Aston Martin shares remain highly volatile in February 2026 — but could strategic restructuring, ultra-luxury positioning, and upcoming model launches trigger a sustainable turnaround?

Key Takeaways – February 2026 (Latest Market Data)

- FTSE 250-listed Aston Martin Lagonda (LSE: AML) gained +4.9% on 10 February 2026, signalling renewed short-term buying interest.

- The 52-week trading range of 56p–122p highlights extreme volatility and swing-trading behaviour.

- No dividend policy (0% yield) — the company prioritises reinvestment and debt stabilisation.

- Average 12-month analyst price target: ~GBP 69.27, implying modest upside.

- UK macro trends, global luxury demand, and USD/GBP foreign exchange dynamics remain major valuation drivers.

What Is Aston Martin’s Share Price Performance as of 10 February 2026?

As of 10 February 2026, Aston Martin Lagonda shares closed around 63.20p, advancing +4.9% in a single session and outperforming segments of the broader mid-cap market.

However, despite the recent rebound:

- The stock remains approximately 40–45% lower year-on-year.

- Price swings within the 56p–122p range confirm elevated risk and speculative trading patterns.

- Momentum appears technically driven rather than fundamentally anchored.

This positions AML as a high-beta FTSE 250 recovery play, rather than a stable income stock.

Does Aston Martin Pay Dividends in 2026?

No. Aston Martin Lagonda does not currently pay dividends.

- Dividend yield: 0.00%

- Payout ratio: 0%

- Capital allocation priority: operational restructuring and balance sheet stabilisation.

Unlike many FTSE 250 peers, AML focuses on cash reinvestment, product development, and liquidity preservation, typical of turnaround-stage automotive companies.

Income-focused investors may therefore look elsewhere in the UK equity market.

How Is the FTSE 250 and UK Economy Affecting AML Stock?

As a member of the FTSE 250 Index, AML is particularly sensitive to:

- UK GDP growth trends

- Domestic consumer confidence

- Export demand and trade policy

- GBP currency volatility

Recent UK economic softness — including weaker manufacturing output and export pressures — has weighed on mid-cap cyclicals.

Additionally:

- A stronger GBP can reduce export competitiveness.

- A weaker GBP may support overseas luxury pricing but increase import costs.

For a luxury automotive exporter like Aston Martin, currency shifts are material earnings drivers.

What Are Analysts Forecasting for AML in 2026?

Consensus analyst data indicates:

- Average 12-month price target: ~GBP 69.27

- Implied upside: modest from current levels

- Ratings range: Hold to Buy

Broker forecasts remain cautious due to:

- Earnings volatility

- Uncertain sales volume trajectory

- High leverage and credit pressure

While upside exists, conviction remains mixed.

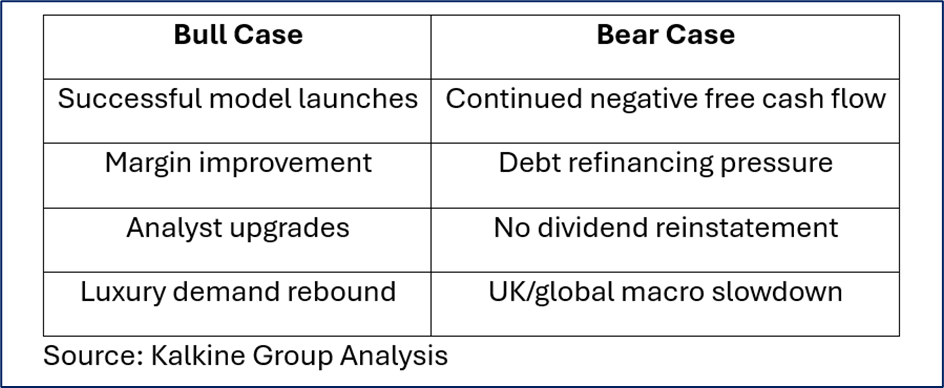

What Are the Core Drivers Behind Aston Martin’s February 2026 Price Move?

Bullish Catalysts

- +4.9% short-term price momentum

- Strong global brand equity and luxury positioning

- New model launches and ultra-luxury product mix

- Potential analyst upgrades if earnings stabilise

Bearish Pressures

- No dividend income support

- Negative EPS and ongoing operational losses

- Credit concerns (recent downgrade to CCC+ territory)

- UK macro and global luxury demand sensitivity

The recent rally appears tactical rather than structural.

