A Commodity Supercycle refers to a prolonged period — often lasting 10 to 20 years or more — during which demand for raw materials rises faster than supply, driving sustained increases in commodity prices. Unlike normal commodity cycles, which are typically driven by short-term economic fluctuations, supercycles are underpinned by structural shifts in the global economy.

As we move through the mid-2020s and into 2026, investors are once again debating whether the world is entering a new Commodity Supercycle — and what that could mean for LSE-listed resource stocks, which remain some of the most commodity-leveraged equities globally.

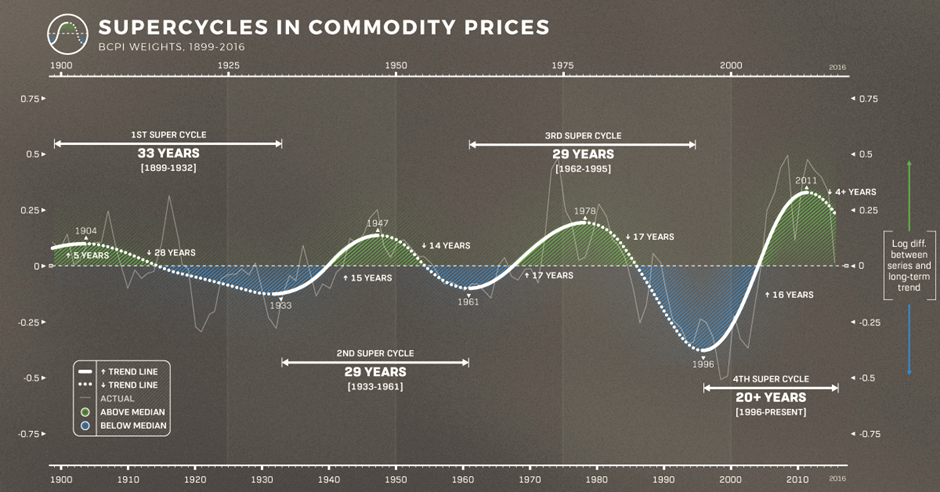

A Brief History of Commodity Supercycles

Historically, commodity supercycles have coincided with periods of major industrial transformation.

- Post-World War II industrialisation (1940s–1960s): Rapid rebuilding and manufacturing growth in the United States and Europe drove enormous demand for steel, copper, oil, and coal.

- China’s urbanisation boom (early 2000s): China’s entry into the World Trade Organization and massive infrastructure investment triggered a multi-year surge in iron ore, coal, copper, and energy prices.

Source: Bank of Canada Price Index (BCPI); Analysis by Kalkine Group

In each case, the key ingredients were the same: new sources of demand, limited short-term supply elasticity, and years of elevated capital investment across the resources sector.

Why a New Supercycle Is Being Discussed in 2026?

The Current Supercycle thesis differs from past examples. Rather than being driven by a single country’s industrialisation, it is shaped by multiple global forces acting simultaneously:

- Energy Transition and Electrification

The shift toward renewable energy, electric vehicles (EVs), grid-scale storage, and electrification of transport and industry is dramatically increasing demand for battery and conductive metals.

- Decarbonisation Commitments

Governments and corporations are committing trillions of dollars to emissions reduction targets, which require vast quantities of metals such as copper, lithium, nickel, and rare earths.

- Supply Constraints

Years of underinvestment following the last commodity downturn have left supply pipelines thin. New mines are capital-intensive, slow to permit, and increasingly constrained by ESG and geopolitical considerations.

- Geopolitical Fragmentation and Resource Security

Countries are prioritising domestic and allied supply chains, leading to duplication of infrastructure and higher long-term demand for strategic commodities.

Together, these forces have created the conditions for persistent commodity tightness rather than short-lived price spikes.

Why This Matters for LSE Commodity Stocks?

London’s equity market is uniquely exposed to commodities. The LSE hosts a large number of globally significant miners, ranging from diversified giants to emerging developers.

Why LSE resource stocks stand out?

