Key Takeaways: The Copper Mega-Trend is Real

The ~4% surge in Antofagasta's FTSE-100 stock is a direct response to two core factors: the soaring global price of copper (which recently crossed the $11,800 per tonne mark) and the company's solid operational execution focused on growth and cost control.

- Copper Price Momentum: The commodity market is pricing in a long-term supply deficit, driven by the insatiable demand from the global energy transition (EVs, renewable power grids). Antofagasta, as a pure-play copper miner, benefits directly from this macro-tailgate.

- Operational Confidence: The company has recently lowered its net cash cost guidance for 2025 to $1.20–1.30/lb due to strong by-product credits (especially Gold and Molybdenum) and currency benefits, signaling improved financial resilience.

- Growth Pathway: Major projects like the Centinela Second Concentrator are progressing on schedule, laying the groundwork for an expected 30% medium-term production increase and higher-margin output.

Reasons & Drivers: The Electrification Story

Antofagasta's valuation is tightly linked to the "future of energy" narrative, positioning it as a key beneficiary of global decarbonization efforts. The recent stock jump highlights the market's urgency to secure exposure to this essential metal.

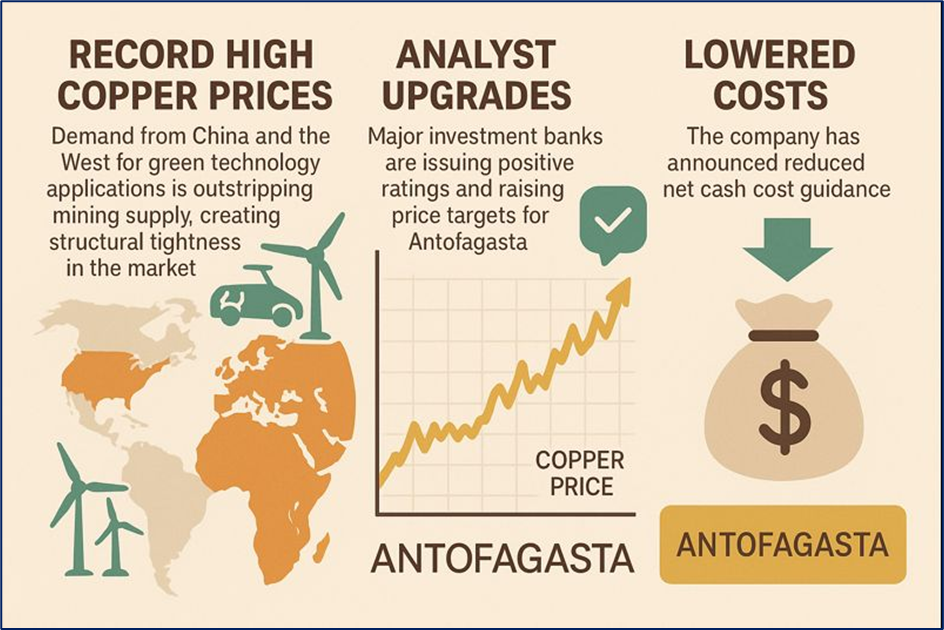

The primary drivers for the share price increase are:

- Record High Copper Prices: Demand from China and the West for green technology applications is outstripping mining supply, creating structural tightness in the market. The high copper price directly boosts Antofagasta's revenue and profit margins.

- Analyst Upgrades: Following the solid operational reports, major investment banks have been issuing positive ratings and raising their price targets for Antofagasta, fuelling retail and institutional buying interest.

- Lowered Costs: The company’s announcement of a reduced net cash cost guidance for the full year 2025 (down from the previous $1.45-$1.65 range) improves expected profitability and provides a larger buffer against future copper price volatility.

Source: Kalkine Group

Latest Business Updates & Focused Business Model

Antofagasta is structured as a focused, high-quality copper producer primarily operating in Chile. Its business model centers on maximizing output from long-life assets while strategically investing for future growth.

The key aspects of its latest business activity and core model include:

Business Model Core:

- Pure-Play Copper Focus: The business is centered on the extraction and processing of copper concentrate and cathodes from its four main operations: Los Pelambres, Centinela, Antucoya, and Zaldívar.

- By-Product Revenue: Critical to the low-cost profile is the significant revenue generated from valuable by-products like gold and molybdenum, which act as a powerful credit against production costs.

- Chilean Concentration: All primary assets are located in Chile, the world’s largest copper-producing nation, allowing for scale and expertise, but also concentrating geopolitical and regulatory risks.

Recent Operational Momentum:

- Centinela Project: Construction on the Centinela Second Concentrator is proceeding on track and on budget, confirming a clear path to a substantial production boost in the coming years.

- Water Resilience: The company is actively investing in and deploying water security solutions, particularly its desalination plants, to mitigate the critical risk of water scarcity in the arid Chilean mining regions.

- Production Guidance: Full-year 2025 copper production is expected to be at the lower end of the 660-700 kilotonnes (Kt) range, a robust figure supported by increased throughput and grades anticipated at Los Pelambres in the final quarter.

Risks: The Roadblocks Ahead

Despite the powerful tailwinds, investors must acknowledge the specific risks inherent in the mining sector and Antofagasta’s concentrated operation:

- Copper Price Swings: The 4% gain is fundamentally tied to the price of copper. Any cooling in global industrial demand (especially in China) or a slowdown in the electrification trend could trigger sharp profit-taking.

- Chilean Regulatory Environment: Changes in the local mining royalty framework or stricter environmental/water regulations could significantly increase the company's tax burden and operating expenses.

- Cost Inflation: Sustained global inflation in inputs like energy, sulfuric acid, and labor could erode the impressive cost savings achieved through higher by-product credits.

- Resource Management: Over the long term, declining ore grades at mature assets like Los Pelambres necessitate heavy capital expenditure (capex), currently guided to be around $3.6 billion for 2025, to maintain production levels.

Conclusion

Antofagasta's 4% stock rally today is a market signal that the structural growth story of copper is accelerating, making miners with proven reserves and clear expansion plans highly attractive. The company is delivering on operational efficiencies, evidenced by its lowered net cost guidance and the smooth progression of key growth projects. While the valuation is becoming elevated and the stock remains highly sensitive to copper price volatility, its strategic position as a low-cost, growth-focused producer in the heart of the copper world positions it well to capitalize on the global push towards electrification.

Source: Trading View, 15 December 2025

Please wait processing your request...

Please wait processing your request...