The UK equity market has entered 2026 with unprecedented momentum. After the FTSE 100 shattered the 10,000-point ceiling in early January, retail and institutional interest has pivoted back to London. For an investor with £25,000, the landscape has shifted from "value-seeking" to "growth-capturing."

This analysis explores five premier UK growth stocks positioned to dominate the next twelve months, leveraging AI integration, global infrastructure booms, and pharmaceutical breakthroughs.

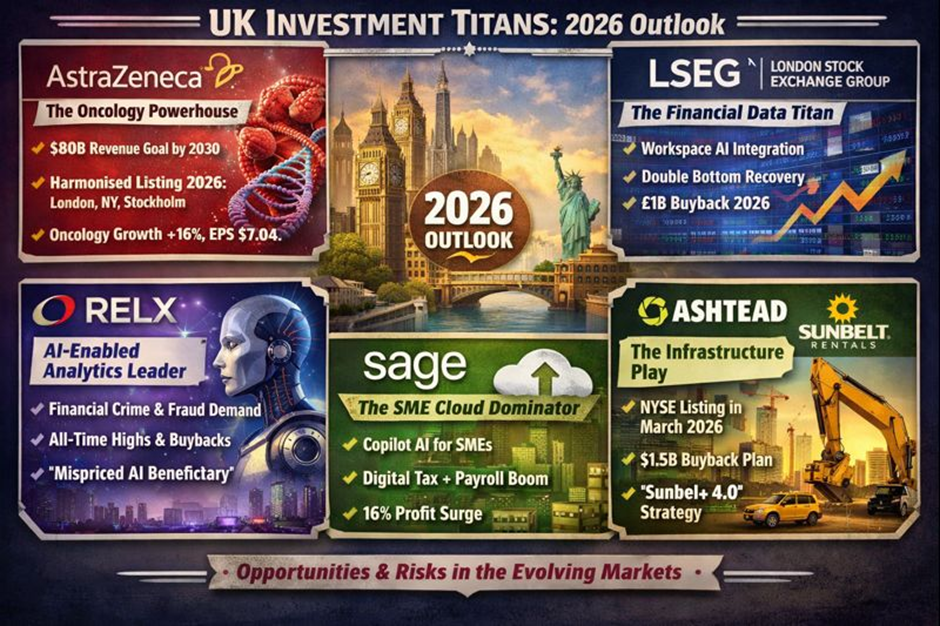

Source: Kalkine Group

AstraZeneca (AZN): The Oncology Powerhouse

Key Reasons & Drivers

- AstraZeneca remains the crown jewel of UK life sciences, driven by a relentless R&D engine and a goal to reach $80 billion in annual revenue by 2030.

- The 2026 catalyst is the full integration of its "Harmonised Listing Structure," allowing seamless global trading across London, New York, and Stockholm from February 2026, significantly increasing liquidity and institutional demand.

Technical Analysis & Financials

- The stock has recently broken out of a consolidation pattern near the £120 support level, with RSI indicators suggesting a healthy uptrend.

- Latest Financials: 9M 2025 revenue surged 11% to over $43 billion, with Oncology growing at 16%. Core EPS increased 15% to $7.04.

- Business Model: Transitioning from traditional pharma to a "biotech-plus" model, focusing on high-margin antibody-drug conjugates (ADCs) and rare disease therapies.

Analyst Sentiment & Risks

- Upgrades: Recent "Buy" reiterations from Goldman Sachs and J.P. Morgan cite the unprecedented 16 positive Phase III trial readouts in 2025 as a floor for 2026 valuation.

- Risks: High sensitivity to US drug pricing legislation and the inherent "binary risk" of late-stage clinical trials failing to reach commercialization.

London Stock Exchange Group (LSEG): The Financial Data Titan

Key Reasons & Drivers

- LSEG has successfully completed its transformation from a mere exchange to a global data and analytics behemoth, directly competing with Bloomberg and EODHD/Others.

- The 2026 driver is the "Workspace AI" rollout in H1, integrating Microsoft-backed natural language processing across its entire user base to automate complex financial modeling.

Technical Analysis & Financials

- After a volatile 2025, the stock is showing a "double bottom" formation, attracting "Growth at a Reasonable Price" (GARP) investors.

