Why LSE: ZIG Hit the Accelerator Today?

The market reacted with a surge in share price for Zigup PLC (LSE: ZIG) today, following the release of a robust half-year trading update. The stock, a key player in integrated mobility solutions, saw its value jump approximately 14%, driven by strong operational performance and an optimistic full-year profit forecast. This dramatic single-day move highlights investor confidence in the company's strategic direction amid a dynamic industrial landscape.

Reasons for the Surge: Catalysts and Key Drivers

Profit Forecast Raised: The Core Driver Behind the 14% Jump

The primary catalyst for the stock's significant rise is the company's Interim Results for the six months ended October 31, 2025.

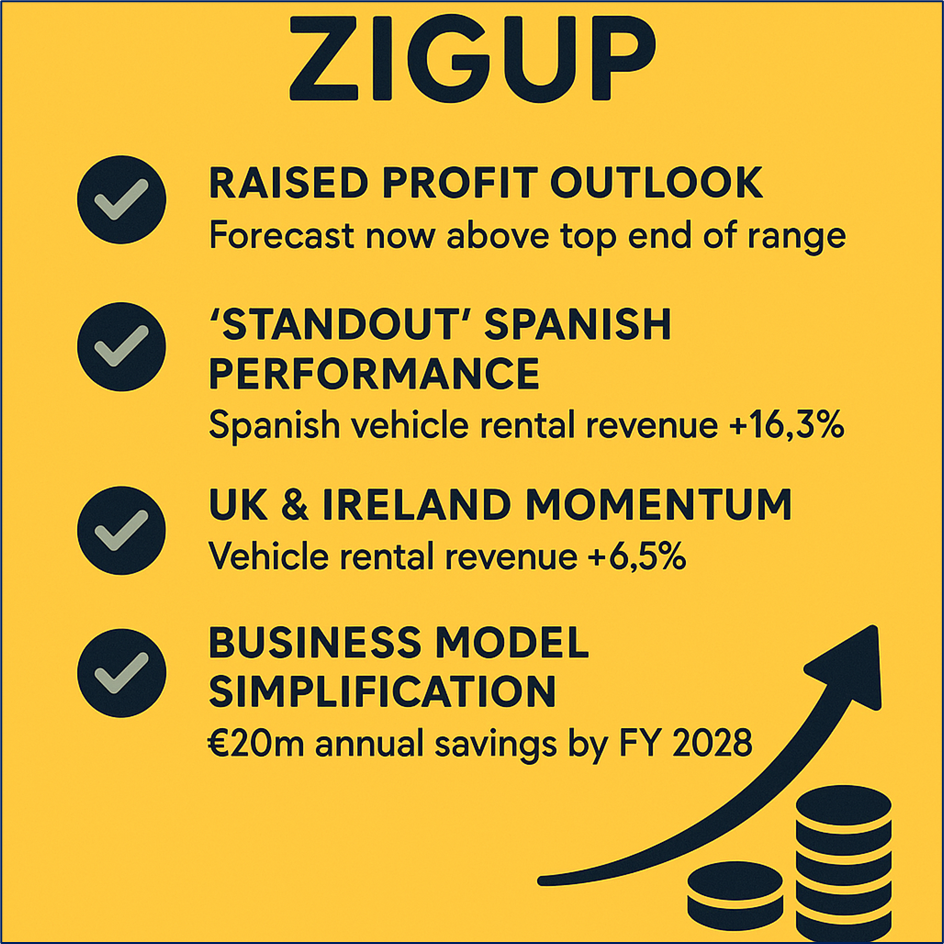

- Raised Profit Outlook: The most impactful news was the expectation that full-year underlying profit before tax is now forecast to be "at least at the top" of the analysts' consensus range (£150 million to £155 million). This signals a stronger-than-expected performance trajectory.

- "Standout" Spanish Performance: The European operations, particularly the Spanish vehicle rental business, delivered a "standout" performance, with vehicle hire revenue rising an impressive 16.3%.

