What Readers Need to Know

- Full SIPPs and SSAS schemes can hold UK commercial property; ordinary workplace pensions and platform SIPPs typically cannot.

- Direct holdings of residential property are normally prohibited under the HMRC taxable property regime.

- Stamp Duty Land Tax applies at non-residential rates and is not exempt for pensions.

- Pensions can borrow up to 50% of net scheme Assets to fund a property purchase.

- Commercial property is Illiquid; specialist legal, tax and pension advice is essential before purchase.

Introduction

Owning your own Business premises through a pension is one of the more powerful Retirement Planning Options available to UK business owners. Rent paid by the business builds the pension. The property can pass through generations within the pension wrapper. And the structure benefits from the standard pension tax reliefs.

It is also one of the more complex pension transactions. UK rules on pension commercial property are detailed, the costs and timelines are significant, and breaches of HMRC rules can be expensive. This guide explains how the rules work in the 2026/27 tax year and where the practical risks sit. It is general information only — anyone considering buying property through a pension should engage a regulated financial adviser, pension specialist administrator, Accountant and solicitor.

Which UK Pensions Can Hold Commercial Property?

Only certain UK pension structures can hold direct UK commercial property. The two main routes are a full Self-Invested Personal Pension (SIPP) and a Small Self-Administered Scheme (SSAS). Platform SIPPs that focus on funds and shares typically do not accept direct property. Workplace pensions are usually invested in pooled funds and cannot hold individual commercial properties.

What Counts as Commercial Property?

HMRC distinguishes between residential and non-residential property. Residential property is defined broadly as a building used or capable of being used as a dwelling, plus adjoining land. Anything that meets that definition is generally prohibited as a direct pension holding under the taxable property regime, with narrow exceptions for cases such as a flat above a shop occupied by an unconnected employee.

Permitted commercial property typically includes offices, shops, warehouses, industrial units, surgeries, hotels, restaurants, pubs (without manager accommodation), development land for commercial use and certain mixed-use buildings. Care homes, prisons and student accommodation operated by specialist providers may meet specific exceptions and require legal review.

How a Pension Property Purchase Works

Step 3 — Purchase and Lease

The pension purchases the property in the name of the SIPP trustees or SSAS trustees. The property is then leased — at a commercial rent on commercial terms — to the tenant. If the tenant is a connected business, an independent valuation supports both the purchase price and the rent.

Tax Implications

Rent and capital gains

Rent received by the pension is generally not subject to UK income tax inside the pension. Capital gains realised when the property is later sold are generally not subject to UK Capital Gains Tax inside the pension. The pension benefits from gross compounding of rent and gains.

Connected Party Rules

Where the tenant of a pension-owned property is connected to the member — a spouse, civil partner, certain relatives, or a company controlled by them — HMRC pays close attention to the terms. Independent valuations of both purchase price and market rent are essential. Rent should be paid promptly; arrears can trigger tax issues. Legal documentation (the lease, rent reviews and any side letters) must reflect arm's-length commercial terms.

Costs to Budget For

- Purchase fees from the SIPP or SSAS administrator, typically time-cost with a minimum charge.

- Legal fees for purchase, lease drafting and any borrowing security.

- Surveyor and independent valuation fees.

- Lender arrangement, valuation and ongoing Facility fees.

- SDLT at non-residential rates, plus equivalents in Scotland and Wales.

- VAT (where applicable) and the cost of any VAT registration.

- Annual property administration fees from the pension administrator.

- Building insurance, maintenance, repairs and statutory compliance.

Borrowing in More Detail

The 50% borrowing limit is calculated against the net Market Value of the scheme's assets at the time the borrowing is taken. The lender will register a first charge over the property. Loan repayments come from rent collected, and any shortfall must be funded from pension contributions or other scheme assets. The pension's own Cash Flow and Liquidity must be planned carefully to handle voids, rent reviews and unexpected costs.

Risks to Weigh Up

- Liquidity Risk: commercial property is hard to sell quickly. In a downturn, selling at full value may not be possible.

- Valuation risk: the market value of commercial property can move sharply and is determined by independent valuation, not by the pension's records.

- Tenant risk: if a connected tenant struggles to pay rent, the pension's income and ability to service borrowing can both be affected.

- Concentration risk: a single property can dominate a pension portfolio, reducing Diversification.

- Compliance risk: connected-party transactions and rent reviews must be properly documented; HMRC charges follow breaches.

- Borrowing risk: Interest Rate rises, refinancing risk and lender covenants can all affect the pension.

Joint Ownership and Multiple Pensions

Where a single property is too large for one pension to fund alone, joint ownership between multiple SIPPs and SSAS schemes is common. Each pension owns a defined share, and rent is split in proportion to ownership. The lease is granted by the joint owners, and any borrowing is structured to reflect each scheme's contribution.

