The £5,000 Reveal: A 51% Rocket Ride

If you strategically deployed £5,000 into Advanced Micro Devices (AMD) during the market uncertainty of mid-July 2025, your portfolio would arguably be the envy of Wall Street today. Based on the current trajectory and the explosive recovery witnessed over the last two quarters, that capital has swelled to approximately £7,550. This represents a profit of £2,550—a staggering 51% return in just six months.

While the broader indices grinded out respectable single-digit gains, AMD shareholders benefited from a violent repricing as the market realized the gap between AMD and the industry leader was closing faster than anticipated. This calculation highlights the power of "contrarian" investing: buying when the narrative was mixed, and holding as the "AI Supercycle" entered its second, more mature phase.

Key Reasons & Drivers: The Second Wave of AI CapEx

Source: Kalkine Group

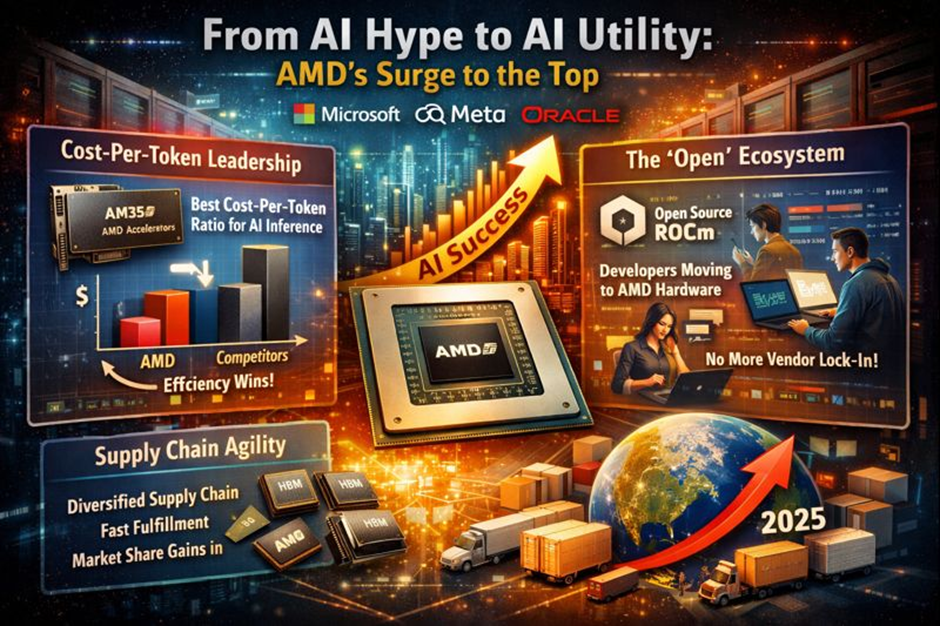

The driving force behind this surge is the transition from "AI hype" to "AI utility." Hyperscalers like Microsoft, Meta, and Oracle have shifted their spending patterns, benefitting AMD’s specific approach to the market.

- Cost-Per-Token Leadership: The primary driver has been the economic reality of AI inference. As large language models (LLMs) moved from training to deployment, customers flocked to AMD’s MI350 accelerators, which offer a superior cost-per-token ratio compared to competitors.

- The "Open" Ecosystem: AMD’s commitment to open-source software via ROCm has finally paid off. Developers previously locked into proprietary ecosystems have migrated to AMD hardware to avoid vendor lock-in, creating a grassroots swell of demand that surprised analysts.

- Supply Chain Agility: While peers struggled with HBM (High Bandwidth Memory) shortages, AMD’s diversified supply chain allowed them to fulfill orders faster, capturing critical market share during the Q3 and Q4 2025 rush.

Current Technical Analysis: Bullish Structure with "Air Pockets"

Source: Trading View

Technical indicators suggest that the stock is currently in a strong uptrend, characterized by higher highs and higher lows, though it is approaching a level that often invites profit-taking.

