What Readers Need to Know

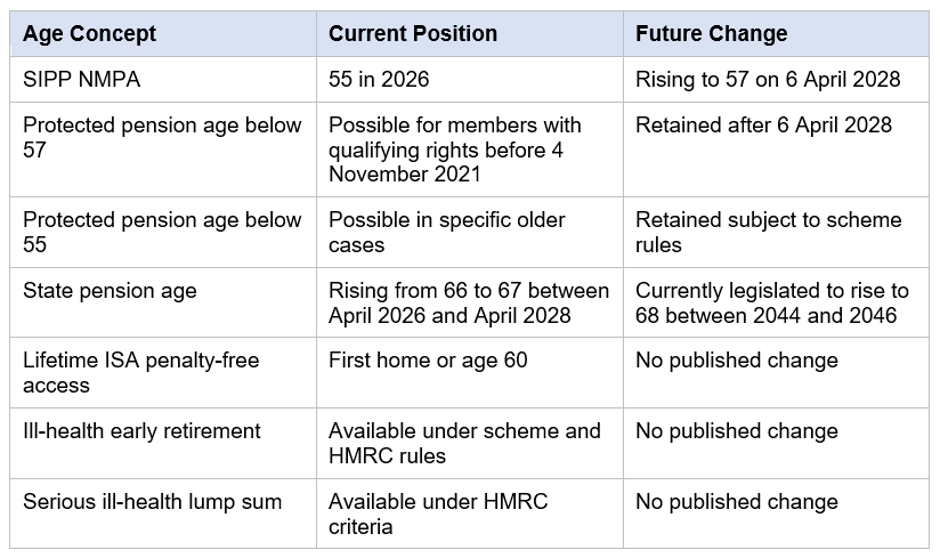

- The normal minimum pension age (NMPA) for SIPPs is 55 in 2026 and is rising to 57 from 6 April 2028.

- Protected pension ages may preserve earlier access for certain savers.

- Ill-health early access is possible under HMRC rules.

- The state pension age is a separate concept and is rising from 66 to 67 between April 2026 and April 2028.

- Accessing a pension before NMPA outside the rules is a serious matter and can trigger pension liberation tax charges and scam risk.

Introduction

Knowing when you can take money out of a SIPP is one of the most important pieces of UK pension planning. Take it too early and you risk losing money, paying penalties or being targeted by scam operators. Wait too long without planning and you may miss out on tax-efficient income strategies.

This guide explains the SIPP pension age rules that apply in the 2026/27 tax year, the upcoming changes that take effect from April 2028, and the relationship between SIPP access and the state pension. It is general information for UK readers and does not constitute personal advice.

What Is the Normal Minimum Pension Age (NMPA)?

The Normal Minimum Pension Age (NMPA) is the earliest age at which a UK private pension — including a SIPP — can normally be accessed under HMRC rules. The NMPA has been 55 since April 2010. From 6 April 2028, the NMPA increases to 57 for most savers.

The Move to 57 in 2028

Protected pension ages

Members of registered pension schemes who, before 4 November 2021, had an unqualified right under the scheme's rules to take their benefits before age 57 may retain a 'protected pension age'. Where the protection applies, the member can still access the pension before 57 after 6 April 2028.

Some savers also have older protected pension ages below 55 — for example, individuals from certain occupations such as professional sport with historic protected ages. These protections are scheme-specific and require careful checking. A regulated adviser or the scheme administrator can confirm whether protection applies.

What 'Accessing a SIPP' Means

Accessing a SIPP means crystallising some or all of the pension to take benefits. Typical Options include taking 25% tax-free cash and moving the rest to drawdown, taking smaller flexible lump sums (UFPLS), buying an Annuity, or a combination.

- Flexi-access drawdown — take 25% tax-free (subject to LSA) and draw Taxable Income flexibly.

- UFPLS — take ad-hoc lump sums, each 25% tax-free and 75% taxable.

- Annuity — exchange some or all of the pension for a guaranteed income for life or for a fixed term.

- Small pots — pots of £10,000 or less can sometimes be taken under specific rules without triggering the MPAA.

Tax-Free Cash and the LSA

Up to 25% of the value of the pension at crystallisation can normally be taken tax-free. The lifetime cap on tax-free cash is the Lump Sum Allowance (LSA) of £268,275, introduced from 6 April 2024 to replace the lifetime allowance. The Lump Sum and Death Benefit Allowance (LSDBA) of £1,073,100 sets the wider lifetime tax-free cap, including on death. Some savers have fixed or individual protection from earlier regimes preserving higher allowances.

