Empyrean Energy PLC (LSE: EME) capped off 2025 with a dramatic 35.71% surge on December 31, closing at 0.05 GBX. After a year defined by the tragic loss of CEO Tom Kelly and a high-stakes legal standoff with its Indonesian partner, the stock's year-end rally has captured the attention of retail investors and micro-cap analysts alike.

Why the Spike? Key Drivers of the 31 Dec Surge

Source: Kalkine Group

The 36% jump appears to be a classic "relief rally" combined with institutional "window dressing" as the year closed. Several factors converged to spark this late-December momentum:

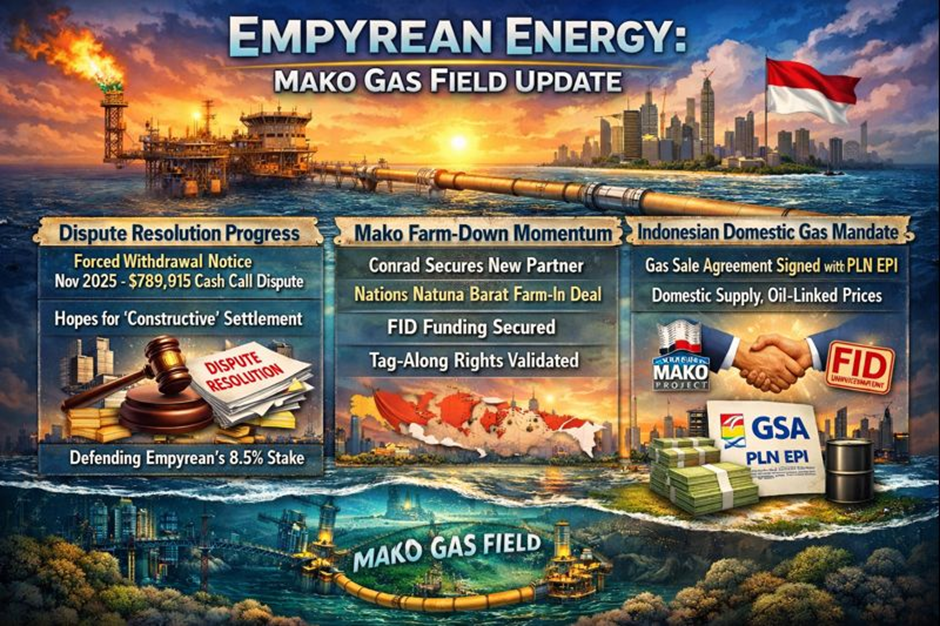

- Dispute Resolution Progress: Following a "Notice of Forced Withdrawal" issued by the operator (Conrad Asia Energy) in November 2025 over a $789,815 cash call dispute, the market reacted to hints of a "constructive" settlement. Investors are betting that Empyrean will successfully defend its 8.5% stake in the Mako Gas Field, which is the company's crown jewel.

- Mako Farm-Down Momentum: The operator, Conrad, recently secured a farm-in partner (Nations Natuna Barat) for the Mako project. This provides the necessary funding for the Final Investment Decision (FID), directly validating the value of Empyrean’s "tag-along" rights.

- Indonesian Domestic Gas Mandate: In late 2025, the Indonesian government shifted all Mako gas production to the domestic market. While this initially caused uncertainty, the signing of a binding Gas Sale Agreement (GSA) with PLN EPI (Indonesia’s state utility) at oil-linked prices has provided a concrete revenue floor.

Latest Business Model: From Explorer to Developer

Empyrean’s business model has shifted from high-risk wildcat exploration to a targeted asset development and monetization strategy.

- Core Focus (Indonesia): The priority is the Duyung PSC, containing the Mako Gas Field (one of the largest undeveloped gas fields in the West Natuna Sea). The model here is to maintain an 8.5% interest through to production (targeted for 2026) or sell the stake to a larger player.

