Key Takeaways:

The exact, single driver for today's ~3.2% surge in Auto Trader Group PLC (AUTO) stock isn't explicitly identified in today's news. However, the movement likely reflects a combination of strong underlying financial health, positive sentiment from recent innovation, and an uplift from a generally robust UK used car market. The daily fluctuation may represent a market reaction to ongoing high-margin performance and the company's defensive 'moat.'

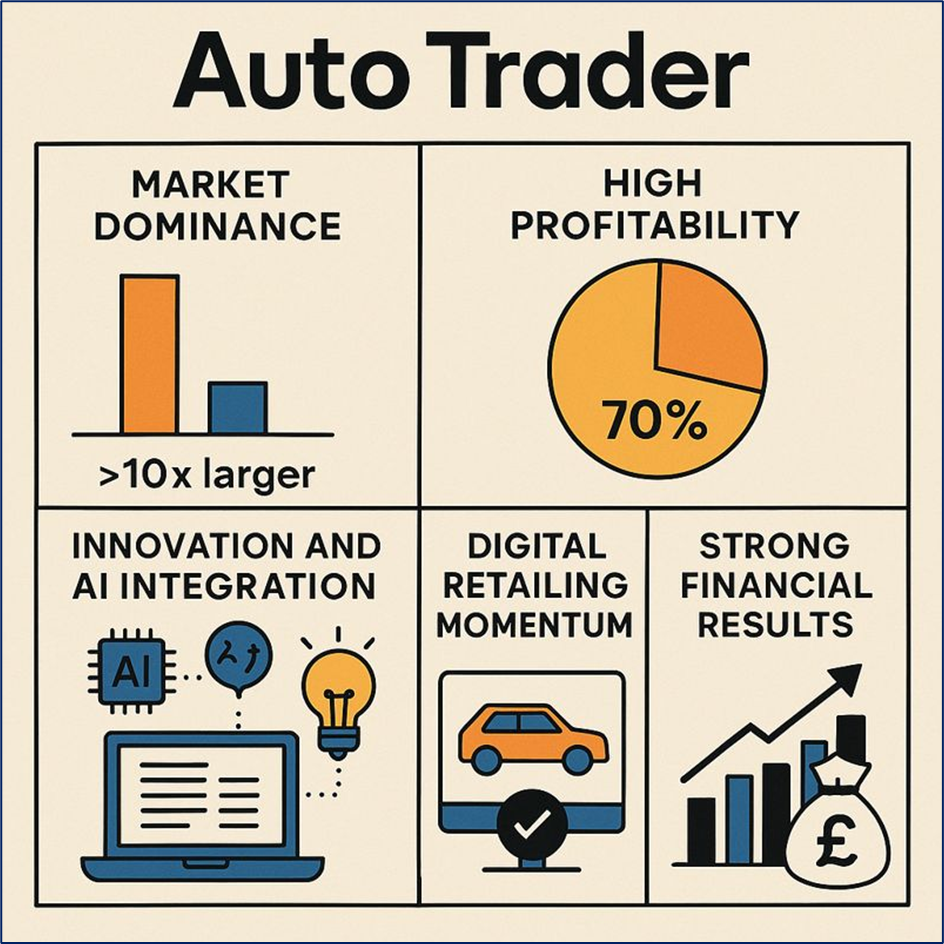

Key Reasons & Drivers of Performance

The company's sustained strength is built on several pillars, which feed into positive investor sentiment:

- Market Dominance (The Moat): Auto Trader is the UK's undisputed leading automotive platform, with over 75% of all minutes spent on UK automotive marketplaces occurring on their platforms, making it more than 10x larger than its nearest competitor. This provides significant pricing power.

- High Profitability: The core Auto Trader business boasts an exceptional operating profit margin of approximately 70%, a key feature of its business model that appeals to investors.

- Innovation and AI Integration: The launch and scaling of Co-Driver, a suite of AI-powered tools (like AI-generated descriptions and Smart Image Management), are improving efficiency for car retailers, strengthening the value proposition, and driving adoption.

- Digital Retailing Momentum: The continued scaling of Deal Builder, a digital retailing product that allows consumers to complete more of the transaction online, demonstrates a successful push into the transactional part of the market.

- Strong Financial Results: Recent half-year results (to Sep 30, 2025) showed continued growth, with a 5% rise in Group revenue and an 11% increase in Basic Earnings Per Share (EPS), demonstrating confidence through increased share buybacks and dividends.

Source: Kalkine Group

The Money Engine: Auto Trader's Business Model

Auto Trader operates primarily as a high-margin digital marketplace with a powerful network effect:

- Subscription Revenue (Core): Car retailers (dealers) pay monthly subscription packages to list their vehicles on the platform. This is the bedrock of the revenue model.

- Advertising/Product Revenue (ARPR Driver): Retailers purchase "premium" products (like higher-prominence listings) and data-driven insights to help them sell cars faster and more profitably. Average Revenue Per Retailer (ARPR) growth is a critical metric, recently driven by annual pricing events and the take-up of new products like Co-Driver.

- Digital Services: Revenue from acquisitions like Autorama (Vanarama), which focuses on new vehicle leasing, diversifies the revenue streams.

The Roadblocks: Key Risks

Despite its strong position, Auto Trader faces material risks:

- Regulatory Scrutiny: Concerns have been raised, including an FCA investigation into motor finance, which can impact the broader industry and dealer sentiment.

- Dealer Backlash/Pricing Pressure: Public protests and threats of package downgrades/cancellations by car dealers due to high listing prices could pressure future ARPR growth.

- Competition and Disintermediation: While dominant, the rise of other platforms (Motors.co.uk, CarGurus) and the potential for new entrants in the digital retailing space (e.g., Cazoo/Cinch models) pose a competitive threat.

- Data Strategy: The company is cautiously navigating how much of its proprietary data it shares with large AI platforms to protect its competitive advantage.

Conclusion: A High-Quality Monopoly in the Digital Auto Space

Auto Trader's stock movement today is likely a reinforcement of its status as a high-quality, highly profitable monopoly in the UK automotive classifieds space. Its formidable market share, high-margin, and proven ability to successfully transition to digital and integrate cutting-edge AI (Co-Driver) provide a compelling narrative of sustainable growth, even amidst macro uncertainties. The short-term risks, such as dealer sentiment and used car supply, appear to be offset by its long-term, structurally advantaged market position.

Source: Trading View, 15 December 2025

Please wait processing your request...

Please wait processing your request...