Defense Sector Wealth Compounders: 2026 Outlook

Current geopolitical instability has transitioned the defense sector from a cyclical industrial play into a structural secular growth theme for 2026. The "Peace Dividend" is officially over, replaced by a global rearmament supercycle. With the UK government committing to a path of 2.5% GDP defense spending and NATO members universally hiking budgets, the floor for earnings in this sector has risen significantly.

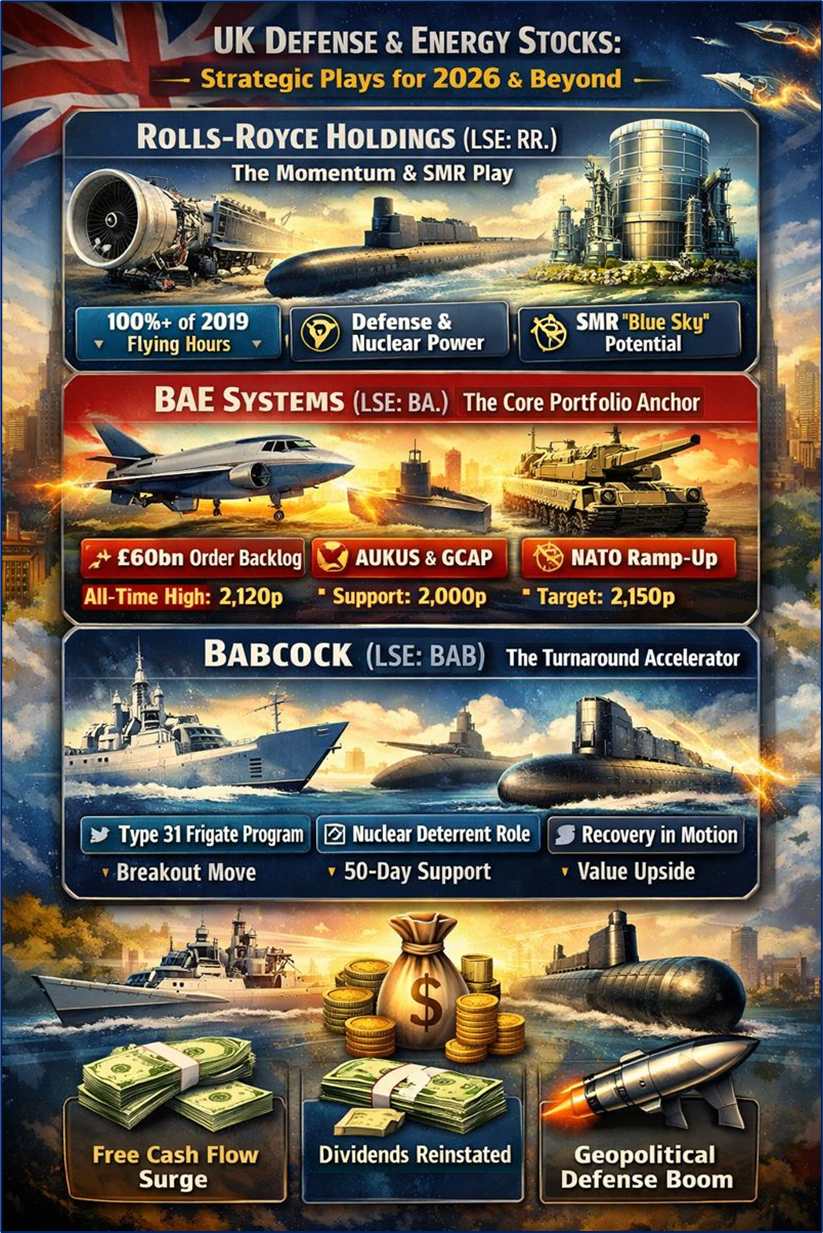

The following analysis identifies three FTSE-listed defense stocks with distinct wealth-compounding profiles: the momentum giant, the steady compounder, and the turnaround accelerator.

Source: Kalkine Group

Rolls-Royce Holdings (LSE: RR.) – The Momentum & SMR Play

- Key Reasons & Drivers: Rolls-Royce has evolved beyond a recovery story into a high-margin industrial powerhouse under CEO Tufan Erginbilgic. The primary driver for 2026 is the dual-engine growth of civil aerospace recovery (returning to 100%+ of 2019 flying hours) and the burgeoning Defense division, which powers the nuclear submarine fleet. The "blue sky" driver is the Small Modular Reactor (SMR) division, which is positioned to capture a massive share of the global energy transition market, potentially unlocking a valuation re-rating similar to a tech stock rather than a legacy industrial.

- Current Technical Analysis: Technically, the stock remains in a parabolic primary uptrend, trading significantly above its 200-day moving average (~1,007p). Price action recently hit a record high of 1,305p earlier this week and is currently consolidating around 1,285p. Immediate support is now seen at the breakout level of 1,190p-1,200p, while upside resistance is testing the new all-time high of 1,305p, with bulls eyeing the psychological 1,500p level next.

