What Readers Need to Know

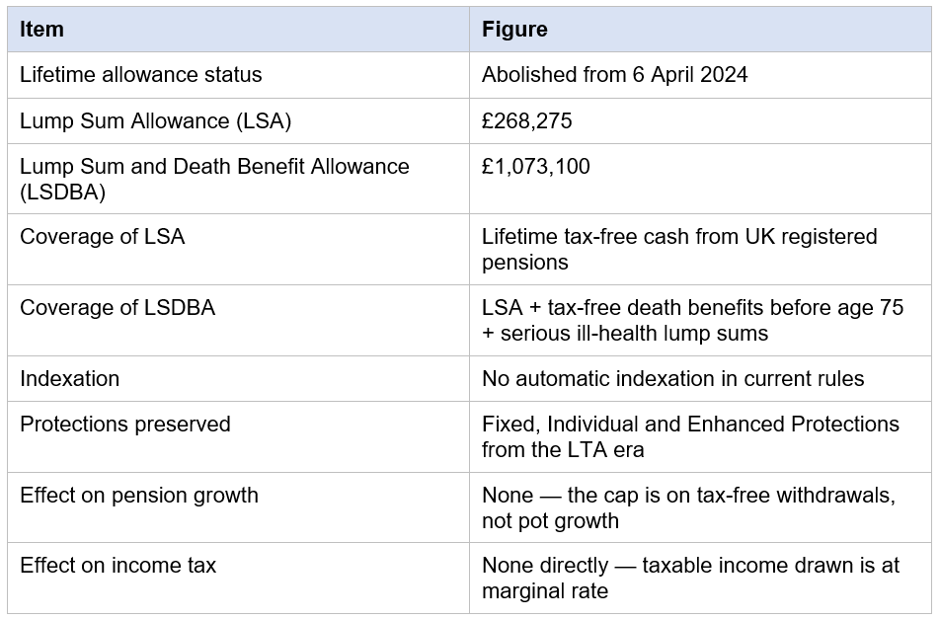

- The UK lifetime allowance (LTA) was abolished from 6 April 2024.

- It has been replaced by the Lump Sum Allowance (LSA) of £268,275 and the Lump Sum and Death Benefit Allowance (LSDBA) of £1,073,100.

- The LSA caps tax-free cash across all UK pensions during the saver's lifetime.

- The LSDBA caps the wider tax-free amount, including death benefits paid before age 75.

- Existing fixed and individual protections may preserve higher allowances for some savers.

Introduction

The UK pension tax framework changed significantly from 6 April 2024 with the abolition of the lifetime allowance and the introduction of two replacement allowances — the Lump Sum Allowance (LSA) and the Lump Sum and Death Benefit Allowance (LSDBA). For savers with large pensions, the replacement rules govern how much can be taken tax-free during life and on death.

This article explains the new framework for UK readers in the 2026/27 tax year. It is general information and not personal advice. Anyone with a large pension or LTA-era protection should review their position with a regulated financial adviser.

The Lifetime Allowance — Brief Background

The lifetime allowance (LTA) was a cap on the total value of UK pension benefits a saver could accumulate without facing additional tax charges on the way out. The LTA had ranged from £1.5 million at its peak to £1,073,100 in the years before abolition. Charges on benefits above the LTA could be punitive — 25% on income drawn over the limit or 55% on lump sums.

Following announcements in the 2023 Spring Budget and confirmation in the Finance Act 2024, the LTA was abolished from 6 April 2024 and replaced by the LSA and LSDBA framework.

The Lump Sum Allowance (LSA)

Once the LSA is fully used, further lump sums from pensions are taxed as income at the saver's marginal rate.

- Pension Commencement Lump Sums (PCLS) — the 25% tax-free cash taken alongside flexi-access drawdown.

- Tax-free element of UFPLS — the 25% tax-free portion of each Uncrystallised Funds Pension Lump Sum.

- Tax-free element of serious ill-health lump sums paid before age 75.

The Lump Sum and Death Benefit Allowance (LSDBA)

The LSDBA effectively caps the lifetime tax-free amount including on death. Death benefits paid above the LSDBA are taxed at the beneficiary's marginal rate.

- All tax-free lump sums during the saver's lifetime (the LSA sits within the LSDBA).

- The tax-free element of death benefits paid before age 75.

- Other relevant lump sums paid out of UK registered pensions.

How the Two Allowances Work Together

Think of the LSA as a subset of the LSDBA. Tax-free cash taken during the saver's lifetime reduces both the LSA and the LSDBA simultaneously. After the saver's death, any remaining LSDBA (after deducting lifetime tax-free cash) determines how much of any death benefit lump sum can be paid tax-free.

How Tax-Free Cash Is Calculated

Under the LSA framework, each pension crystallisation produces a 'relevant lump sum' that reduces the saver's remaining LSA. For a flexi-access drawdown PCLS, the relevant lump sum is the actual tax-free cash taken. For a UFPLS, it is the 25% tax-free element of each Withdrawal. The provider tracks LSA usage and reports it to the saver and HMRC.

