As the curtain closes on 2025, XAAR PLC (LSE: XAR) has signaled to the market that its long-term "Ultra High Viscosity" bet is finally paying off. On December 30, 2025, Xaar shares climbed approximately 4.08%, closing at ~GBX 102.

While the broader FTSE All-Share remained relatively flat, Xaar’s late-year rally suggests investors are looking past historic headwinds and toward a massive 2026.

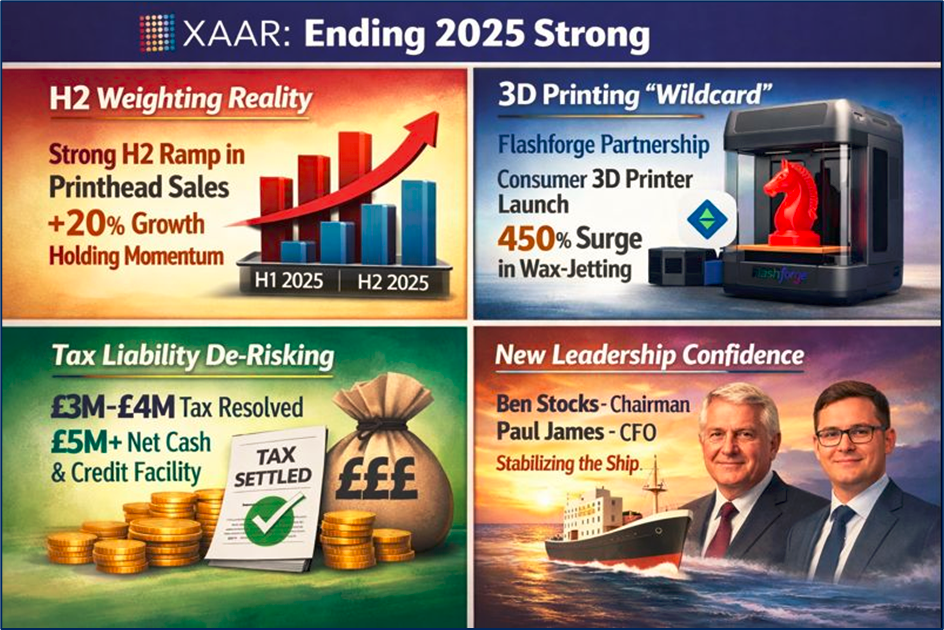

The Pulse: Key Drivers Behind the 30 Dec 2025 Rally

The year-end bump wasn't a fluke; it was the result of a "perfect storm" of operational execution and strategic clarity:

Source: Kalkine Group

- H2 Weighting Reality: Management had consistently signaled that 2025 revenue would be heavily skewed toward the second half. As the year ends, data suggests the ramp-up in Printhead sales—which saw 20% growth earlier in the year—held its momentum.

- The 3D Printing "Wildcard": A major catalyst in late Q4 was the anticipated launch of a consumer-priced desktop 3D printer powered by Xaar technology. This partnership (notably with Flashforge) is expected to mirror the success of Xaar’s wax-jetting business, which exploded by 450% in H1 2025.

- Tax Liability De-risking: Earlier in Oct 2025, Xaar disclosed a £3M–£4M overseas tax liability. By Dec 30, the market has fully "baked this in," viewing the company’s £5M+ net cash and £5M undrawn credit facility as more than sufficient to handle the settlement without stalling R&D.

- New Leadership Confidence: The appointment of Ben Stocks as Chairman and Paul James as permanent CFO has stabilized the "ship," providing institutional investors with the governance confidence needed to increase positions.

Latest Business Model: From "One-Trick Pony" to Diversified Powerhouse

Xaar has undergone a radical transformation. No longer solely dependent on the volatile ceramics market, its 2025 business model rests on three pillars:

- Direct-to-Shape & Advanced Manufacturing: Using "ImagineX" technology to jet fluids 100x more viscous than competitors. This is the "secret sauce" for EV battery coatings (Sokan partnership) and automotive two-tone painting (Axalta/Dürr).

- Turnkey Solutions: Rather than just selling a component (the printhead), Xaar now provides integrated systems (via EPS and Megnajet). This increases the "stickiness" of their revenue.

- The "Fee-per-Car" Potential: Xaar is exploring recurring revenue models in automotive digital coatings, moving away from purely cyclical hardware sales.

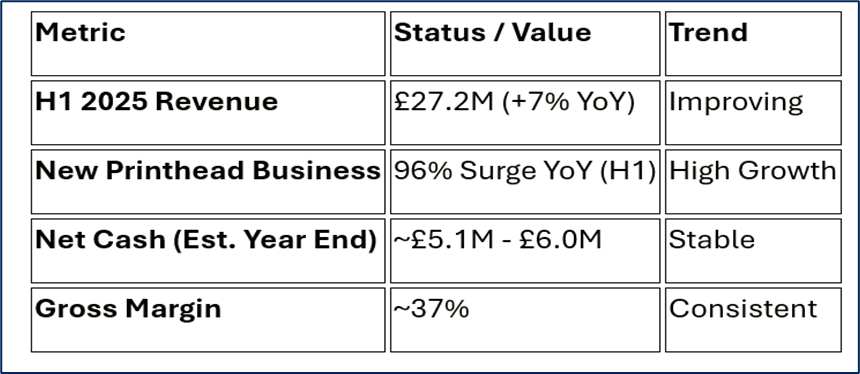

Financial & Operational Performance (2025 Snapshots)

Source: Company Data

Operational Milestone: In November 2025, Xaar successfully transitioned 100% of its UK operations to renewable gas, cutting Scope 1 emissions by 60%. This ESG milestone has made the stock more attractive to "green" institutional funds.

SWOT Analysis: Xaar at the Edge of 2026

Source: Kalkine Group

Strengths

- Technological Moat: Only company capable of reliably jetting fluids at 100 centipoise (cP).

- Strong IP: Over 280 patents creating high barriers to entry.

- Diversified Portfolio: 40–50 different applications across 15+ active projects.

Weaknesses

- High P/E Ratio: Trading at a premium, making the stock sensitive to any missed earnings.

- Historical Volatility: A legacy of "mixed" years makes some retail investors cautious.

Opportunities

- EV Battery Market: An estimated £260M opportunity for battery coatings.

- AI Integration: Using AI to optimize "waveforms" for customers, shortening the sales cycle from months to weeks.

- 3D Printing Expansion: Disrupting the desktop 3D market with high-resolution, low-cost inkjet tech.

Threats

- Geopolitical Tariffs: Global trade tensions continue to impact the Engineered Print Systems (EPS) division.

- Competition: Heavyweights like Fujifilm Dimatix and Ricoh are constantly innovating.

The Risk Landscape

Despite the 4% jump, Xaar is not without peril. The £4M tax liability will weigh on cash flows over the next 24 months. Furthermore, the Ceramics market (once Xaar's bread and butter) continues to be a drag, though it is finally nearing its "trough." Any further slowdown in global manufacturing or a spike in R&D costs could delay the projected return to significant profitability in 2026.

The "Big Picture" Conclusion

Xaar’s 4% climb on December 30, 2025, reflects a growing market consensus: The turnaround is real. By diversifying away from ceramics and dominating high-growth niches like EV batteries and 3D printing, Xaar has built a more resilient, tech-heavy engine.

While the 2025 bottom line may still show the scars of historic tax issues and R&D spend, the "New Printhead" growth (up nearly 100% in H1) is the leading indicator that bulls have been waiting for.

Please wait processing your request...

Please wait processing your request...