- Latest Financials: Organic income growth is tracking at 7%, with a committed £1 billion share buyback program concluding in February 2026.

- Business Model: Subscription-heavy (over 70% recurring revenue), focusing on high-value analytics, indices (FTSE Russell), and post-trade services.

Analyst Sentiment & Risks

- Upgrades: Morgan Stanley recently flagged a target price of 1,400p, viewing the Microsoft partnership as a multi-year margin expander.

- Risks: Competitive pressure from "open data" AI models and potential disruptions if global trade volumes decelerate due to new tariff regimes.

RELX PLC (REL): The AI-Enabled Analytics Leader

Key Reasons & Drivers

- RELX is the quiet winner of the AI era, utilizing proprietary datasets in legal, medical, and risk sectors to build high-moat decision tools.

- The 2026 momentum stems from its Risk segment, which is seeing surging demand for financial crime compliance and digital identity fraud solutions.

Technical Analysis & Financials

- The stock is currently testing all-time highs, supported by a £250 million tactical share buyback program running through Q1 2026.

- Latest Financials: Underlying revenue growth reached 7% in late 2025, with adjusted operating profit growth outpacing revenue.

- Business Model: A "platform-as-a-service" approach where 84% of revenue is now electronic/digital analytics rather than traditional publishing.

Analyst Sentiment & Risks

- Upgrades: Bank of America recently added RELX to its "25 Stocks for 2026" list, labeling it a "mispriced AI beneficiary."

- Risks: Data privacy regulations in the EU and US could impose higher compliance costs or limit data-scraping capabilities for new AI models.

Sage Group (SGE): The SME Cloud Dominator

Key Reasons & Drivers

- Sage has evolved into the "operating system" for Small and Medium Enterprises (SMEs), with its Sage Copilot AI assistant becoming a standard feature in 2026.

- Growth is fueled by the mandatory shift toward digital tax reporting and cloud-based payroll in the UK and North America.

Technical Analysis & Financials

- The stock exhibits a consistent "step-ladder" upward trend, with low volatility and strong support at the 200-day moving average.

- Latest Financials: FY2025 results showed a 16% jump in operating profit to £600 million; management forecasts at least 9% revenue growth for 2026.

- Business Model: A pure-play SaaS (Software as a Service) model with a 20-year track record of consecutive dividend increases.

Analyst Sentiment & Risks

- Upgrades: Citigroup upgraded Sage to "Buy" in late 2025, citing "sticky" customer retention and successful cross-selling of HR modules.

- Risks: Increased competition from Intuit (QuickBooks) and the impact of rising employment taxes on its SME customer base.

Ashtead Group (AHT): The Infrastructure Play

Key Reasons & Drivers

- Trading in the UK but earning 90% of its revenue in North America via Sunbelt Rentals, Ashtead is the primary beneficiary of the US "mega-project" boom.

- 2026 is a milestone year: Ashtead moves its primary listing to the New York Stock Exchange in March 2026, which is expected to trigger a significant valuation re-rating.

Technical Analysis & Financials

- The chart shows an ascending triangle pattern, typically a bullish indicator ahead of major corporate actions like a listing change.

- Latest Financials: Record free cash flow of $1.1 billion in H1 2026; a new $1.5 billion share buyback commences in March 2026.

- Business Model: "Rental-as-a-Service," shifting from general tool hire to high-margin "Specialty" segments like power, climate control, and disaster relief.

Analyst Sentiment & Risks

- Upgrades: Analysts view the "Sunbelt 4.0" strategy as a blueprint for 15%+ ROIC, with several US-based funds initiating "Buy" ratings ahead of the NYSE move.

- Risks: Cyclicality in the construction market and exposure to high interest rates, which increases the cost of fleet financing.

Conclusion: Navigating the 2026 Growth Cycle

The UK market in 2026 is no longer just a "dividend play." For an investor with £25,000, these five companies offer a blend of technological disruption (RELX, Sage), global scale (AstraZeneca), and structural infrastructure tailwinds (Ashtead). While the FTSE 100’s recent highs provide a supportive backdrop, the 2026 winner’s circle will likely be defined by companies that can successfully monetize AI and navigate the shifting transatlantic regulatory environment.

Please wait processing your request...

Please wait processing your request...