Source: Kalkine Group

Key Commodity Groups and LSE Beneficiaries

- Battery and Energy Transition Metals

Notable LSE players, and annual % returns (at the time of writing on 12 Jan 2026)

- European Metals Holdings (LSE:EMH) — Trading at GBX 18.50, up 124.24% in the past one year.

- Savannah Resources (LSE:SAV) — Priced at GBX 4.80, up 14.29% in the past one year.

- Glencore plc (LSE:GLEN) — Closed at GBX 465.50, up 27.90% in the past one year.

- Antofagasta plc (LSE:ANTO) — Close price of GBX 3,446, up 103.78% in the past one year.

Copper, in particular, is often described as the “backbone of the energy transition”, given its essential role in power grids, EVs, and renewable infrastructure.

- Bulk Commodities — Still Relevant

While bulk commodities may not lead the next supercycle, they remain essential to global development.

Drivers:

Infrastructure investment, emerging market urbanisation, disciplined supply growth.

Key commodities:

- Iron ore

- Metallurgical coal

Major LSE producers, and annual returns as on 12th Jan 2026 (at the time of writing):

- Rio Tinto (LSE:RIO) - Priced at GBX 6,047.

- Glencore plc (LSE:GLEN) - Priced at GBX 465.50, up 27.90% in the past one year

- Ecora Resources plc (LSE:ECOR) - Priced at GBX 124.80, up 102.93% in the past one year.

Although demand growth may be slower than in the 2000s, supply constraints and capital discipline could support structurally higher prices compared to historical averages.

- Energy: Oil, Gas, and Uranium

Despite the push toward renewables, traditional energy sources remain critical — particularly in a world increasingly focused on energy security.

Drivers:

Underinvestment, geopolitical risk, nuclear power revival.

LSE exposure, and yearly returns as on 12th Jan 2026:

- Shell plc (LSE:SHEL) — Priced at GBX 2,632, down 1.16% in the past one year.

- BP plc (LSE:BP.) — Priced at GBX 425, down 1.44% in the past one year.

- Yellow Cake plc (LSE:YCA) —Priced at GBX 615, up 19.77% in the past one year.

Uranium stands out as a commodity increasingly viewed as structural rather than cyclical, supported by renewed nuclear investment across Europe, Asia, and North America.

- Gold and Precious Metals

Gold plays a different role in a supercycle environment.

Drivers:

Inflation hedging, central bank buying, geopolitical uncertainty.

LSE-listed names and % yearly returns as on 12th Jan 2026:

- Fresnillo plc (LSE:FRES) - Priced at GBX 3,722, up 477.50% in the past one year.

- Endeavour Mining plc (LSE:EDV) - Priced at GBX 4,021.20, up 170.79% in the past one year.

- Hochschild Mining plc (LSE:HOC) - Priced at GBX 554.50, up 153.20% in the past one year.

Gold often performs best late in the economic cycle or during periods of financial stress, providing portfolio diversification when other commodities become volatile.

Who Benefits Most During a Supercycle?

Not all resource companies benefit equally. Historically, the strongest performers tend to share common characteristics:

- Low-cost production profiles

- Long-life, high-quality assets

- Strong balance sheets

- Operational scale and pricing power

Large-cap miners typically provide stability and income, while smaller producers and developers can deliver outsized returns — albeit with higher execution and funding risk.

Risks Investors Should Watch

Even in a Commodity Supercycle, risks persist. A sharper slowdown in China could weaken demand, while technological substitution may alter long-term commodity usage. Government intervention, rising royalties, and cost inflation can pressure margins. ESG and permitting delays may disrupt project timelines, making careful stock selection essential.

In conclusion if a commodity supercycle continues to unfold through 2026 and beyond:

- LSE resource stocks are exceptionally well positioned

- Energy transition metals — especially copper and lithium — are likely leaders

- Investors should prioritise quality, cost discipline, and asset longevity

For long-term investors, commodities may once again represent not just a cyclical trade, but a strategic allocation in a rapidly changing global economy.

Please wait processing your request...

Please wait processing your request...