- Asset Rationalization: After the failure of the Wilson River-1 well in Australia (which produced formation water instead of oil in May 2025), Empyrean is pivoting away from high-cost terrestrial drilling to focus on proven offshore resources.

- Capital Light Strategy: Following multiple fundraises in 2025 (totaling over £2.5 million), the company is strictly managing overhead to survive until the Mako field reaches FID.

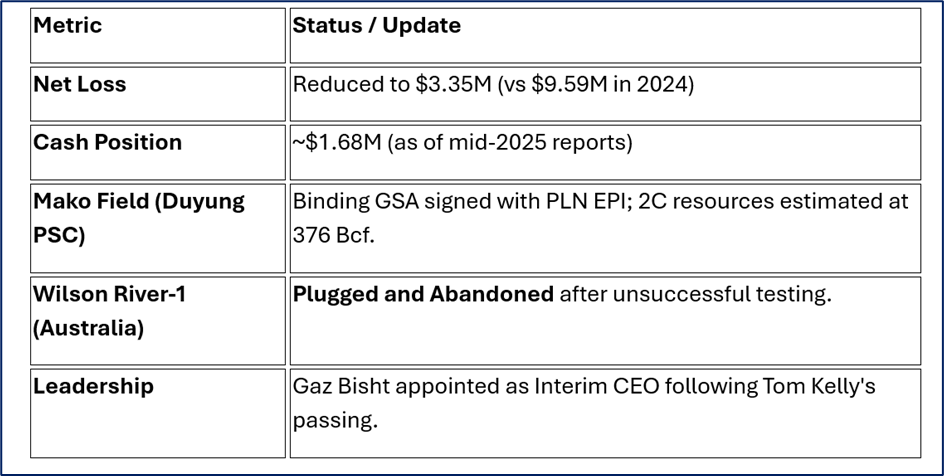

Financial & Operational Update: 2025 in Review

Source: Company Data

SWOT Analysis: The 2026 Outlook

Source: Kalkine Group

Strengths

- High-Value Asset: The Mako Gas Field is a world-class resource with binding sale agreements.

- Strategic Location: Proximity to Singapore and Indonesian infrastructure makes the gas highly marketable.

- Operational Validation: Farm-in by Nations Natuna Barat proves the project's bankability.

Weaknesses

- Legal Vulnerability: The ongoing dispute with Conrad over unpaid cash calls remains a "sword of Damocles" over the 8.5% stake.

- Funding Gaps: Frequent dilutive share placements are needed to cover operational costs.

- Micro-cap Liquidity: Small market cap leads to extreme price volatility.

Opportunities

- Tag-Along Rights: The potential to sell the 8.5% stake alongside the operator at a premium.

- Indonesian Energy Transition: High demand for gas as Indonesia shifts away from coal.

- Arbitration Success: A favorable legal outcome could fully restore market confidence and share value.

Threats

- Forced Withdrawal: If the legal dispute fails, Empyrean could lose its entire stake in the Duyung PSC.

- Regulatory Shifts: Changes in Indonesian domestic gas pricing or export taxes.

- Commodity Prices: Significant drops in the Indonesian Crude Price (ICP) would devalue the GSA.

Risk Factors for 2026

Investors must weigh the high-reward potential of Mako against severe risks. The Nov 2025 Forced Withdrawal Notice is the primary threat; if enforced, the stock's value proposition essentially disappears. Furthermore, the company remains in a loss-making position and will likely require further capital injections before first gas is achieved in late 2026.

Conclusion

The 36% jump on December 31, 2025, reflects a market that is beginning to price in a successful resolution to the Mako dispute and the eventual commercialization of the Duyung PSC. While the operational failure in Australia was a blow, the Indonesian gas assets remain a potent driver for 2026. However, with legal hurdles still in the path, the road ahead for Empyrean remains as volatile as its year-end performance.

Please wait processing your request...

Please wait processing your request...