Joint ownership adds documentation and ongoing administrative complexity. Co-owners need a clear deed of trust setting out decision-making, succession on a member's death and exit procedures. Specialist legal advice is essential, particularly where the owners are connected to the tenant business.

Practical Steps Before Buying

- Speak to a regulated financial adviser to confirm a pension property purchase fits your wider retirement plan.

- Engage an SSAS or full SIPP administrator to confirm the property is acceptable and to quote on fees.

- Instruct a solicitor experienced in pension property to review the title, lease and security documentation.

- Instruct an RICS-qualified surveyor for the purchase valuation and any rental valuation.

- Confirm VAT treatment and any TOGC position with the seller before exchange.

- Confirm SDLT, Welsh LTT or Scottish LBTT and have funds in place to pay.

- Plan for liquidity — voids, rent reviews and unexpected costs all need cash inside the pension.

- Plan an exit strategy in good time for retirement and intergenerational planning.

What Happens at Retirement?

The pension property can normally remain in the pension into and through retirement. Members can take tax-free cash and income from the pension while the property continues to generate rent. On the member's death, the property forms part of the pension's death benefits, which can pass to beneficiaries under the pension rules. Specialist advice is essential to plan around the LSA, LSDBA and beneficiary nomination rules.

Taking tax-free cash where the pension's main asset is illiquid commercial property requires careful planning. The pension needs enough cash — built from rent, contributions or sale of other investments — to pay the lump sum. Some members plan ahead by building a cash buffer over years, while others sell the property close to retirement. Both approaches have advantages and trade-offs that benefit from professional input well before the planned retirement date.

Intergenerational planning is another common consideration. A pension-owned property can pass to nominated beneficiaries through the scheme, supporting longer-term family Wealth planning. Trustees should keep beneficiary nominations up to date and aligned with the member's wider estate plans, and should regularly review valuations to ensure the property's value is correctly reflected in pension and tax planning.

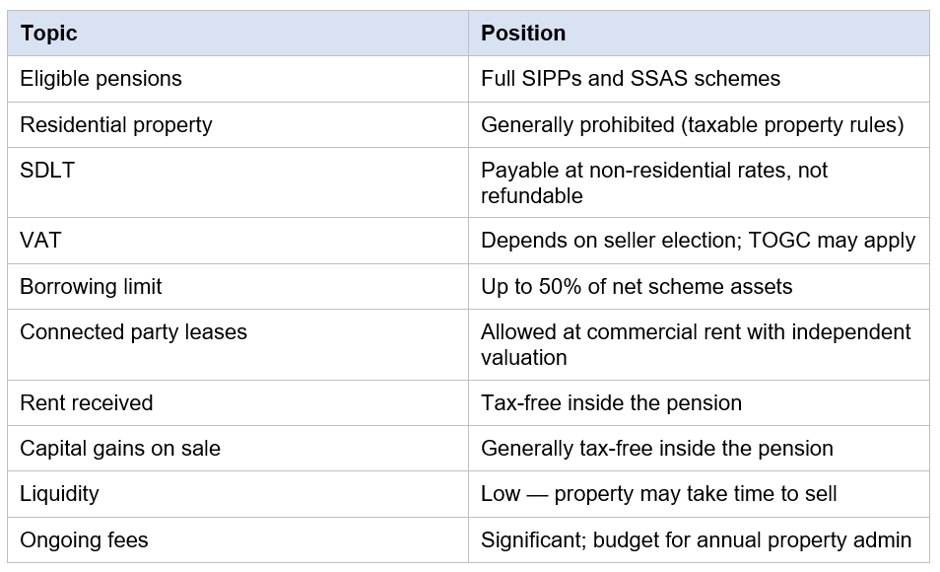

Commercial Property in UK Pensions at a Glance

Headline rules and risks for direct commercial property holdings inside a UK pension in 2026/27.

Key Takeaways

- Only full SIPPs and SSAS schemes can hold direct UK commercial property.

- Residential property is generally prohibited under the HMRC taxable property regime.

- SDLT applies at non-residential rates and cannot be reclaimed by the pension.

- VAT treatment depends on the seller's tax election and TOGC rules.

- Pensions can borrow up to 50% of net scheme assets to fund the purchase.

- Rent from a connected business must be at commercial market rates with proper documentation.

- Commercial property is illiquid — specialist legal, tax and pension advice is essential.

_06_08_2026_03_55_07_719582.jpg)

_06_08_2026_03_55_54_476359.jpg)

_06_08_2026_03_57_55_845266.jpg)

Please wait processing your request...

Please wait processing your request...