- UK & Ireland Momentum: The core UK & Ireland Rental business showed "good momentum," backed by new fleet wins and expansion of its specialist fleet, driving vehicle hire revenue growth of 6.5%.

- Business Model Simplification: Zigup announced plans to simplify its UK & Ireland operating model around two main units. This simplification is projected to deliver approximately £20 million in annual savings by fiscal 2028, appealing to investors looking for efficiency and margin improvement.

- Reaching a Cashflow "Inflexion Point": The company's disciplined investment in fleet renewal is leading to an expected improvement in cash generation, with steady-state cash flow projected to increase in the years ahead, reaching a critical "inflexion point."

Source: Kalkine Group

Zigup's Business Model and Strategy

From Rental to Full-Cycle Mobility: How Zigup Makes Its Money

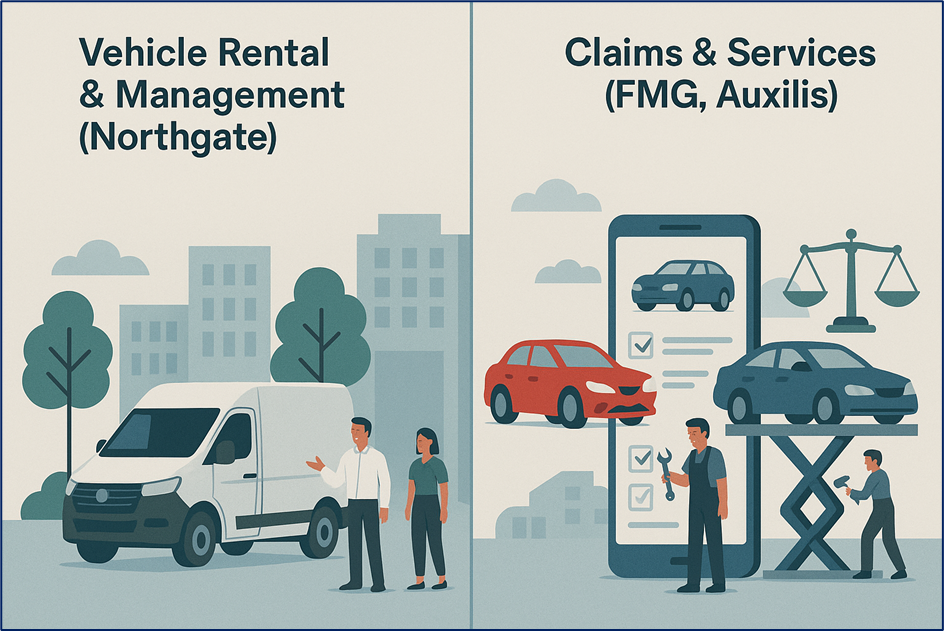

Zigup (formerly Redde Northgate plc) operates as an integrated mobility solutions platform across the vehicle lifecycle in the UK, Ireland, and Spain.

Business Model: The Two Pillars of Revenue

The model is built on two primary segments, offering a high degree of service integration:

- Vehicle Rental & Management (Northgate): This core segment provides long-term and short-term light commercial vehicle (LCV) and passenger vehicle rental and fleet management services to corporate, public sector, and SME customers. Revenue is generated through rental fees and ancillary services like maintenance.

- Claims & Services (FMG, Auxillis): This segment is capital-light and provides technology-enabled mobility and claims solutions. This includes accident management, vehicle repair, mobile repair, and legal/insurance services, ensuring a replacement vehicle is provided and the incident is managed end-to-end. This platform offers sticky, recurring revenue by connecting directly with major insurance partners.

Source: Kalkine Group

Strategic Direction: Positioning for the Electric Future

The strategy is focused on sustainable, technology-enabled growth and operational efficiency.

