The Big Move: On January 6, 2026, AstraZeneca (LSE: AZN) defied the typical "slow-moving blue chip" label, surging ~5% to close at approximately GBX 14,056.

While the broader FTSE 100 reached a historic milestone by trading above 10,000, AstraZeneca was the primary engine behind the rally.

Key Drivers: Why is AstraZeneca Up Today?

Source: Kalkine Group

The 5% jump isn't a fluke; it's the culmination of three massive catalysts hitting the wire simultaneously:

- AI Oncology Breakthrough: AstraZeneca announced a strategic collaboration with BostonGene to use AI foundation models for tumor and immune biology. This moves AZN from "traditional pharma" to "tech-bio," aiming to predict patient responses and de-risk early-stage clinical trials.

- The "Lifting Tide" Effect: The FTSE 100 broke its psychological ceiling of 10,000, triggering massive institutional inflows. As the largest constituent by market cap (approx. £211bn), AstraZeneca is the first destination for global funds entering the UK market.

- Regulatory Tailwinds: New reports suggest the UK government is increasing medicine spending to secure carve-outs from potential US trade tariffs. This protects AZN’s massive US export business while shoring up domestic revenue.

Latest Business Model: The "Precision & Proximity" Strategy

AstraZeneca has transitioned from a generalist pharmaceutical company to a precision medicine powerhouse. Their 2026 model rests on four pillars:

- Oncology Dominance: Led by blockbusters like Enhertu and Tagrisso, cancer treatments now account for over 35-40% of total revenue.

- The Rare Disease Engine: Following the Alexion acquisition, AZN has integrated high-margin "orphan drugs" (like Soliris and Ultomiris) that face less competition and enjoy longer patent protection.

- Global Harmonization: The board recently proposed a "Harmonised Listing Structure" across London, Stockholm, and New York, making the stock more accessible to US retail and institutional investors.

- In-House Manufacturing: Moving away from outsourcing, AZN recently broke ground on a $4.5bn Virginia facility to "onshore" supply chains for the US market.

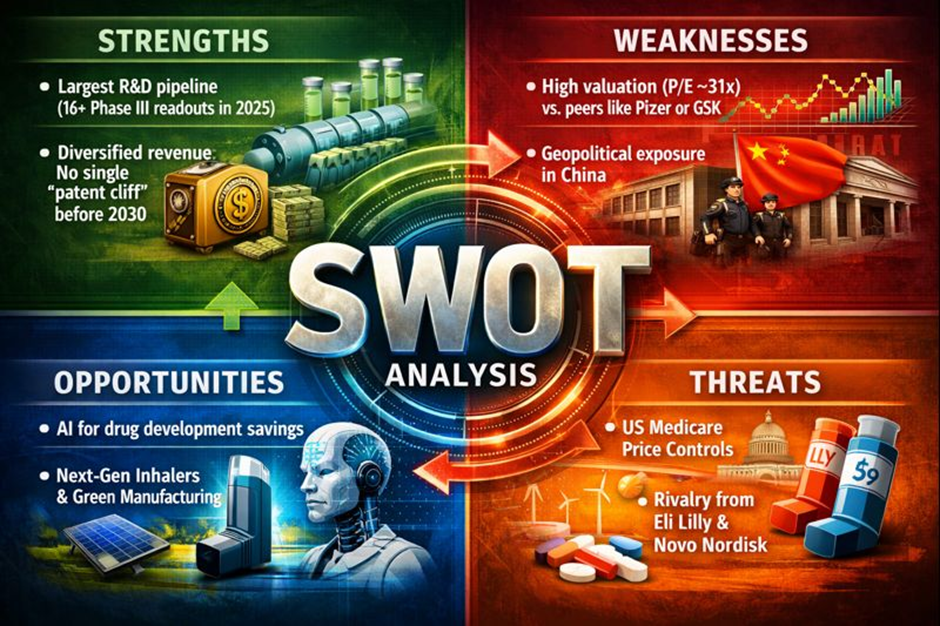

AstraZeneca SWOT Analysis

Source: Kalkine Group

Financial & Operational Update

- Revenue Growth: In the most recent 9M 2025 report, total revenue grew 11% (CER), hitting $43.2 billion.

- Earnings Per Share (EPS): Core EPS increased 15% to $7.04, beating analyst consensus.

- Dividend Yield: Currently sitting at ~1.75%, AZN remains a "High Flyer" that prioritizes growth reinvestment over massive payouts.

- Operations: The company has hit its target of 100% renewable energy for power and heat across its global sites as of early 2026.

Risks to Watch

Despite the euphoria, retail investors should monitor two specific risks:

- The "Trump Tariff" Variable: With the US being AZN's largest market, any disruption in trade relations or increased pressure on drug pricing could hit the bottom line.

- Clinical Trial Failure: Even with AI, high-profile Phase III trials (like the recent ceralasertib results) can fail, leading to sharp, short-term price corrections.

Conclusion

AstraZeneca’s 5% surge on January 6 is a reflection of its status as the "Gold Standard" of the FTSE 100. By blending aggressive AI adoption with a rock-solid oncology portfolio, the company has convinced the market that it can grow like a tech stock while providing the stability of a healthcare giant. As the FTSE 100 enters the "10k Era," AstraZeneca remains the undisputed leader of the pack.

Please wait processing your request...

Please wait processing your request...