Rolls-Royce Holdings PLC (LSE: RR.) has transitioned from a pandemic-era recovery play to a high-octane growth engine under CEO Tufan Erginbilgic. As of January 2026, the company is no longer a "value" play in the traditional low-multiple sense; it has become a premium-priced industrial compounder.

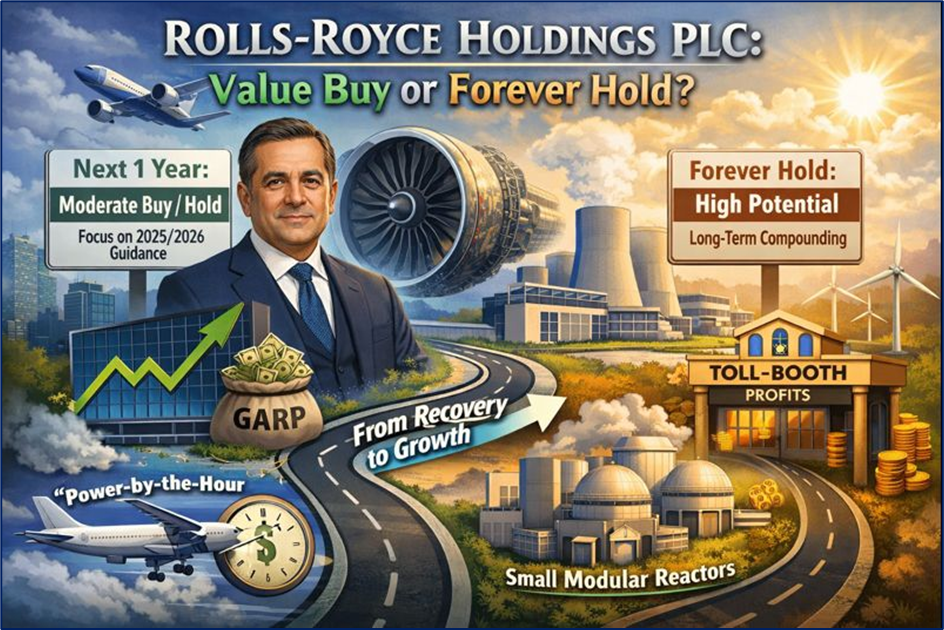

Investment Thesis: Value Buy or Forever Hold?

Rolls-Royce is currently characterized by "Smart Money" as a GARP (Growth at a Reasonable Price) prospect rather than a deep-value play. For the next 12 months, the upside may be capped by high valuation multiples, but for wealth compounding over decades, its dominant position in wide-body engine servicing and Small Modular Reactors (SMRs) makes it a structural winner.

- Next 1 Year: Moderate Buy / Hold. Analysts suggest much of the "low-hanging fruit" from the turnaround is priced in. The focus is now on meeting raised 2025/2026 guidance.

- Forever Hold: High Potential. The transition to a recurring revenue model (Power-by-the-Hour) and nuclear energy creates a "toll-booth" style business model ideal for long-term compounding.

Source: Kalkine Group

Global Institutional Sentiment & Market Coverage

Top-tier investment banks and fund managers have shifted from skeptical to "Overweight," though price targets are beginning to converge with the current market price.

- Investment Banks (Goldman Sachs, Citi, RBC): Generally bullish. Citi recently raised its 12-month target toward 1,440p, while others like J.P. Morgan remain more conservative at 1,040p, citing valuation "gravity."

- Smart Money & Hedge Funds: Institutional inflows have remained strong, with firms like BlackRock and L&S Advisors maintaining or increasing positions as the company’s Free Cash Flow (FCF) reaches record levels.

- Broker Consensus: Currently sits at a "Moderate Buy." Out of 18 major analysts, 14 maintain Buy/Outperform ratings, 4 are on Hold, and 0 have a Sell rating.