Early Access Outside the NMPA

Pension liberation — what to avoid

Schemes that promise to 'unlock' a pension before the NMPA outside ill-health or protected pension age rules are almost always either non-compliant or fraudulent. HMRC treats early access as an unauthorised payment, with charges that can exceed 50% of the value. The FCA's ScamSmart resource is essential reading for any saver approached with such an offer.

Overseas Residence and SIPP Access

UK pension rules apply to UK-registered pension schemes wherever the saver lives. Living abroad does not change the NMPA or the tax-free cash rules, but it can affect how withdrawals are taxed under double taxation agreements. Many countries tax UK pension withdrawals at local rates, with or without a UK Withholding tax depending on the treaty. Returning to the UK after a period overseas restores the standard UK rules. International planning is highly specialist and should involve a regulated adviser with cross-border experience.

What Happens at NMPA?

Reaching the NMPA does not require the saver to take benefits immediately. Many UK savers delay drawing a SIPP for years after the NMPA, allowing the pension to keep growing. Others combine partial withdrawals with continued employment.

- Take nothing — leave the pension invested.

- Take 25% tax-free cash only — useful where extra cash is needed without taxable income.

- Take small taxable amounts — preserving more of the LSA for later.

- Move the whole pension into drawdown — providing ongoing flexible income.

- Buy an annuity — providing a guaranteed income for life or a fixed term.

- Combine approaches — for example, partial annuity plus drawdown.

The Money Purchase Annual Allowance (MPAA)

Once a saver flexibly accesses a DC pension — for example, by taking taxable income from drawdown or a UFPLS — the £10,000 MPAA replaces the standard annual allowance for DC contributions. Taking only the 25% tax-free cash without touching the drawdown income does not normally trigger the MPAA, but tax rules are technical and should be checked before acting.

SIPP Access and the State Pension

The state pension age is a separate concept and applies to the state pension only — not to a SIPP. The state pension age is rising from 66 to 67 between April 2026 and April 2028, and is currently legislated to rise to 68 between 2044 and 2046, subject to review. SIPP access and state pension entitlement can be combined or staggered to support a flexible retirement plan.

Working While Drawing a SIPP

Many UK savers do not stop working the day they first access a SIPP. Partial drawdown alongside continued employment or self-employment is common. The taxable element of any SIPP Withdrawal is added to other taxable income for the year, so withdrawing too much while still earning can push the saver into a higher tax band. Spreading withdrawals across tax years can keep the effective rate lower.

Continued contributions to a workplace pension may still be possible after partial SIPP access, but the MPAA caps DC contributions at £10,000 per year if taxable income has been drawn. Employer contributions count towards the MPAA limit, so savers planning to continue working should check the impact of any DC contributions, including auto-enrolment.

Defined Benefit Pensions and the NMPA

Where a saver also has a defined benefit (DB) pension, the access rules can differ from those of a SIPP. DB scheme rules govern the normal retirement age, with reductions for early payment and increases for delayed payment. The DB normal retirement age is not necessarily the same as the NMPA, and benefits taken before scheme normal retirement age typically reduce the income for life. Specialist advice is usually required for any decision involving DB pensions, including the choice between taking benefits in line with the DB scheme rules or transferring to a SIPP.

Practical Tips Before Accessing a SIPP

- Check your projected SIPP value, LSA usage and other pension income before deciding.

- Model the tax outcome of different withdrawal strategies over several years.

- Consider the MPAA — flexibly accessing one pension can limit future contributions.

- Plan how a SIPP fits alongside the state pension, workplace pensions and any defined benefit schemes.

- Speak to MoneyHelper or use Pension Wise for free guidance before taking advice.

- Engage a regulated financial adviser for personalised recommendations.

Pension Access Ages at a Glance

Key UK pension age numbers as at the 2026/27 tax year.

Key Takeaways

- The SIPP NMPA is 55 in 2026 and rises to 57 from 6 April 2028.

- Protected pension ages can preserve earlier access for some savers.

- Ill-health and serious-ill-health early access rules exist under strict criteria.

- Pension liberation schemes promising earlier access are almost always non-compliant or scams.

- Reaching NMPA does not force a saver to take benefits.

- The state pension age is a separate concept and is rising to 67 between 2026 and 2028.

- Free guidance is available via MoneyHelper and Pension Wise; personalised advice is essential.

_06_08_2026_03_55_07_719582.jpg)

_06_08_2026_03_55_54_476359.jpg)

_06_08_2026_03_57_55_845266.jpg)

Please wait processing your request...

Please wait processing your request...