What Readers Need to Know

- Full SIPPs can buy UK commercial property; platform SIPPs and workplace pensions typically cannot.

- Direct holdings of residential property are normally prohibited under the HMRC taxable property regime.

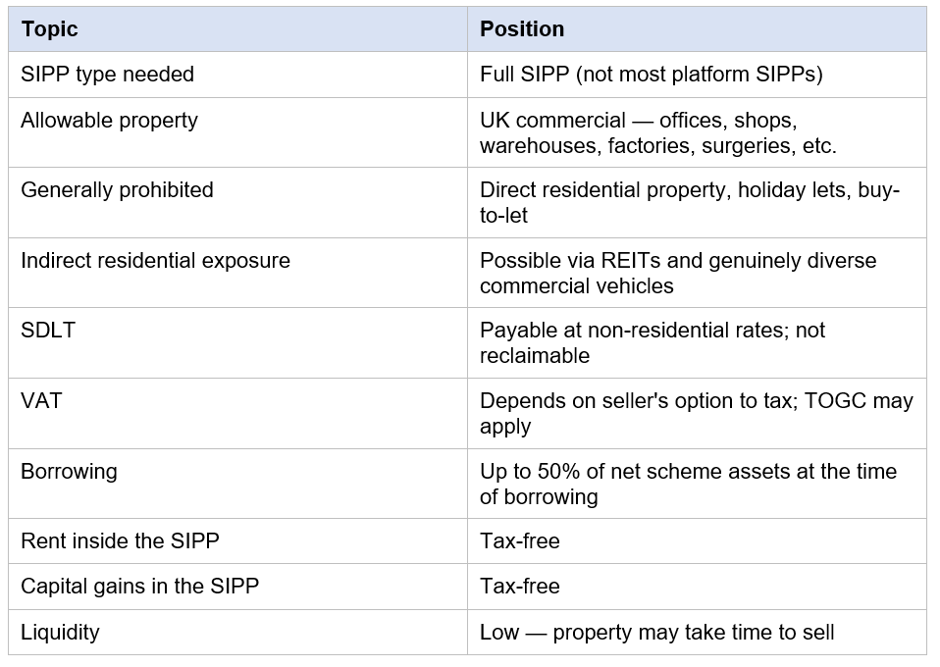

- SDLT applies at non-residential rates and cannot be reclaimed by the pension.

- Pensions can borrow up to 50% of their net asset value to fund a purchase.

- Property in a SIPP is Illiquid and benefits from specialist legal and tax advice.

Introduction

Buying Business premises through a pension has been one of the most enduring UK Retirement Planning ideas of the past two decades. Done well, the structure can support a working life of rent payments that build the pension, all within a tax-efficient wrapper. Done badly, the same structure can lock value into an illiquid asset, hit unexpected tax charges and create disputes between the pension and the connected business.

This article explains, in plain British English, whether you can buy property through a SIPP, what the rules look like for the 2026/27 tax year, and the practical issues to weigh. It is general information and not personal advice. Anyone considering buying property through a SIPP should engage a regulated financial adviser, a SIPP specialist administrator, a solicitor experienced in pension property and an RICS surveyor.

Which SIPPs Can Buy Property?

Not every SIPP can hold direct property. The market broadly splits into two types: 'platform' SIPPs that focus on funds, shares, ETFs and Investment trusts; and 'full' SIPPs that can also hold UK commercial property and certain specialist Assets. To buy property through a SIPP, the saver normally needs a full SIPP with a provider that accepts property purchases on its permitted assets list.

What Counts as Allowable Property?

HMRC pension rules distinguish between commercial and residential property. Commercial property — offices, shops, warehouses, factories, surgeries, hotels and similar non-residential premises — is generally allowable inside a SIPP. Residential property is generally prohibited as a direct holding, with narrow exceptions.

- Allowed: offices, shops, factories, warehouses, surgeries, restaurants, public houses (subject to manager accommodation rules), development land for commercial use.

- Allowed (indirectly): pooled vehicles such as REITs that meet HMRC's 'genuinely diverse commercial vehicle' tests.

- Generally not allowed: direct buy-to-let, holiday lets, student lets, second homes, and any building used or capable of being used as a dwelling.

- Possible exceptions: a flat above a shop occupied by an unconnected employee of the shop tenant; some specialist care homes, hotels and student accommodation under operator structures that meet specific HMRC criteria.

Why Residential Property Is Treated Differently

HMRC's taxable property regime applies a series of tax charges where a SIPP acquires residential property or other 'taxable property' such as personal chattels. The charges include an unauthorised payment charge of 40% of the value, a possible Surcharge of 15% above thresholds, a scheme sanction charge of 15% to 40% on the administrator and an annual benefit charge on any direct or indirect use of the asset. In combination, the charges typically destroy the value of the investment, which is why reputable SIPP operators refuse to acquire residential property directly.