The Business Model: From Engines to Ecosystems

The "New Rolls-Royce" operates on a high-margin, recurring revenue framework across three primary pillars:

- Civil Aerospace: Shifting focus from selling engines to long-term service agreements (LTSAs). With engine flying hours (EFH) at 109% of 2019 levels, the "aftermarket" is a cash machine.

- Defence: Benefiting from geopolitical shifts. Key contracts include the AUKUS submarine program and Eurofighter Typhoon engines for NATO partners.

- Power Systems & SMRs: The "Wildcard." SMRs (Small Modular Reactors) are targeting profitability by 2030, with the UK government recently investing £2.5 billion. This segment is being positioned to power AI data centers globally.

Latest Financials & Operational Updates (Jan 2026)

- Operating Profit: FY2025 underlying operating profit is guided between £3.1bn – £3.2bn, up 24% from 2024.

- Free Cash Flow: Surged to £3.0bn – £3.1bn, providing massive "dry powder" for buybacks.

- Dividends: The company has reinstated its dividend, with an interim payout of 4.5p and a projected total 2026 dividend of 11p per share.

- Share Buybacks: Completed a £1 billion program in late 2025 and launched a new £200 million interim buyback in January 2026.

- Net Debt: Successfully reduced, with the company now sitting on £1.1bn in net cash, a complete reversal from its debt-heavy past.

Technical Analysis: The Chart Overview

Source: Trading View

The stock is currently trading in a strong upward channel, though it is testing major resistance levels.

- Trend: Bullish. The stock is holding well above its 200-day Moving Average (1,001p) and 50-day Moving Average (1,128p).

- RSI (Relative Strength Index): Currently around 68, signaling it is approaching "overbought" territory. A short-term pullback to the 1,165p support level would be considered a healthy consolidation.

- MACD: Remains positive at 43.42, indicating that the upward momentum has not yet exhausted, despite the high P/E ratio.

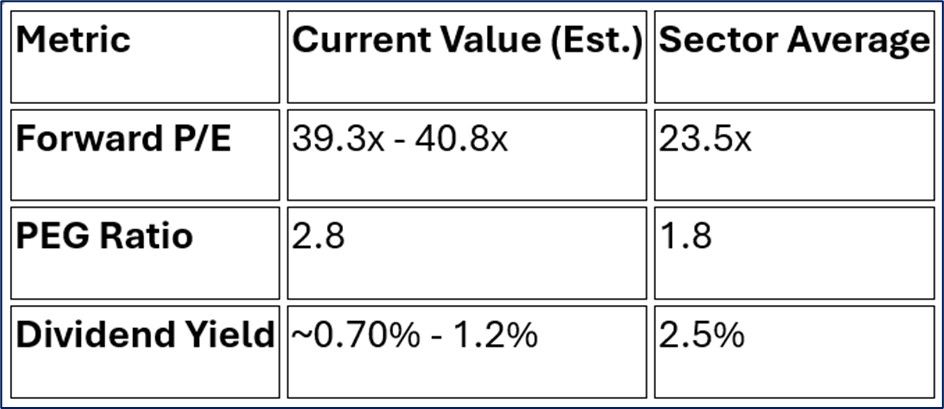

Valuation & Key Risks

Source: Market Data

The Risks

- Valuation Fatigue: Trading at over 40x earnings leaves zero room for operational errors.

- Supply Chain: Lingering constraints in aerospace components could delay engine deliveries.

- SMR Uncertainty: While exciting, the nuclear technology is still unproven at a commercial scale and carries significant regulatory risk.

Conclusion

Rolls-Royce is no longer a "cheap" stock, but it remains a high-quality growth story. While the short-term (1-year) outlook suggests a potential cooling off as the market digests recent 100% gains, the long-term (compounding) thesis is arguably stronger than ever. The shift toward high-margin services, a fortress balance sheet, and a dominant position in the future of nuclear energy suggests that for those with a "forever" horizon, the business remains a core industrial holding.

Please wait processing your request...

Please wait processing your request...