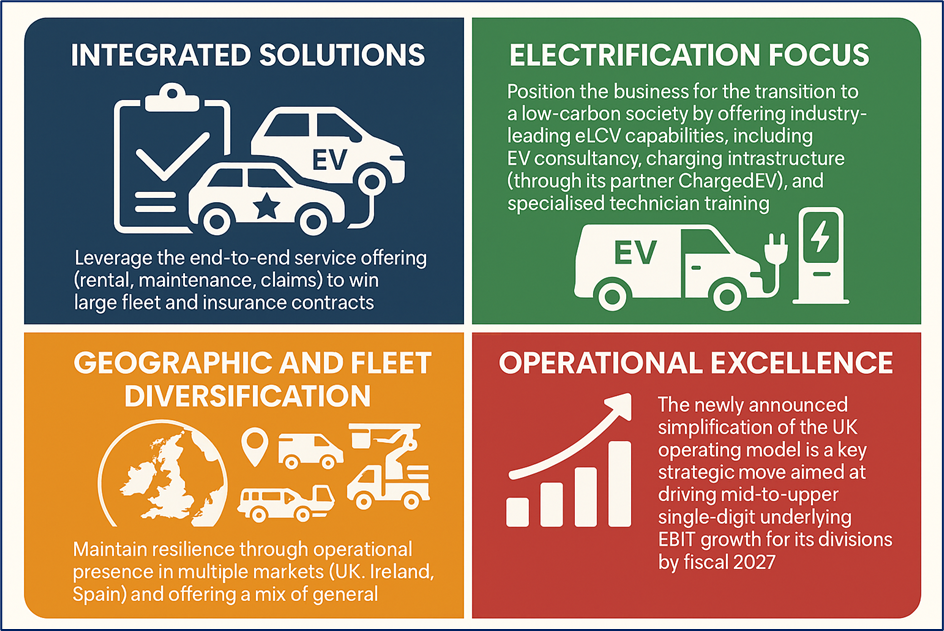

- Integrated Solutions: Leverage the end-to-end service offering (rental, maintenance, claims) to win large fleet and insurance contracts.

- Electrification Focus: Position the business for the transition to a low-carbon society by offering industry-leading eLCV capabilities, including EV consultancy, charging infrastructure (through its partner ChargedEV), and specialised technician training.

- Geographic and Fleet Diversification: Maintain resilience through operational presence in multiple markets (UK, Ireland, Spain) and offering a mix of general and specialist vehicles.

- Operational Excellence: The newly announced simplification of the UK operating model is a key strategic move aimed at driving mid-to-upper single-digit underlying EBIT growth for its divisions by fiscal 2027.

Source: Kalkine Group

Where Does Zigup Go From Here? Growth Drivers and Headwinds

Outlook: Poised for an Uptrend

The company's outlook is currently positive, driven by several structural tailwinds:

- Outsourcing Trend: Increasing numbers of corporate and public sector fleets are choosing to outsource vehicle rental and fleet management to benefit from flexible solutions, lower capital expenditure, and comprehensive service packages.

- EV Transition: Zigup's early focus on eLCVs and the associated infrastructure/consultancy services positions it to capture future growth as businesses pursue their net-zero commitments.

- Attractive Valuation: Despite the high forward P/E ratio, the stock has often been cited by analysts as being undervalued relative to its enterprise value-to-EBITDA, its strong free cash flow generation, and the potential for a lucrative takeover bid, which is common for undervalued UK companies in the current climate.

Key Risks: Managing the Bumps

No investment is without risk, and Zigup faces several potential headwinds:

- Residual Value Risk: As a large purchaser of vehicles, the value of its fleet assets is crucial. A rapid decline in residual values for used vehicles, particularly internal combustion engine (ICE) vehicles as EV adoption accelerates, could negatively impact disposal profits.

- Interest Rate and Debt: The business is capital-intensive, relying on significant debt to finance its fleet assets. Net debt increased to £939 million. While the leverage ratio (1.9x EBITDA) is relatively modest compared to peers, rising interest rates could increase financing costs.

