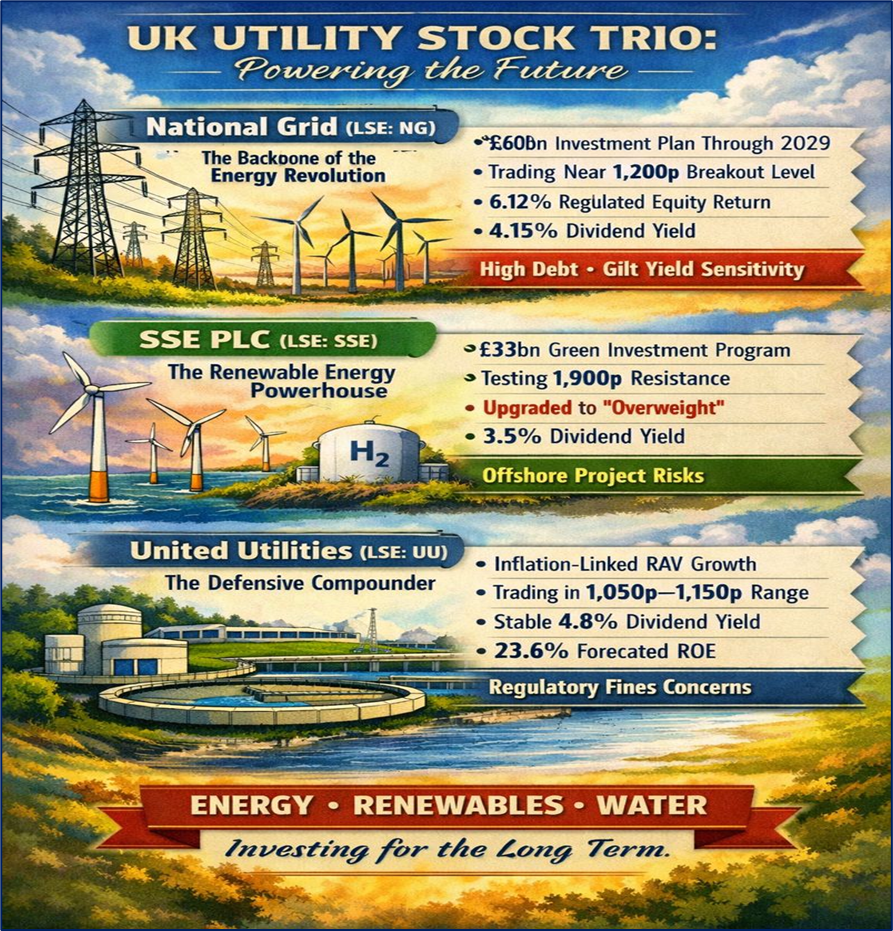

Source: Kalkine Group

The Backbone of the Energy Revolution

National Grid stands as the primary beneficiary of the UK’s massive grid reinforcement. As the owner of the high-voltage transmission system, it is the "toll booth" through which all new renewable power must pass.

- Key Drivers & Business Model: The company is executing a £60 billion investment plan through 2029. Its model has pivoted toward "pure-play" networks, selling off non-core assets like Grain LNG to focus on high-growth electricity transmission.

- Technical Analysis: As of early 2026, NG is trading near its 52-week highs of 1,180p–1,200p. After a successful consolidation above the 1,100p support level, the MACD shows a sustained bullish crossover on the monthly chart. Technical resistance is thin above 1,210p, suggesting a "blue sky" breakout if capital inflows continue.

- Analyst Outlook & Smart Money: Major institutions like Barclays and JPMorgan maintain "Buy" ratings with price targets revised upward to 1,250p+. "Smart money" sentiment is bolstered by Ofgem’s RIIO-T3 framework, which recently set a 6.12% equity return, providing the regulatory certainty that hedge funds crave for long-term compounding.

- Financials & Dividend: The current yield sits at approximately 4.15%, with a progressive policy aiming for 6–8% EPS growth. Latest results show a 17% jump in operating profit, though high CapEx has led to a temporary negative free cash flow—a common trait in high-growth utility cycles.

- Risks: High debt-to-equity ratios and sensitivity to sudden spikes in long-dated Gilt yields.

The Renewable Energy Powerhouse

SSE has transformed from a traditional supplier into a leading developer of offshore wind and flexible thermal power, making it a favorite for ESG-focused global fund managers.

- Key Drivers & Business Model: SSE is midway through a £33 billion investment program. Its business model is uniquely integrated, combining "Networks" (transmission/distribution) with "Renewables" and "Flexibility" (pumped hydro and gas-to-hydrogen).

- Technical Analysis: The stock has recently broken out of a multi-year horizontal channel. It is currently testing the 1,900p resistance zone. Volume profiles indicate heavy accumulation by institutional desks around the 1,750p mark. A sustained move above 1,950p targets a psychological 2,200p level.

- Analyst Outlook & Smart Money: Goldman Sachs and Morgan Stanley have highlighted SSE as a "Thematic Champion" for 2026. Brokers have recently upgraded the stock to "Overweight," citing its 7–9% EPS CAGR guidance through 2030 as conservative given the accelerating pace of electrification.

- Financials & Dividend: SSE offers a dividend yield of roughly 3.5%–4%, with a policy targeting 5–10% annual growth. Latest updates confirm a 22% increase in capital investment, largely funneled into its SSEN Transmission wing.

- Risks: Weather-related volatility (low wind speeds) and execution risks on massive offshore projects like Dogger Bank.

The Defensive Compounder

While electricity takes the headlines, United Utilities represents the "pure defensive" play with a massive regulatory asset base (RAV) that is inflation-linked, providing a hedge against "sticky" 2026 inflation.

- Key Drivers & Business Model: Operating primarily in the North West of England, UU is focused on the AMP8 regulatory period, which involves the largest environmental investment program in the water sector’s history.

- Technical Analysis: The stock exhibits low-beta stability, currently trading in a horizontal range between 1,050p and 1,150p. A "Double Bottom" formation was noted in late 2025, providing a technical floor. It is viewed as a "bond proxy" with an upward-sloping 200-day moving average.

- Analyst Outlook & Smart Money: Simply Wall St and EODHD/Others data show a consensus "Hold/Accumulate" rating. While it lacks the explosive growth of SSE, it is being bought by "Value" funds for its 23.6% forecast Return on Equity (ROE) over the next three years.

- Financials & Dividend: It maintains one of the sector's most reliable yields at approx 4.8%. EPS has shown a significant rebound (35p in H1 2026 vs 15p in H1 2025).

- Risks: Regulatory fines regarding sewage discharge remain a headline risk, and the heavy debt burden requires careful management as interest rates stay "higher for longer."

Sector Risks & Conclusion

The utility sector in 2026 faces a unique paradox: it is more relevant than ever due to AI and Net Zero, yet it is capital-intensive. Risks include regulatory tightening, cost-of-debt increases, and political intervention in consumer pricing.

Conclusion: For wealth compounding, National Grid offers the most stable grid-exposure, SSE provides the highest growth potential through renewables, and United Utilities serves as the inflation-hedged anchor.

Please wait processing your request...

Please wait processing your request...