- Valuation, Financials & Analyst Opinion: Despite its rally, analysts argue the stock is not expensive relative to its improved free cash flow (FCF) guidance. The company aims for £3.1bn FCF by 2027, putting it on a forward FCF yield that rivals top US peers. Recent upgrades from UBS and Jefferies highlight the "conservative" nature of management guidance. The business model has shifted to value over volume, aggressively pricing long-term service agreements (LTSA). Dividends have been reinstated, signaling balance sheet health, though the yield remains modest as capital is prioritized for growth.

- Risks & Outlook: The outlook is heavily bullish, but risks center on supply chain fragility, particularly in titanium and specialized alloys. Any delay in the SMR regulatory approval process could dampen sentiment. However, as the sole provider of nuclear power plants for the Royal Navy's submarines, the competitive moat is virtually impenetrable.

BAE Systems (LSE: BA.) – The Core Portfolio Anchor

- Key Reasons & Drivers: BAE Systems is the "sovereign default" for UK defense exposure. The key driver for 2026 is the sheer visibility of its order backlog, which stands at record levels (over £60bn). The AUKUS submarine pact (UK, US, Australia) and the Global Combat Air Programme (GCAP) provide multi-decade revenue streams that are insulated from short-term economic dips. BAE is also a major beneficiary of ammunition restocking, with its Land UK and Hägglunds divisions running at maximum capacity to replenish NATO stockpiles.

- Current Technical Analysis: BAE Systems remains a standout performer, currently trading at 2,088p, just shy of its fresh all-time high of 2,120p set on Jan 12. The stock is currently digesting a ~70% rally over the last year. Immediate support is found at the psychological 2,000p level (and technically at 1,830p), while the next major breakout target is in blue-sky territory above 2,150p. Momentum indicators like the RSI are elevated (overbought), suggesting a brief pause or pullback may occur before the next leg higher.

- Valuation, Financials & Analyst Opinion: Trading at a forward P/E of roughly 16-18x, BAE trades at a discount to US defense peers like Lockheed Martin or Northrop Grumman (often 20x+), offering a clear "valuation gap" arbitrage. JP Morgan and Goldman Sachs have maintained "Overweight" ratings, citing the stock as a key beneficiary of the 2.5% GDP spending pledge. The company recently increased its dividend and launched further share buybacks, reinforcing its commitment to shareholder returns.

- Risks & Outlook: The primary risk is government budget constraints or a sudden de-escalation in geopolitical tensions leading to order deferrals. However, the operational outlook is robust, with margins expected to expand as supply chain inflation eases. The acquisition of Ball Aerospace has successfully diversified revenue into the high-growth US space and intelligence sectors.

Babcock International (LSE: BAB) – The Turnaround Accelerator

- Key Reasons & Drivers: Babcock represents the highest "beta" or potential percentage gainer among the three. After a successful restructuring, the company has pivoted from a distressed asset to a high-quality defense contractor. The key drivers are the Type 31 frigate program and its critical role in sustaining the UK's nuclear deterrent (Vanguard and Astute class submarines). Unlike BAE, Babcock is earlier in its recovery curve, meaning margin expansion (from ~6% to ~8%+) acts as a double-lever for share price growth.

- Current Technical Analysis: The technicals show a "breakout" from a long-term base. The stock has recently cleared multi-year resistance levels, attracting volume from breakout traders. Relative strength against the FTSE 250 is high. The chart shows a series of higher highs and higher lows, confirming a trend reversal is fully established. Pullbacks to the 50-day moving average have been aggressively bought, signaling strong institutional support.

- Valuation, Financials & Analyst Opinion: Babcock trades at a significant discount to BAE and Rolls-Royce, often in the 10-12x P/E range. This valuation disparity is closing as trust in management is restored. Citi and Peel Hunt have issued upgrades, noting that the "risk premium" attached to the stock is diminishing. The business model now focuses on cash generation and contract profitability rather than revenue chasing. Dividends have been restored, marking the final box ticked in its recovery roadmap.

- Risks & Outlook Turnarounds are inherently riskier; execution errors on complex contracts (like the Type 31 dispute, which has largely been settled) can be costly. However, the "super-cycle" in naval shipbuilding and nuclear infrastructure support provides a massive tailwind that mitigates individual contract risks.

Smart Money & Institutional Sentiment

- Global Fund Flows Data from major custodians like BlackRock and State Street indicates a structural rotation out of consumer discretionary and into "Security & Defense" thematic baskets. Hedge funds have moved from being net short defense (ESG concerns) to net long, driven by the pragmatic realization that defense is a prerequisite for ESG.

- Analyst Consensus The consensus from "Smart Money" is that UK defense stocks are chronically undervalued compared to US peers. US defense stocks trade at premium multiples due to the "Trump Trade" or US budget expectations, while UK stocks offer similar growth profiles at a 30-40% discount. Investment banks are advising clients to overweight European defense as a hedge against geopolitical volatility in 2026.

Please wait processing your request...

Please wait processing your request...