- Claims & Services Volatility: The profitability of the Claims & Services division can be exposed to changes in the regulatory and legal environment, as well as fluctuating claims volumes and costs.

Latest Financial and Operational Snapshots (H1 2026 vs. H1 2025)

The Numbers Tell the Story: Decent Operational Earnings

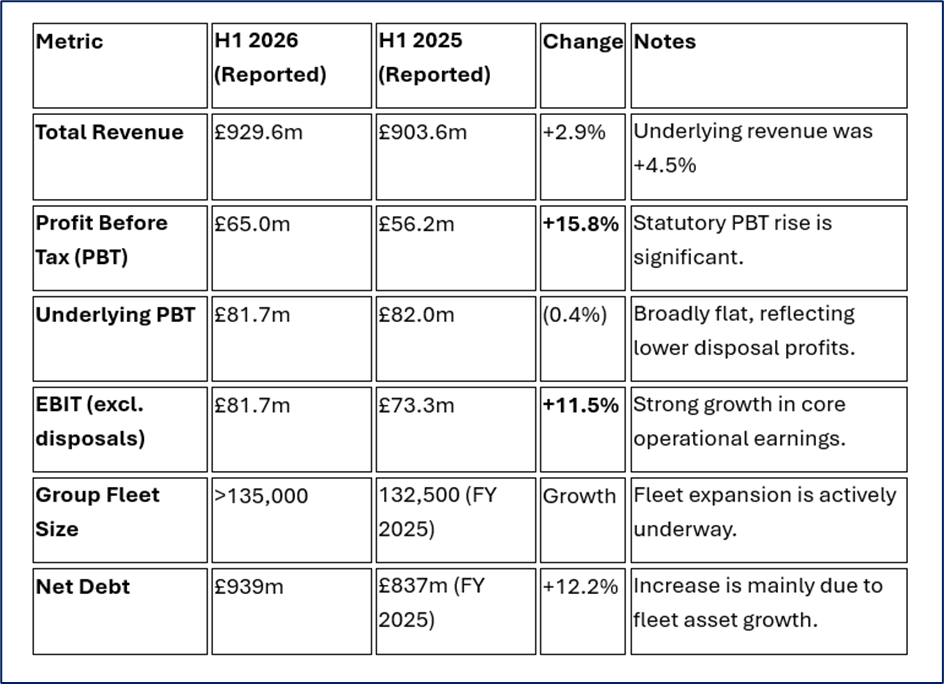

The latest financial results confirm the narrative of operational strength offsetting disposal profit normalisation.

Data Source: Company Fillings, Kalkine Group

Operational Highlights:

- Fleet Wins: Secured a major rail maintenance fleet contract in Spain and a large Fleet Management contract in the UK.

- Insurance: New contract secured with Howden Insurance and a multi-year renewal with Tesco Insurance, reinforcing the Claims & Services platform.

- Technology: Roll-out of an advanced call-centre platform commenced, which includes potential for AI-driven enhancements to boost operational efficiencies.

Conclusion: Is the Mobility Giant Set for a Longer Ride?

Zigup’s 14% stock surge is not a flash in the pan but a decisive market reaction to a solid, detailed set of interim results that confirm a positive operational narrative. The key takeaway for the market is the company’s ability to deliver double-digit operational earnings growth (EBIT ex-disposal profits: +11.5%) and confidently raise its full-year profit guidance, underpinned by robust rental demand in Spain and strategic efficiency gains planned for the UK.

While the underlying PBT remains flat due to the expected normalisation of disposal profits—a factor the market has already digested—the focus is clearly shifting to the sustainable, future-oriented rental and claims platforms. The market has provided a strong vote of confidence that Zigup is successfully navigating its post-pandemic fleet transition and is well-positioned to capitalise on the structural shift toward outsourced, electrified mobility solutions.

Source: Trading View, 3 December 2025, 11:30 AM GMT

Please wait processing your request...

Please wait processing your request...