Aston Martin Lagonda (LSE: AML) has spent much of 2025 in the "slow lane," but the tides turned on December 22, 2025, as the FTSE 250 stock climbed ~3% in a single session. After a year defined by profit warnings, supply chain snarls, and leadership transitions, investors are finally seeing a glimmer of the "Ultra-Luxury" turnaround promised by Executive Chairman Lawrence Stroll.

The "Santa Rally" Drivers: Why AML Jumped 3%

While the broader market enjoyed a year-end lift, Aston Martin’s specific 3% gain was fueled by a convergence of operational milestones and technical factors:

Source: Kalkine Group

- Valhalla Deliveries Commence: The primary catalyst is the long-awaited start of deliveries for the Valhalla—the brand’s first hybrid supercar. With 150 units slated for Q4 2025, the market is pricing in the immediate cash-flow injection these £1M+ vehicles provide.

- Liquidity Boost: Following the strategic sale of shares in its F1 team (AMR GP) for roughly £108 million and a fresh cash infusion from the Yew Tree Consortium, total liquidity has stabilized at approximately £250 million, easing immediate bankruptcy fears.

- Oversold Rebound: After a brutal 41% drop year-to-date, the stock entered "oversold" territory on the RSI (Relative Strength Index). Technical buyers stepped in, viewing the 60p–65p range as a potential floor.

- Operational Streamlining: Investors reacted positively to the ongoing 10% reduction in SG&A expenses and a "comprehensive review" of future Capex, signaling a shift from reckless expansion to disciplined profitability.

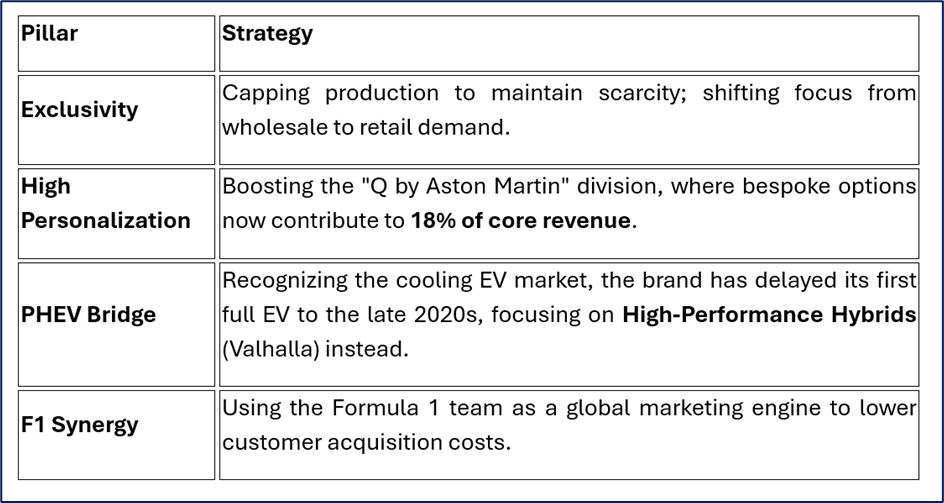

The Latest Business Model: "Ultra-Luxury" 2.0

Under new CEO Adrian Hallmark, Aston Martin is moving away from being a "volume" manufacturer to a true Ferrari rival.

Source: Company Data

Operational & Financial Snapshot (Q4 2025 Update)

The recent 3% bump is a reaction to a "less bad" outlook for 2026.

- Wholesale Volume: Revised down to a mid-to-high single-digit decline for FY2025 (approx. 5,500–5,700 units).

- Average Selling Price (ASP): Core ASP has increased by 4–7%, proving that even if they sell fewer cars, they are selling more expensive ones (like the new V12 Vanquish).

- Profitability Gap: Adjusted EBIT for 2025 is still expected to be a loss (below -£110m), but management has officially guided for materially improved free cash flow in 2026.

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- Unrivaled Brand Equity: Iconic status reinforced by James Bond and F1.

- Strong Order Book: Core vehicle orders remain stable, extending up to five months out.

- Design Excellence: The new Vantage S and DBX707 continue to receive "best-in-class" reviews.

Weaknesses

- Debt Burden: Net debt remains a heavy anchor at nearly £1.4 billion.

- Production Delays: Persistent "timing issues" with homologation and engineering completion for new models.

- Negative ROE: Currently destroying shareholder value with a return on equity of ~-36%.

Opportunities

- Hybrid Expansion: High demand for the Valhalla could act as a "halo effect" for the rest of the lineup.

- US-UK Trade Clarity: Recent trade agreements help mitigate the fear of sudden 10% tariffs.

- Ultra-HNWI Growth: The global increase in billionaires continues to expand the target demographic.

Threats

- China Slowdown: Weak macroeconomic demand in Greater China—a critical luxury market.

- Supply Chain Fragility: Vulnerability to niche supplier bankruptcies or cyber-attacks (as seen recently in the UK).

- EV Pivot: Competitors like Ferrari and Porsche are further ahead in the race to high-performance electrification.

The Risk "Roadblocks"

Investing in AML isn't for the faint of heart. The primary risks include interest rate sensitivity (due to high debt), geopolitical tariffs (specifically the US quota system), and execution risk. If the remaining Valhalla units aren't delivered on time in 2026, the current rally could stall as quickly as it started.

Conclusion

The 3% jump on December 22 is a "vote of confidence" in the Hallmark-Stroll turnaround plan. By slashing costs and finally moving the Valhalla from the factory to the driveway, Aston Martin is trying to prove it can be a business, not just a brand. 2026 will be the "make-or-break" year: either the company achieves the promised positive cash flow, or it risks becoming another cautionary tale in British automotive history.

Source: Trading View, 22 December 2025

Please wait processing your request...

Please wait processing your request...