Nvidia 2026: The $5 Trillion Throne and the "Rubin" Revolution

As 2026 unfolds, Nvidia (NVDA) stands at an unprecedented crossroads in financial history. Having recently crossed the $5 trillion market capitalization threshold, the company has transitioned from a chip designer into the essential "operating system" for the global AI industrial revolution.

Global fund managers and analysts are no longer just looking at GPU sales; they are tracking "Sovereign AI" budgets and the shift from model training to large-scale inference.

Global Analyst Forecasts and Price Targets

The consensus among major global brokers is overwhelmingly bullish, though valuation scrutiny has intensified. As of January 2026, analysts have set a wide but optimistic range for the year ahead:

- Average Consensus Target: Approximately $250.00 to $264.00, implying a 30%–40% upside from current levels near $188.

- High-End Targets: Evercore ISI leads the bulls with a $352.00 target, citing a potential 79% jump in revenue by mid-2026.

- Moderate/Bullish Targets: Bernstein SocGen and Bank of America maintain targets around $275.00, banking on the successful ramp-up of the Blackwell Ultra and Vera Rubin platforms.

- Bearish/Conservative Scenarios: Even "bearish" revisions, such as HSBC’s adjustment to $185.00, still project earnings that sit 8%–14% above broader market consensus, suggesting a very high floor for the stock.

Key Growth Drivers and Business Model Evolution

Source: Kalkine Group

Nvidia has fundamentally altered its business model for 2026, moving away from "semiconductor cycles" toward a "One-Year Rhythm" of architectural releases.

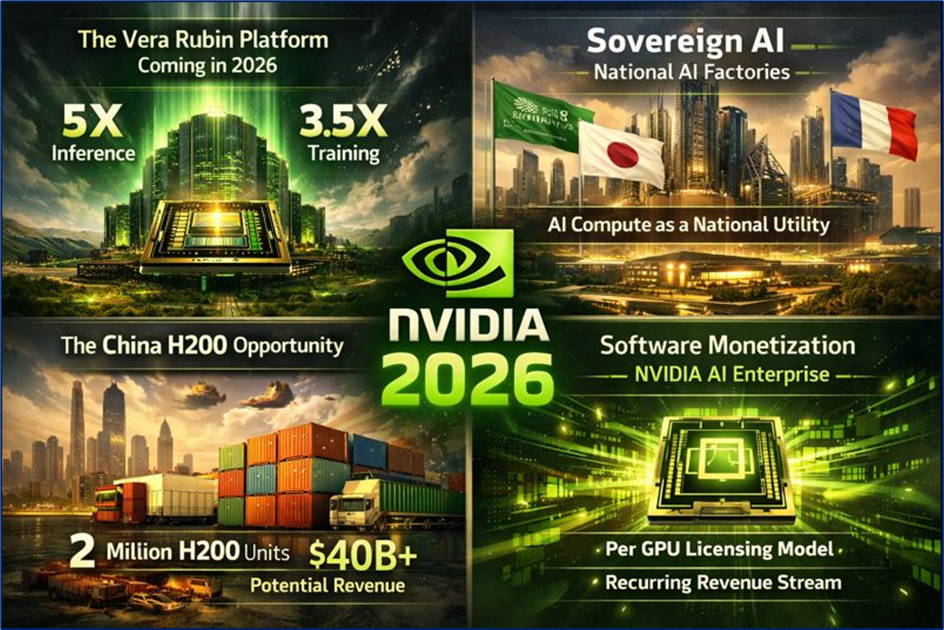

- The Vera Rubin Platform: Shipping in the second half of 2026, the Rubin architecture is expected to offer a 5x improvement in inference performance and 3.5x in training compared to Blackwell, further widening the competitive moat.

- Sovereign AI: Nations like Saudi Arabia, Japan, and France are now treating AI compute as a national utility (like electricity). This "National AI Factory" trend provides a non-hyperscaler revenue stream that is less sensitive to Silicon Valley capital expenditure (CapEx) fatigue.

- The China H200 Opportunity: Following shifts in U.S. export policy, Nvidia is poised to ship up to 2 million H200 units to Chinese firms in 2026. Even with a 25% revenue-share agreement with the U.S. government, this could add over $40 billion to the top line.

- Software Monetization: Through Nvidia AI Enterprise, the company is now capturing recurring revenue via a per-GPU-per-year licensing model, transforming from a one-time hardware vendor into a high-margin software ecosystem.

Financial and Operational Updates

Nvidia’s fiscal 2026 (ending January 2026) has been a year of staggering efficiency and capital return.

- Record Revenue: Third-quarter revenue hit a historic $57 billion, up 62% year-over-year, with Data Center sales alone accounting for $51.2 billion.

- Margin Supremacy: Gross margins have stabilized in the 73%–75% range, a testament to the pricing power of the CUDA ecosystem.

- Shareholder Returns: The company returned $37 billion to shareholders in the first nine months of fiscal 2026 via buybacks and dividends, with over $60 billion still remaining in its repurchase authorization.

- Inventory Expansion: Operational focus has shifted to aggressive inventory building to meet a $500 billion order book spanning 2025 and 2026.

Latest Analyst Upgrades and Downgrades

- Bernstein (Upgrade/Reiteration): Outperform rating maintained post-CES 2026, calling the Rubin platform "a monster" that justifies a premium valuation.

- Evercore ISI (Upgrade): Raised target to $352, identifying Nvidia as the "top pick for 2026" due to the accelerating shift from CPUs to GPUs in the world's data centers.

- HSBC (Tactical Downshift): Lowered target to $185 from $195 while maintaining a 'Buy'. The analyst cited a slower Blackwell ramp in early 2026 but remains bullish on the second-half recovery.

- Zacks Investment Research: Highlights a potential 40.7% CAGR through 2028 but warns that Blackwell supply constraints remain the primary bottleneck.

Current Technical Analysis

Source: Trading View

The stock is currently navigating a short-term consolidation phase after the explosive gains of 2025. Technically, NVDA is testing a critical pivot level at $188, which aligns with a recently formed bullish double-bottom pattern. Momentum indicators like the MACD (Moving Average Convergence Divergence) have recently turned positive, suggesting that the "exhaustion" phase may be ending.

If the stock successfully breaks above the overhead resistance zone of $194–$200, the path to the $212 historical resistance becomes clear. Conversely, a failure to hold the **$176 support** could see a retest of the Fibonacci retracement levels in the $168 range. Volume profile analysis shows high "Point of Control" (POC) near current prices, indicating that the market is "accepting" this valuation before the next major move.

Risks to the Forecast

- CapEx Fatigue: If "Big Tech" (Microsoft, Google, Meta) does not see a clear Return on Investment (ROI) from their AI spending, they may moderate their 2027 procurement plans.

- Supply Chain Vulnerability: Dependence on TSMC for advanced "CoWoS" packaging remains a single point of failure.

- Geopolitical Flux: While the China H200 deal is a tailwind, any sudden shift in trade rhetoric could strand billions in anticipated revenue.

- Energy Constraints: The physical limit of the electrical grid to power massive new AI data centers could slow the pace of deployment, regardless of chip availability.

Conclusion

Nvidia enters 2026 not just as a chip leader, but as the primary architect of a new computing era. While the "easy money" of the early AI rally has been made, the transition to Physical AI (robotics) and Sovereign AI suggests that the company's earnings power is still scaling. Success in 2026 hinges on the execution of the Rubin platform and the seamless integration of the China market back into the global revenue stream.

Please wait processing your request...

Please wait processing your request...