- Momentum Oscillators: The stock is trading well above its rising 50-day moving average, acting as dynamic support. However, the RSI (Relative Strength Index) is teasing the 55 level, indicating the stock is technically "neutral" and may need to consolidate sideways to digest these recent gains.

- Volume Profiles: The rally has been supported by "high volume nodes" on up-days, confirming that institutions—not just retail traders—are accumulating shares. There is a distinct lack of resistance (an "air pocket") above current levels, meaning volatility could be high as the stock seeks a new equilibrium.

- Gap Support: Several price gaps left behind during earnings surprises in late 2025 remain unfilled. These often act as magnetic support levels if the broader market experiences a correction.

Latest Analyst Sentiment: The "Catch-Up" Trade

Wall Street has effectively admitted it was behind the curve on AMD. The narrative has shifted from skepticism to a "must-own" infrastructure play.

- Upgrades Galore: Leading firms have revised their 12-month price targets upward, with the "Street High" target now implying a move toward $300. The consensus rating has firmed to a "Strong Buy," with analysts citing the massive TAM (Total Addressable Market) expansion for 2027.

- Institutional Rotation: Fund managers who were overweight on other semiconductor names have been rebalancing into AMD to hedge their exposure. This "rotation" creates persistent buying pressure that cushions the stock against minor dips.

Business Model Evolution: Beyond the CPU

The company that your £5,000 bought into is no longer just a chip designer; it is a heterogeneous computing platform. The business model has successfully pivoted toward high-margin data centre dominance.

- Data Centre First: For the first time, Data Centre revenue has decisively eclipsed the Client and Gaming segments combined. This shift fundamentally alters the valuation multiples investors are willing to pay, as data centre revenue is viewed as more durable and higher margin.

- Semi-Custom Stability: While the gaming console cycle has matured, the semi-custom division provides steady, predictable cash flow that acts as a ballast, allowing the company to take aggressive risks in AI R&D.

Financial & Operational Updates: Efficiency at Scale

Financially, the company is demonstrating "operating leverage," meaning revenue growth is outpacing expense growth.

- Gross Margin Expansion: Margins have ticked upward, approaching the mid-50s percent range. This is largely due to the rich product mix of high-end AI accelerators which command premium pricing power.

- Free Cash Flow Generation: The company is generating robust free cash flow, which is being deployed into share repurchases. This reduces the share count and artificially boosts Earnings Per Share (EPS), adding more fuel to the stock price.

- Dividend Status: AMD continues to pay no dividend. Management maintains that the best return on capital is reinvestment into the business and strategic acquisitions, a stance that growth investors overwhelmingly support.

Risks: The "High Expectations" Trap

Despite the 51% gain, the path forward for your £7,550 is not risk-free. The market has now priced in near-perfect execution for the next 12 months.

- Valuation Premium: The stock trades at a premium forward P/E multiple. Any sign of slowing growth in the data center segment—even if it's just a return to "normal" growth—could trigger a sharp multiple contraction.

- Geopolitical Exposure: The reliance on TSMC in Taiwan remains a single point of failure. Any geopolitical escalation in the region represents a "black swan" event that could erase gains overnight.

- Competitive Response: The competition is fierce. If rivals slash prices to protect market share, AMD’s margins could compress, undermining the profitability narrative that supports the current stock price.

Conclusion: A Winning Bet on the Future

In summary, the decision to invest £5,000 in AMD six months ago has yielded a remarkable £2,550 profit, validating the thesis that the AI market has room for more than one winner. The company has executed flawlessly on its roadmap, proving the skeptics wrong and rewarding the believers.

While the easy money has likely been made, the long-term compounding story remains intact. Investors holding this position are now sitting on a significant cushion of profit, allowing them to weather future volatility with confidence. The "Smart Money" suggests holding the core position while perhaps trimming slightly to manage risk, as the AI era is still in its early innings.

Please wait processing your request...

Please wait processing your request...