_11_18_2025_15_27_51_117210.png)

Index Update: The FTSE 100 index, a key benchmark index for the London stock exchange, was trading down around 1.22% on 18 November 2025.

Macro Update: The Bank of England is preparing to ease certain ring-fencing rules for major lenders but will resist broader reforms sought by banks, aiming to preserve core post-crisis protections even as the government pushes regulatory simplification. Meanwhile, Imperial Brands delivered slightly better-than-expected annual profits and reaffirmed its outlook for steady growth driven by higher tobacco prices and expanding smoke-free products. In UK bond markets, gilts remain attractive but political uncertainty and budget risks are creating a volatility premium, with some investors expecting further tax rises next year and long-term gilt yields potentially approaching 6% amid growing concerns over fiscal stability.

Top Market Movers: Among top gainers on FTSE 100 index, ICG PLC (LSE: ICG) witnessed a rise of 5.56% followed by Imperial Brands PLC (LSE: IMB) which gained around 2.38%.

Commodity Update: The yen weakened to a nine-month low in early Asian trade on Tuesday as fading expectations of a Fed rate cut next month boosted the dollar. Precious metals retreated, with gold down 1.32% to USD 4,020.40, silver slipping 2% to USD 49.68, and copper easing 0.43% to USD 10,733.10. Brent crude dipped 0.40% to USD 63.92 as supply concerns eased after Russian export loadings resumed.

Our Stance: Global markets reflected a broad risk-off tone as the dollar briefly hit a nine-month high against the yen on worries over Japan’s fiscal outlook, while investors awaited key U.S. data after the shutdown. Corporates signalled softer labour demand, with Fed Governor Waller noting rising layoff discussions as firms prepare for weaker demand and potential AI-driven efficiency gains—adding pressure for another rate cut in December. In equities, Apple saw a 37% surge in China iPhone sales, but tech-heavy markets slipped, European indices hit multi-month lows, and U.S. benchmarks broke below their 50-day moving averages, highlighting fragile sentiment ahead of Nvidia earnings and delayed U.S. jobs data. Bitcoin fell below $90,000 amid waning risk appetite, while oil prices eased as Russian export loadings resumed despite ongoing sanctions concerns.

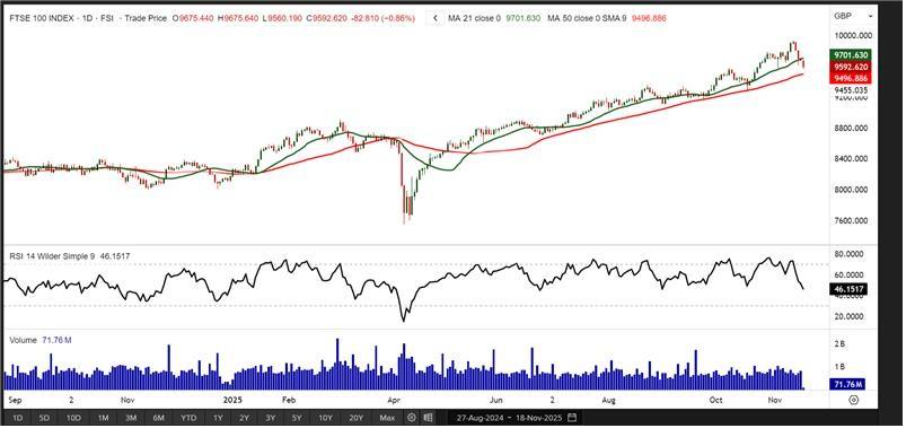

FTSE 100

The FTSE 100 slipped 82.83 points to 9,592.62 but continues to hold firmly above the key support zone near 9,200, keeping the broader structure intact. The 21-day SMA at 9,701.63 sits above the CMP, reflecting a bearish undertone, while the 50-day SMA at 9,496.88 signals overall stability, pointing to the likelihood of near-term consolidation. The RSI remains elevated but within bearish territory, indicating a mildly negative bias. Immediate support lies near 8,950, with resistance at 10,000 and 10,120.

Source - EODHD/Others

Please wait processing your request...

Please wait processing your request...