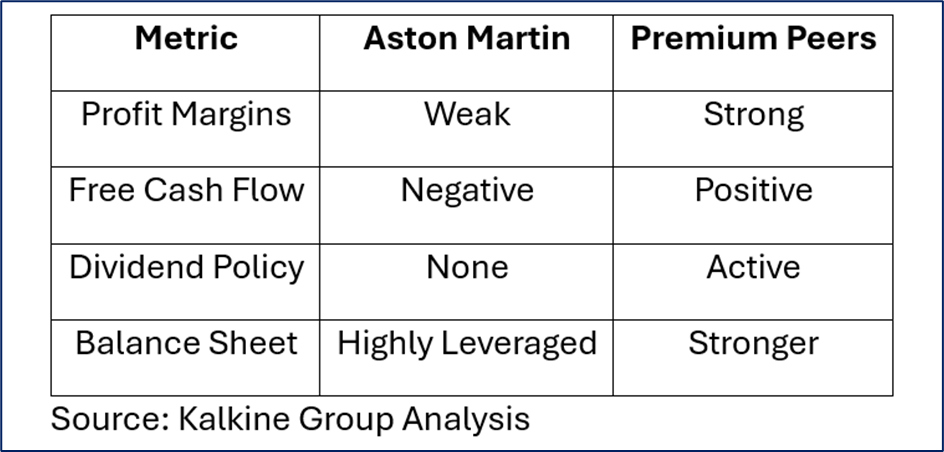

How Does Aston Martin Compare to Industry Peers?

Aston Martin competes within the global luxury automotive segment against stronger cash-generating peers such as:

- Ferrari

- BMW

- Mercedes-Benz Group

Compared to these competitors:

AML’s brand prestige is undeniable, but financial execution lags sector leaders.

Is Aston Martin Stock Bullish or Bearish Across Time Horizons?

Short-Term (0–3 Months): Neutral–Bullish

Technical rebound and trading momentum could continue.

Medium-Term (3–12 Months): Neutral

Analyst targets suggest mild upside, but earnings uncertainty caps enthusiasm.

Long-Term (1+ Year): Neutral–Bearish

Sustainable upside depends on:

- Margin expansion

- Debt reduction

- Consistent positive free cash flow

Without those, AML risks lagging premium automotive peers.

What Strategic Actions Should Retail Investors Consider?

For Short-Term Traders (3–6 Months)

- Monitor weekly price trends and FTSE 250 sentiment.

- Use volatility strategically.

- Consider risk-managed approaches (e.g., hedging strategies).

For Medium-Term Investors

- Watch quarterly earnings and cash flow progression.

- Track model launch performance.

- Monitor debt reduction initiatives.

For Long-Term Investors

- Focus on structural turnaround evidence.

- Evaluate balance sheet improvement.

- Avoid speculation-driven entries without earnings validation.

Bull vs Bear Scenario Matrix

What Are the Primary Investment Risks?

- High leverage and credit rating vulnerability

- No dividend income support

- Cyclical luxury demand exposure

- Currency and tariff risks

- Execution risk on restructuring strategy

AML remains a high-risk, high-volatility equity.

FAQ – Aston Martin Lagonda Shares 2026

Q: Does Aston Martin pay dividends in 2026?

A: No, the company currently has no dividend policy.

Q: Is AML stock oversold?

A: Short-term technical rebounds suggest trading interest, but fundamentals remain fragile.

Q: Should retail investors buy AML now?

A: Only investors with high risk tolerance and awareness of turnaround volatility should consider exposure.

Final Investment Outlook – February 2026

Aston Martin Lagonda’s +4.9% surge on 10 February 2026 reflects tactical buying momentum rather than confirmed operational recovery.

While the brand’s luxury positioning, product pipeline, and restructuring initiatives provide potential upside, ongoing losses, debt pressure, and macroeconomic uncertainty continue to constrain valuation expansion.

For global retail investors seeking UK mid-cap exposure, AML remains:

- A speculative recovery candidate

- A volatility-driven trading vehicle

- Not currently an income investment

A sustained rally will depend not on short-term price spikes — but on clear improvements in profitability,

Please wait processing your request...

Please wait processing your request...