The first trading day of 2026 kicked off with a notable spark for Centrica (LSE: CNA). While the FTSE 100 toyed with the historic 10,000-point mark, Centrica shares outperformed many of its blue-chip peers, closing up ~2.8% at 174.35p.

This wasn’t just a "New Year rally" fluke. From aggressive share buybacks to a strategic pivot toward "Green Base-load" power, Centrica is repositioning itself from a volatile energy trader to a stable, green infrastructure play.

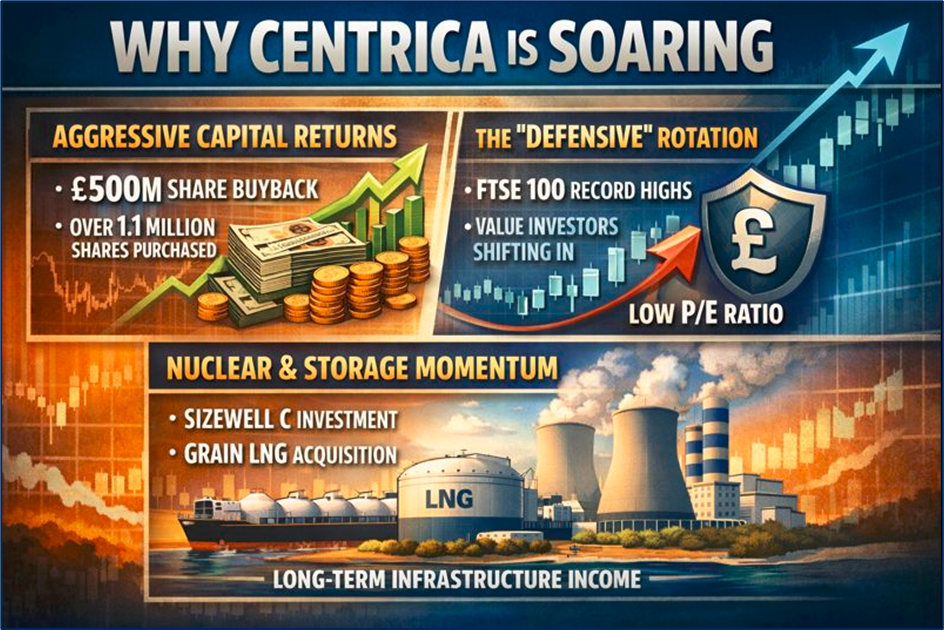

Key Drivers: Why the Stock Popped on Jan 2

Source: Kalkine Group

The ~2.8% gain on January 2nd was driven by a combination of technical momentum and fundamental reassurance:

- Aggressive Capital Returns: On the morning of Jan 2, Centrica confirmed a "Transaction in Own Shares," revealing it had purchased over 1.1 million shares on the final day of 2025 as part of its ongoing £500 million buyback tranche. This relentless reduction in share count continues to support the stock price.

- The "Defensive" Rotation: As the FTSE 100 hit record highs, investors shifted toward "cheaper" areas of the market. With a P/E ratio significantly lower than the tech-heavy US markets, Centrica’s defensive profile—utility-linked earnings and massive cash reserves—became a magnet for value-seeking capital.

- Nuclear & Storage Momentum: Recent late-2025 updates, including the finalized investment in Sizewell C and the acquisition of Grain LNG, have signaled to the market that Centrica is successfully replacing declining North Sea gas earnings with long-term, regulated infrastructure income.

Business Model 2026: "The Integrated Energy Pivot"

Centrica has moved away from the "British Gas" identity of old. Its 2026 business model is built on three integrated pillars:

- Retail (British Gas Energy/Services): Focused on "smart" home management and heat pump installations. The goal is higher customer retention through the Hive ecosystem.

- Optimisation (Centrica Energy): A sophisticated trading arm that manages the volatility of renewable energy, buying and selling power to balance the grid.

- Infrastructure (The "Green Engine"): This is the growth sector. Centrica is now a major player in Energy Storage+ (the Rough gas storage facility) and is investing heavily in Solar, Battery Storage, and Nuclear (Sizewell C).

2026 SWOT Analysis: The Deep Dive

Source: Kalkine Group

Strengths

- Cash King: A robust balance sheet with over £2.4bn in net cash (as of latest interim data) allows for consistent dividends and buybacks.

- Market Dominance: British Gas remains the UK's largest energy supplier, providing a massive, sticky customer base.

- Integrated Value Chain: Unlike pure retailers, Centrica can produce, store, and trade the energy it sells, protecting margins.

Weaknesses

- Earnings Volatility: Despite the shift, the "Optimisation" (trading) arm is still sensitive to commodity price swings.

- Service Recovery: The "Services & Solutions" wing (boiler repairs, etc.) has historically struggled with profitability and customer satisfaction compared to the energy supply wing.

Opportunities

- Hydrogen Transition: Centrica is exploring turning its storage assets (like Rough) into hydrogen hubs.

- Small Modular Reactors (SMRs): Strategic partnerships (like X-energy) position Centrica at the forefront of the next nuclear wave.

- Data Centre Demand: Rising UK electricity demand from AI data centres provides a new, high-volume B2B market.

Threats

- Regulatory Squeeze: The UK's Ofgem price cap remains a constant threat to retail margins.

- Geopolitical Risk: Global gas prices are susceptible to conflicts, which can lead to unpredictable windfall taxes or government intervention.

- Windfall Tax Uncertainty: Continued political debate over "excess profits" in the energy sector creates a valuation overhang.

Latest Financial & Operational Updates

- Dividend Growth: Centrica is on track for a total dividend of 5.5p per share for the 2025/26 cycle, representing a significant 22% year-on-year increase.

- Clean Energy Milestone: As of January 2026, over 50% of capital expenditure is now directed toward "green taxonomy" projects, up from just 5% in 2019.

- Operational Efficiency: The company is currently undergoing a "lean" transformation, aiming to deliver around £800m in sustainable operating profit from Retail and Optimisation alone by the end of 2026.

The Risk Landscape

While the stock is currently in favor, investors are monitoring:

- Weather Sensitivity: A warmer-than-expected winter in 2025/26 could suppress gas demand in the retail segment.

- Nuclear Outages: As a stakeholder in the UK's aging nuclear fleet, any unplanned maintenance shutdowns can lead to sudden earnings hits.

- Interest Rates: As a capital-intensive business (especially with the Sizewell C build), prolonged high interest rates could increase the cost of future debt-funded projects.

Conclusion

Centrica’s 2.8% jump on the first day of 2026 reflects a growing market consensus: the company is no longer just a "gas man." By leveraging its massive cash pile to buy back shares and fund the UK’s energy transition, Centrica has transitioned into a hybrid utility-infrastructure play. While commodity volatility remains a "known unknown," the structural shift toward regulated, green income is providing the "valuation floor" that investors have long waited for.

Please wait processing your request...

Please wait processing your request...