If you had invested GBP 1,000 in MobilityOne (LSE: MBO) just one month ago, you would be looking at one of the most explosive short-term returns on the FTSE AIM market this year.

On December 16, 2025, the stock was trading at approximately 0.78p. As of mid-January 2026, the price has surged to 8.50p (hitting highs of 12.50p earlier in the month). Your initial £1,000 investment would now be worth approximately £12,780—a staggering 1,178% return in just ~30 days.

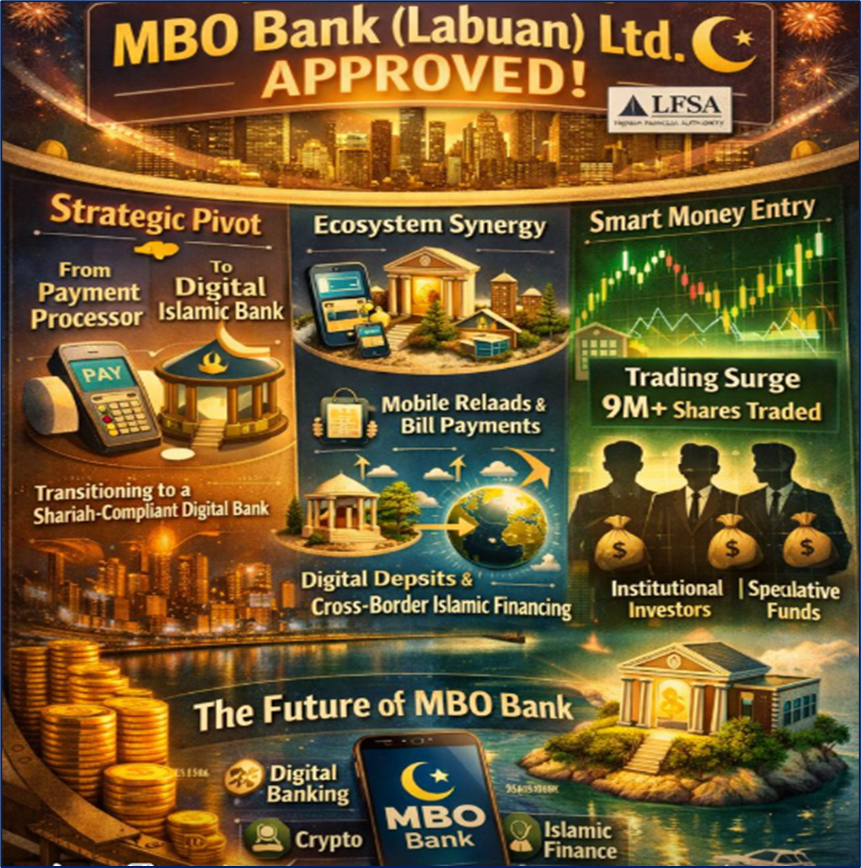

Key Drivers and the "Islamic Banking" Catalyst

Source: Kalkine Group

The primary driver for this vertical price action was the landmark announcement on December 31, 2025. MobilityOne’s Malaysian subsidiary received conditional approval from the Labuan Financial Services Authority (LFSA) to establish MBO Bank (Labuan) Ltd.

- Strategic Pivot: The company is transitioning from a high-volume, low-margin payment processor into a full-scale Shariah-compliant digital bank.

- Ecosystem Synergy: By leveraging its existing network of mobile reloads and bill payments, MBO plans to offer offshore financial services, including digital deposits and cross-border Islamic financing.

- Smart Money Entry: High trading volumes (exceeding 9 million shares on peak days) suggest institutional "flippers" and speculative funds moved in to capitalize on the news of the banking license.

Current Technical Analysis: Overextended or Just Beginning?

Technically, MBO is currently in a "blue sky" breakout phase but showing signs of extreme volatility.

- Momentum Metrics: The stock is trading 477% above its 200-day Moving Average, a classic sign of an overbought condition in the short term.

- Support & Resistance: Significant support has formed at the 7.00p level, while the 12.50p mark remains the immediate psychological resistance.

- Volume Profile: The massive volume spike in early January suggests a "change of hands" from long-term retail bag-holders to aggressive momentum traders. A period of consolidation or a "cooling off" back to the 5.00p–6.00p range would be technically healthy before any further leg up.

Latest Analyst View: Upgrades and Sentiment

While formal "Investment Bank" coverage for AIM micro-caps is sparse, boutique brokers and research houses like Stockopedia have shifted their sentiment.

- Ratings Shift: Sentiment has moved from "Speculative/Avoid" to a "Neutral/Momentum" classification.

- Broker Outlook: Analysts note that while the banking license is a "game-changer," the company has explicitly stated it expects zero revenue from the digital bank in the 2026 financial year due to preparatory work. This creates a "valuation gap" where the stock is trading on future potential rather than current earnings.

Latest Business Model and Financial Updates

MobilityOne operates a diversified fintech model, but the core revenue still comes from its Telecommunication Services segment.

- Operational Footprint: Leading virtual distributor of mobile prepaid reloads in Malaysia, connected to major banks, hypermarkets, and telcos.

- 2026 Outlook: Management is focusing on meeting the LFSA's conditions for the new bank. The company recently narrowed its interim losses, reporting an annual turnover of approximately £230.23 million, though it remains currently unprofitable at the bottom line.

- Valuation: Market Cap has swelled to approximately £7.44M to £9M depending on daily fluctuations. With a Price-to-Sales ratio that remains incredibly low compared to peers, the "Value" argument is based on the massive top-line revenue finally being converted to profit via the higher-margin banking arm.

Dividends and Risk Profile

- Latest Dividend: The company does not currently pay a dividend. All capital is being redirected toward the digital banking infrastructure and regulatory compliance.

- Major Risks: The CEO, Hussain Rahman, holds over 50% of the shares, leading to low "free float" and high price sensitivity. Additionally, the "Execution Risk" is high; if the company fails to meet the final conditions of the Labuan FSA, the stock could retracing its entire 1,000% gain as quickly as it made it.

- Margin Concerns: Analysts have highlighted a deterioration in profit margins (from 13% to 7.1%), suggesting the core business faces stiff competition.

Conclusion

MobilityOne has transformed from a forgotten AIM laggard into a high-octane fintech play. The move into Islamic digital banking provides a massive TAM (Total Addressable Market) expansion. However, for a £1,000 investor, the current price represents a "frothy" entry point. The smart money is currently looking for proof of infrastructure build-out in Labuan before committing to a long-term "Buy and Hold" strategy.

Please wait processing your request...

Please wait processing your request...