Key Takeaways

- FTSE 100 hovers near the 10,000-point milestone, supported by upbeat corporate updates and decisive demand for UK government bonds.

- Utilities, pharmaceuticals, and telecoms lead gains; housebuilders and consumer stocks remain soft.

- Record £69 billion gilt auction signals continued investor confidence in UK debt despite political uncertainty.

- Labour data shows a modest slowdown, raising expectations for a Bank of England rate cut in December.

- Investors monitor global sentiment as SoftBank’s Nvidia exit and weaker US tech trade impact risk appetite.

Market Overview

The UK equity market opened on a steady note on 12 November 2025, with the FTSE 100 index inching closer to the 10,000-point level — a symbolic milestone reflecting optimism over global growth trends and corporate stability.

The broader FTSE 250 also gained modestly, tracking a positive tone across European peers, where investors welcomed easing inflation expectations and strong corporate balance sheets.

Source: EODHD/Others, Date:12 November 2025

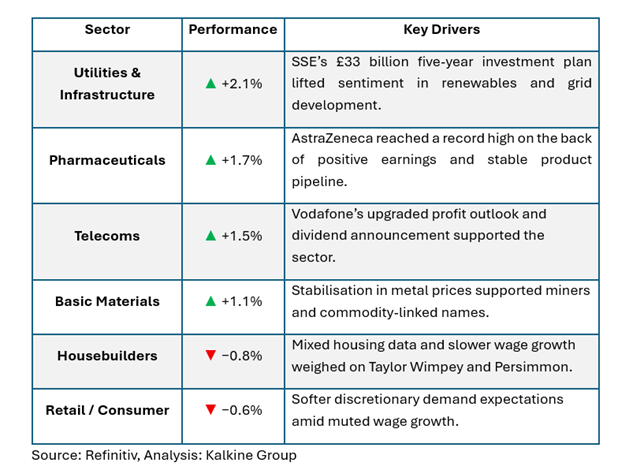

Sector Snapshot

Macro Highlights

- Labour and Monetary Policy

Recent data showed unemployment rising to around 5%, its highest in four years. While this suggests cooling in the job market, it also reinforced expectations of a possible BoE rate cut in December.

The pound eased slightly on the report, while bond yields declined as markets priced in a softer monetary stance.

- Government Debt and Fiscal Sentiment

A record-breaking £69 billion in orders for the UK’s 2038 inflation-linked gilts underscored great investor demand for sovereign debt.

Despite occasional political and fiscal debates, this level of interest highlights confidence in the UK’s debt framework.

Global Context

Globally, markets responded to SoftBank Group’s sale of its Nvidia stake, which triggered mild profit-taking in tech stocks worldwide.

European shares, however, held firm — aided by resilient banking and industrial sectors — while UK equities saw rotation toward defensive and dividend-oriented names.

Stocks in Focus

- SSE PLC (LSE: SSE) – Shares jumped over 11% after unveiling a £33 billion renewable investment roadmap, boosting confidence in the UK’s clean-energy and infrastructure ambitions.

- Vodafone Group PLC (LSE: VOD) – Gained around 5.5% following an improved profit forecast and dividend confirmation, reflecting investor preference for stable, high-yield telecom names.

- AstraZeneca PLC (LSE: AZN) – Advanced 1.7%, touching a record high after decisive quarterly earnings underscored consistent demand across oncology and cardiovascular drugs.

- EasyJet plc (LSE: EZJ) – Featured among the most-traded UK shares with nearly 80% buy interest, as travel demand indicators pointed to steady passenger recovery.

- Empyrean Energy PLC (LSE: EME) – Attracted sharp retail activity amid renewed interest in oil and gas exploration plays, with investors tracking energy price resilience.

- Taylor Wimpey PLC (LSE: TW) – Declined roughly 4% as housing data softened, signalling slower buyer activity and pressure on sector margins.

- BT Group plc (LSE: BT.A) – Moved higher after reports of ongoing strategic partnerships to expand fibre rollout and strengthen cash generation.

- Barclays PLC (LSE: BARC) – Traded actively following analyst commentary suggesting ample capital buffers and scope for dividend maintenance into 2026.

- Glencore PLC (LSE: GLEN) – Edged up on stabilising metal prices, with traders highlighting potential volume recovery in copper and zinc.

- Unilever PLC (LSE: ULVR) – Saw steady inflows as consumer-staple stocks drew attention amid softer retail sentiment in discretionary spending.

Market Themes to Watch

- Sector Rotation: Defensive names continue to attract flows, while cyclicals await clarity on rate decisions.

- Inflation vs. Growth: Data remains finely balanced — easing inflation supports equities, but weaker jobs data raises concerns about spending.

- FTSE 100 Momentum: A potential breakout above the 10,000-mark could attract algorithmic and institutional buying.

Summary

UK markets remain steady with mixed but constructive sentiment. Gains in utilities, healthcare, and telecoms reflect confidence in long-term stability, while cyclical sectors like housing and retail await robust demand cues.

Global developments — especially in technology and interest-rate expectations — continue to shape near-term trading patterns.

Please wait processing your request...

Please wait processing your request...