As the UK equity market enters 2026, the FTSE 250 is emerging from a period of relative underperformance compared to its blue-chip sibling, the FTSE 100. Strategists at major houses like UBS and Barclays suggest that mid-caps are now a "coiled spring," potentially benefiting from a stabilizing domestic economy and a shift toward growth-oriented valuations.

Source: Kalkine Group

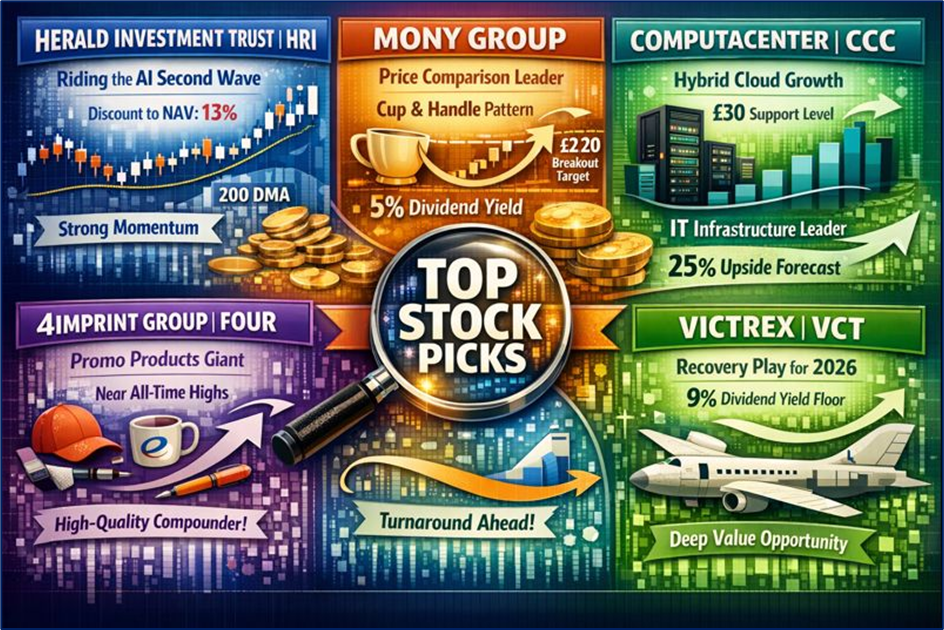

- Key Reasons & Drivers: Positioned as a premier vehicle for the global technology and communications sector. It benefits from the "AI Second Wave" where mid-sized tech enablers are finally seeing margin expansion.

- Latest Business Model: A specialized investment trust focusing on smaller companies in the technology, media, and telecommunications (TMT) space.

- Technical Analysis: The stock has recently broken out of a multi-year consolidation pattern. It is currently trading above its 200-day Moving Average (DMA) with the RSI (Relative Strength Index) indicating healthy momentum without being overbought.

- Latest Financial & Operational Updates: Recent reports highlight a narrowed discount to Net Asset Value (NAV), currently sitting at approximately 13%, which is tighter than the 20% historic average but still offers "value-gap" potential.

- Analyst Upgrades/Downgrades: InvestingPro recently assigned a "Good" health score with a fair value upside of over 31%.

- Risks: Exposure to high-beta tech volatility; potential for NAV dilution if the global tech sector faces a valuation reset.

- Key Reasons & Drivers: As UK households continue to navigate a "barbelled" consumption environment, the demand for price comparison and lead generation remains a defensive growth driver.

- Latest Business Model: Operates a diversified platform for insurance, energy, and financial product switching, increasingly leveraging AI to personalize user journeys.

- Technical Analysis: MONY is exhibiting a classic "cup and handle" formation on the weekly charts, suggesting a potential breakout above the £2.20 resistance level.

- Latest Financial & Operational Updates: Management recently confirmed a robust dividend yield of approximately 5.0%, supported by high free cash flow conversion.

- Analyst Upgrades/Downgrades: Multiple analysts have maintained "Buy" ratings in early 2026, citing a potential upside of up to 44% based on proprietary fair value models.

- Risks: Tightening regulations in the insurance switching market; increased competition from Google-integrated financial tools.

- Key Reasons & Drivers: A major beneficiary of the corporate "hardware refresh" cycle and the transition to hybrid cloud environments for public sector entities.

- Latest Business Model: An independent provider of IT infrastructure services, earning revenue through both technology sourcing (reselling) and high-margin managed services.

- Technical Analysis: The stock has shown strong support at the £30.00 level. Volume trends indicate institutional accumulation following its latest trading statement.

- Latest Financial & Operational Updates: Boasts a healthy balance sheet with a market cap of ~£3.1 billion and a sustainable 2.4% dividend yield.

- Analyst Upgrades/Downgrades: Upgraded by several brokers in late 2025 to "Outperform" with price targets suggesting a 25% upside as IT spending budgets normalize.

- Risks: Supply chain disruptions for high-end server components; slowing corporate CAPEX if global growth stutters.

- Key Reasons & Drivers: Dominant market share in the fragmented North American promotional products market. The company is using its scale to squeeze out smaller competitors through superior digital marketing.

- Latest Business Model: A direct marketer of promotional products (branded pens, apparel, etc.), utilizing a highly efficient data-driven customer acquisition model.

- Technical Analysis: Currently trading near all-time highs but maintaining a disciplined P/E ratio relative to its double-digit earnings growth.

- Latest Financial & Operational Updates: Recent trading updates showed a 5% daily price surge following better-than-expected organic revenue growth in its US division.

- Analyst Upgrades/Downgrades: Consistently receives "Buy" reiterations from mid-cap specialists who view it as a "high-quality compounder."

- Risks: High sensitivity to US marketing budgets; currency risk due to significant USD revenue exposure.

- Key Reasons & Drivers: A "recovery play" for 2026. After a significant share price slump in 2024-2025, the company is poised for a turnaround as its high-margin medical and aerospace polymers segments recover.

- Latest Business Model: A global leader in high-performance PEEK (Polyether ether ketone) polymers used in mission-critical industrial and medical applications.

- Technical Analysis: After falling significantly, the stock is showing signs of a "bottoming out" process. The dividend yield has reached a historic high of over 9%, acting as a floor for the share price.

- Latest Financial & Operational Updates: A new CEO took the helm in early 2026 with a mandate to optimize the product mix and restore profitability.

- Analyst Upgrades/Downgrades: While some remain cautious, value-oriented analysts have begun upgrading the stock to "Tactical Buy" due to the extreme valuation discount.

- Risks: Slower-than-expected recovery in medical device demand; potential for a dividend rebase if the turnaround takes longer than expected.

Conclusion

The FTSE 250 in 2026 represents a diverse hunting ground for investors. While Herald Investment Trust and Computacenter offer tech-driven growth, MONY Group and 4imprint provide robust operational cash flows. Victrex stands as the high-risk, high-reward value play. Overall, the index’s discount relative to the S&P 500 and even the FTSE 100 provides a significant margin of safety for those seeking double-digit returns.

Please wait processing your request...

Please wait processing your request...