Where the saver has multiple pensions, the LSA is shared across all of them — not £268,275 per pension. Total tax-free cash across SIPPs, workplace pensions, SSAS schemes and personal pensions all count towards the same allowance.

Transitional Tax-Free Cash Certificates

Savers who had crystallised pension benefits before 6 April 2024 may need a 'transitional tax-free cash certificate' to establish how much of the LSA they have already used. The standard rule applies a transitional calculation based on the saver's previous LTA usage. Where the calculation is unfavourable, savers can apply for a certificate based on actual tax-free cash taken — sometimes producing a higher remaining LSA.

Specialist advice is essential for any saver who had crystallised pensions before 6 April 2024 and who plans to take further tax-free cash. The certificate application process is technical and has deadlines.

Death Benefits Before and After 75

Death before age 75 normally allows benefits to pass tax-free up to the LSDBA. Death after 75 means beneficiaries pay income tax at their marginal rate on benefits received. The IHT treatment of pension death benefits is the subject of announced future changes; savers should follow current GOV.UK guidance.

Protections from the LTA Era

Protections can be invalidated by certain actions, such as new pension contributions after registering for fixed protection. Anyone with LTA-era protection should review their position with a specialist adviser before contributing further or transferring.

- Fixed Protection 2016 — protected LTA of £1.25 million, with corresponding LSA/LSDBA increases.

- Individual Protection 2016 — protected LTA based on pension value at 5 April 2016, capped at £1.25 million.

- Earlier Fixed and Individual Protection regimes — preserving higher LTAs from 2014 and 2012 frameworks.

- Enhanced Protection — a protection against the original A-Day LTA introduced in 2006.

What the Replacement Does and Doesn't Do

- Caps lifetime tax-free cash (LSA) and total tax-free death benefits (LSDBA).

- Does not cap pension growth or pension value.

- Does not directly apply to Taxable Income drawn from a pension — that is taxed at marginal rate.

- Does not change the annual allowance or MPAA rules.

- Does not change the normal minimum pension age framework.

Worked Example (Illustrative Only)

Consider a saver with a £1 million SIPP at age 60. Under the new framework, the saver can take 25% — £250,000 — as tax-free cash, well within the £268,275 LSA. The remaining £750,000 is moved into flexi-access drawdown and used for taxable income. If the saver later wants to take more tax-free cash from a second pension, only £18,275 of further tax-free cash is available before the LSA is exhausted; further withdrawals would be taxable income at the marginal rate.

If the saver dies before age 75 with £750,000 remaining in drawdown, the death benefits up to the remaining LSDBA (£1,073,100 minus the £250,000 already used = £823,100) can pass tax-free to beneficiaries. Death after 75 would mean beneficiaries pay income tax on the benefits at their marginal rate. This is an illustration only and not personal advice.

Implications for High-Earning Savers

For savers with pension benefits above £1 million, the new framework requires careful planning. The LSA caps tax-free cash at the same effective level as before, but the abolition of the LTA removes the punitive charges that previously applied to total benefits above £1,073,100. The shift creates an opportunity for high-earning savers to continue building pension benefits without the previous penalty — but the LSDBA still caps lifetime tax-free amounts.

Practical Effects

For most UK savers, the LSA and LSDBA framework is broadly equivalent in cash terms to the old LTA on the tax-free side. The differences become significant for savers with very large pensions or specific historic protections. Withdrawing more than 25% tax-free across all pensions is no longer possible above the LSA.

The new framework also affects death benefit planning. Members close to or above the LSDBA should review their estate planning, beneficiary nominations and the IHT treatment of pension death benefits.

What to Do Next

- Check whether you hold any LTA-era protection — fixed, individual or enhanced.

- Track total tax-free cash taken across all UK pensions during your lifetime.

- Review beneficiary nominations to support efficient death benefit planning.

- Speak with a regulated financial adviser if you have large pension benefits or unusual protection.

- Follow current GOV.UK guidance on any future changes to the IHT treatment of pensions.

Where to Get Help

MoneyHelper provides free guidance on UK pensions and the new lump sum allowance framework. HMRC publishes detailed guidance on the LSA, LSDBA and protections on GOV.UK. For personalised analysis of protections and high-value pensions, a regulated financial adviser is recommended.

LSA and LSDBA at a Glance (2026/27)

Headline figures for the UK lifetime allowance replacement framework in 2026/27.

Key Takeaways

- The lifetime allowance was abolished from 6 April 2024.

- Replacements are the LSA (£268,275) and LSDBA (£1,073,100).

- The LSA caps lifetime tax-free cash; the LSDBA caps wider tax-free amounts including death benefits.

- Existing protections from the LTA era may preserve higher allowances.

- Pension growth itself is not capped; only tax-free withdrawals are.

- Death benefit rules and IHT treatment may change in future.

- Specialist advice is essential for savers near or above the new allowances.

_06_08_2026_03_55_07_719582.jpg)

_06_08_2026_03_55_54_476359.jpg)

_06_08_2026_03_57_55_845266.jpg)

Please wait processing your request...

Please wait processing your request...