How a SIPP Property Purchase Works

Step 3 — Purchase and Lease

The SIPP trustees buy the property in their names. The property is then leased — on commercial terms supported by an independent valuation — to the tenant. Where the tenant is the saver's own business or a connected party, the lease must be on arm's-length terms with proper documentation.

Tax Implications

Rent, gains and ongoing tax

Rent received by the SIPP is generally free from UK income tax inside the pension. Capital gains on sale are generally free from UK CGT inside the pension. Council tax, business rates and similar local taxes are not removed by the pension wrapper and remain payable in the normal way.

Connected Party Considerations

Where the tenant is the saver's own business or any connected party, the lease must reflect arm's-length commercial terms. Rent should be set by independent valuation, paid promptly and reviewed at agreed intervals. Side letters, informal arrangements and rent holidays are red flags that can attract HMRC attention. Solicitors should draft the lease as they would for any commercial landlord-tenant relationship.

Costs to Budget For

- SIPP operator's purchase fees, often time-cost with a four-figure minimum.

- Solicitor fees for purchase, lease drafting and (if borrowing) security documentation.

- RICS surveyor fees for valuation, structural surveys and rental advice.

- Lender arrangement, valuation and ongoing Facility fees.

- SDLT (or Welsh LTT, or Scottish LBTT).

- VAT, where applicable, and the cost of registering the SIPP for VAT.

- Annual SIPP property administration fees.

- Insurance, maintenance, repairs and statutory compliance costs.

Risks UK Savers Should Weigh

- Liquidity Risk: commercial property is difficult to sell quickly.

- Valuation risk: market values move; an over-rented property can mask falling capital values.

- Tenant risk: if a connected business cannot pay rent, both pension income and borrowing repayments suffer.

- Concentration risk: a single property can dominate a SIPP's value.

- Borrowing risk: Interest Rate rises and refinancing risk can affect the pension's Cash Flow.

- Compliance risk: connected-party transactions, rent reviews and lease renewals must be properly documented.

- Scam risk: high-pressure Marketing of unusual 'property pension' schemes has featured in FCA cases.

Pension Property and the Connected Business

Where the SIPP property is let to the saver's own company, the structure can support long-term continuity. Rent flows from the business to the pension rather than leaving the family as taxable profits or external rent. The business can budget rent as a known cost and the pension builds an income-producing asset.

The arrangement must be set up and operated at arm's length. Rent should be paid promptly and in full; any reductions or holidays must be on genuine commercial grounds and properly documented. If the business is sold, the SIPP can retain the property and continue to lease it to the new owner, or sell at Market Value. Either route should be planned in advance with specialist advice.

Practical Checklist Before Buying

- Confirm the SIPP type — only a full SIPP accepts direct property.

- Engage a regulated financial adviser to confirm a property purchase fits your retirement plan.

- Speak to a SIPP property specialist administrator to confirm the property is acceptable and to quote on fees.

- Instruct a solicitor experienced in pension property to handle title, lease and security.

- Instruct an RICS-qualified surveyor for purchase and rental valuations.

- Plan the SDLT, VAT and TOGC position before exchange.

- Confirm borrowing terms with a pension-property lender.

- Plan ongoing cash flow inside the SIPP to cover voids and maintenance.

- Plan an exit strategy in good time for retirement.

Joint Ownership and Multi-Pension Purchases

Where a single SIPP cannot fund a property alone, joint ownership across multiple SIPPs or SIPP plus SSAS is common. Each pension owns a defined share, the lease is granted by the joint owners, and rent is split in proportion. A deed of trust between the co-owners sets out decision-making, succession on a member's death and exit procedures. Joint ownership adds documentation and ongoing administration that should be planned with a specialist administrator.

Selling a SIPP Property

Property can be sold by the SIPP at any time, subject to market conditions and lease arrangements. Proceeds remain inside the pension. Where the buyer is a connected party, the sale must be at independently valued Market Price and supported by full documentation. Selling close to retirement may require careful timing to align with planned tax-free cash and ongoing drawdown, and may also need to be coordinated with any outstanding lender borrowing.

SIPP Property Purchase Snapshot

Headline rules and considerations for buying property through a SIPP in 2026/27.

Key Takeaways

- Full SIPPs can buy UK commercial property, but platform SIPPs and most workplace pensions cannot.

- Residential property is generally prohibited under the HMRC taxable property regime.

- Rent and capital gains inside the SIPP are normally tax-free.

- SDLT applies at non-residential rates and cannot be reclaimed.

- Pensions can borrow up to 50% of net assets to fund a purchase.

- Property is illiquid — exit planning matters as much as purchase planning.

- Specialist legal, tax and pension advice is essential.

_06_08_2026_03_55_07_719582.jpg)

_06_08_2026_03_55_54_476359.jpg)

_06_08_2026_03_57_55_845266.jpg)

Please wait processing your request...

Please wait processing your request...